Non-employee resources are routinely called 1099 workers, but really fall into the categories of vendors or contractors. The tax code makes no distinctions between a vendor you utilize or a contractor you hire, but they make a difference in how you might think and interact with them. Additionally, vendors are more clearly not-employees, and therefore not subject to the IRS re-characterizing them as employees.

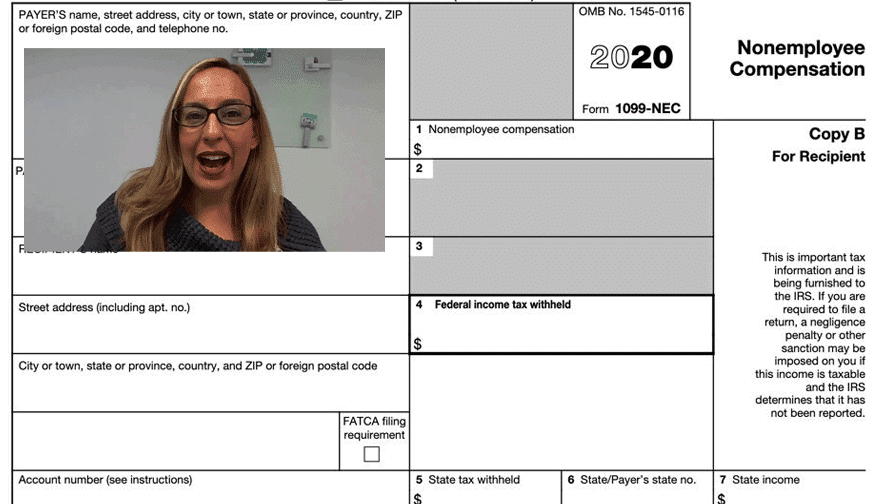

When we pay a non-corporation over $600 in a year, we are required to supply them with a 1099. Before the 2020 Tax year (filed in 2021), everyone received the 1099-MISC. However, beginning in January 2021, you file a 1099-NEC (Non Employee Compensation) for contractors, relegating the 1099-MISC back to miscellaneous things like rent, attorney’s etc.

The rules governing 1099-NEC and 1099-MISC filings are relatively straight forward, but the rules governing who is an employee and who is a contractor is more often challenged and disputed. The IRS has guidelines regarding who is an employee and who is a contractor, but there are no hard and fast rules making this a challenging area of tax and employment law. The switch to the 2020 change to the 1099-NEC was one of the biggest changes to small business filings in a few years.

Making certain that you stay in compliance by properly collecting a W-9 from all 1099 workers and giving them the appropriate 1099-NEC form on a timely basis is critical to remaining in tax compliance. Your business or your tax preparer have to be certain to get everything done on time to get the forms out in January, because your 1099 workers will not appreciate having their taxes held up by your non-compliance.