Educational Video

2020 COVID-19 Stimulus Options, as of April 3, 2020. Learn more about moving tax deadlines, individual rebates, unemployment, the paycheck protection program (PPP), economic injury disaster loans & grants (EIDL).

I just want to make the disclaimer that as I said, this information has changed multiple times this week. It might be different Monday. So just keep an eye on that. I’ll try to update, I’ll try to figure out a way to get information out and updated to people as quickly as possible. Let’s see if I can make my slides work. Oh, hold on one second.

I think I have to change the view back to the navigator. Okay. All right. So what we’re going to talk today about and sorry, I couldn’t get it to work in a better view because I’m on a Mac and I don’t have PowerPoint installed, so it’s a little bit goofy. But we’re going to talk about the different stimulus options for individuals. We’re going to take a look at the big picture what’s going on and what the next steps for you to take are. I’m going to start at the tax because I’m a tax person.

So we’re going to talk about the changing deadlines, the individual rebates, unemployment, the big one, the paycheck protection program or PPP, that has loan forgiveness and a special kind of loan forgiveness at that. The EIDL or that free $10,000 is everybody’s talking about and what we know now, and again, it’s going to keep changing.

So to start with the tax situation, July 15 is the new April 15. The IRS deadlines for anything that was due April 15th is now due July 15th. You don’t have to fill out an extension. This is automatic, but this is for income and self-employment taxes. I sat in a two hour webinar about the tax ramifications of all the new legislations came out. The first hour was just about changing deadlines. So I suffered through that so that you don’t have to, so I can boil it down to one slide for you.

What is due April 15th normally is your prior year taxes. So this April 15th would be due the 2019 taxes that are now due on July instead. Your first quarter, 2020 estimated payment also due on April 15 is now pushed off to July, but not all of the States are conforming. So I’m in Florida. Most of my clients are in Florida. I do have a bunch that are in California, New York, Massachusetts, New Jersey. You have to check every single state. Well, you don’t have to, I have to check every single state.

A lot of the states are conforming, but not all of them. So it’s something we’re keeping an eye on. Other things that have been extended, IRA contributions, HSA contributions, retirement plan contributions. A lot of those things that normally due April 15th have been pushed off. The F bar, which is if you own a foreign bank account, there’s a lot of very… it’s not complicated reporting, but there’s very serious ramifications for not getting those filed. It was not extended, but they have an automatic extension. So we don’t have to panic about that.

But what are a lot of tax lawyers saying? File extensions just in case. I’m sure many of you have had a problem with something totally normal that you normally would do going crazy with the IRS. It’s not that unusual. And here we are in the midst of the apocalypse, do we think the IRS is going to get this all handled properly and smoothly and correctly? It’s probably not. Actually, I called the IRS the other day, they’re closed. There is nobody at any of the call centers. They have sent their entire workforce home from any of the phone numbers that you would call into and they are home indefinitely. So we don’t even know when they’re going to be back to try to help with anything.

So anyone who is a client of mine last year, or this year, I am just filing extensions. No questions asked, no charge. We’re just going through or filing for everybody that’s in our system because we don’t want anyone to run into a problem. And just to cover your butt and make sure everybody’s got better things to worry about than the, “Did I or did I not file an extension for you?” So moving along to the good stuff, the individual rebates.

There are many questions here, but this is what we know. And this is actually what’s in the bill that was passed. If you are a single taxpayer, you’re going to get 1,200. If you’re a joint patent, taxpayer 2,400 and qualifying children under 18, 500, more or less. It’s not 100% exactly what that is. There’s other stipulations, but for most business owners, this is most individuals that I deal with, this is the case that they’re going to fall into. Now, who is getting it? Not everyone.

If you’re married, filing joint, your AGI, which is accountant speak for your Adjusted Gross Income, which is also accountant speak for how much money you make before you take out the deductions itemized or standard deduction, and all that garbage is 150,000. Now, of course, this is the way everything with the IRS works. There’s a phase out. So if you get over 198,000, you don’t qualify anymore. If you’re between the 150 and the 198, there’s a formula for which they’re going to reduce the amount of that stimulus.

Head of household, you’re going to get the 1200 for the head of household and then the 500 for the children, because you have to have children to file head of household. You got to be under 112,500. And again, it’s going to phase out over 146,500. And if you’re single, you want to be under 75,000. And when your AGI goes over 99, again, you’re phased out. Now this, I think we talk about it in the next side. It doesn’t matter. I’ll talk about it anyway.

There’s a little bit of strategy here. They are looking at your 2018 or your 2019 returns to process these rebates. So if you know of back up, if you know, 2018 or 2019 is going to be under the amount, if one year is going to be under, but one year isn’t, if it’s 2018, “Oh, I only made 140,000 in my household.” Don’t file your 2019 yet if it’s going to kick you over that, and the opposite is also true. If you know, “Oh my 2019, wasn’t a great year. I made less money. I’ll get more of a rebate,” file it immediately so that they have that information to work off of. All right, that’s the strategy we’re looking at right now. So non-residents cannot get this. Normally, if you get a tax credit, the IRS will take that credit and apply it to old taxes that you owe.

But that is not the case here. They are not doing that. This is coming for you, no matter what your situation with the IRS is. They are going to direct deposit with the direct deposit bank information from your ’18 or ’19 return, whatever you’ve filed most recently. Now, what happens if you don’t have that bank account anymore? Well, now they’re going to mail it to you. Well, what if you’ve moved since then? And your address is wrong, oh boy, hopefully it forwards to you. If not, there’s a phone number that’s not available yet. They’re going to have some kind of phone call in. If you ever called the IRS in a normal situation, you know you can be on hold for a couple of hours, hoping somebody is going to pick up. I don’t think this is going to be fun if you need to call that phone number.

It’s chaos. It’s chaos right now. And like I said, all the call centers are closed. So this is going to be a separate call center just for getting these checks reissued. They’re going to look at your 2019, 2018 returns. If you do not file, if you have not filed since 2017, you might want to hop on that like really fast and file ’18 or ’19 return. Because if you filed ’18 or ’19, you’re not going to get a check unless your only source of income is Social Security. They’re going to take that Social Security information similar to the tax return information and use those. Then it’s not supposed to… at least at this point, it’s not supposed to be clawed back in 2020, who knows, as I said, things can change, but right now this is what I was told.

All right. Let’s see, I got a question. What happens if your 2018 was filed late and the IRS is still processing? The IRS, the processing part of their of the IRS, like whoever’s in that division is still working. They’re still there. They’re still operational. I’m guessing things are much slower than they used to be. What’s going to happen? Who the hell knows. It takes them a couple of weeks, even from when they’re filed to get it “in the system.” So you might be on a wait and see, you might have to wait until that phone number comes out and give them a call.

Your new part-time job might be calling the IRS at 7:00 in the morning. I’m not sure what’s going to happen. They have not given a lot of information other than what was on my slides as to what’s going on with those individual rebates.

All right, so I’m going to move on to unemployment. So many people got laid off, so many. What was the record number? It was like $69 million, I think, or 69 million people filing for unemployment. It’s devastating. It’s unbelievable. The federal government knows this and they are funneling money to the states to get more unemployment. Now, I’m also going to say the thing that’s tricky with unemployment is that it’s different in every single state. Okay. None of them operate the same way.

The general pattern is you go, you apply for unemployment, you have to go through a waiting period. They make some kind of determination, and then you have to prove that you’re actively seeking work. But now that we’re in the apocalypse, everything is different. I know I was looking at New Jersey for somebody and they said they told you specifically, “If you’re filing because you’re out of work for Corona, put these specific answers in the system.”

I saw something that Florida is waiving the waiting period or something. I don’t know. I think they usually have a waiting period and they’re waving it. So unemployment ranges, usually from the 30 to 50% of standard, I think it’s supposed to pay not way, depends on the state. It’s different everywhere. The Feds have included an extra $600 per week, regardless of what your pay level was. So for some people on the lower end of the pay scale, they actually might be a better off on unemployment than they were working, depending on how that goes.

If you had an employee that you laid off early on, or if you were laid off early on in this whole Corona disaster, you can retroactively get the $600 federal surplus, not surplus, federal addition of unemployment. You can go back to whenever it was first filed.

They also said that they’re extending the 13 week extension that is being paid for by the federal government beyond what your state covers. So if you have a state that maybe only covers three months, the Feds are adding in another 13 weeks on top of it. Oh, let me stay here on unemployment for a second. So one of the things that’s kind of crazy is usually, you have to be on payroll somewhere to get unemployment, but there’s so many unemployed or out of business, single member, LLC owners, or self-employed people, that they’ve actually opened up unemployment that so that people who work for themselves and cannot work right now are eligible to get unemployment. I have a question, “If I have an LLC and get paid through it for my services, do I file for unemployment?” “What happens to a freelancer who’s unemployed?”

Actually, yes, you can file for unemployment. I don’t know what kind of documentation and whatnot they are looking for right now, but they send this 100%. If you’re self-employed, this is not normal situation right now because we’re in the apocalypse. You can go and file for unemployment. S-Corporation owners usually, you’re running payroll because by statute you have to, you can go and put yourself on unemployment. I’ve spoken with other business owners who have as corporations. And they said, “I filed for unemployment, put myself on unemployment because you just don’t know what the cash situation is going to be or how long we’re going to be in this situation.” Now, unemployment or laying off employees is going to take us to the next slide, the paycheck protection program, PPP.

This is the forgivable SBA loan that got a lot of people talking about it. The whole purpose of this is to keep America working, right? This is to help employers keep their employees off of unemployment, keep them at work, being productive. The way they’re calculating it is it’s 250% of average monthly payroll costs up to a max of $10 million. For most small businesses, you’re not getting anywhere near $10 million and you can have it be 100% forgiven, if you’ve got at least 75% of what you get from this program paid towards payroll costs. 100 % can be forgiven if at least 75% of the spending goes towards payroll costs, leaving the other 25 to go towards specific costs that we’ll talk about. This is for small businesses with 500 or fewer employees, including self-employed and contractors.

Then if you are a self-employed person, your net earnings can be considered payroll. Also, I’ve seen, I don’t know if it’s 100% true or not, but I have been told that the money you take out of your LLC is also considered a payroll. Usually, for most taxpayers, the money you take out and your net earnings are roughly the same amount. So I think that’s why they’re doing it that way. But I haven’t gone through this application process. By the way, this application process opens allegedly today. So really hardly anybody’s been through it yet.

So what is it? The PPP? It is an SBA loan under 7(a), and these terms, let me just reiterate. These might change. When we first did this, the interest rate, when we first did the presentation, the interest rate was 4% yesterday. It was 0.5%. And last night when I was updating it, it had changed to 1%. So it’s a very fluid situation. At some point, they’re going to have to nail this down because you can’t apply with things changing all the time. But there’s no payments for the first six to 12 months. It’s deferred automatically. You’re repaying it over a two year term. Originally, they said 10, they’ve lowered it down to two, and up to 100% of the principal can be forgiven. And that’s, again, if you’re putting 75% of it towards payroll cost.

So who is eligible? A business or non-profit with less than 500 employees, including full-time and part-time. And you had to be in business before February 15th. So if you started a new business because you lost your job in the beginning of March, and then you started something new, well, unfortunately, you don’t qualify, but it does include the sole proprietors, independent contractors and self-employed individuals, which kind of like the unemployment, is a little bit unusual because we don’t usually consider those folks being on payroll, but for the situation we are in, they are considered able to apply for these loans.

So 250% of average monthly payroll cost. So that’s going to be your wages. That’s what you’re normally paying out commissions, any other kind of compensation like that, tips if you’re in a business that uses tips, like if you’re a restaurant, vacation, sick leave, if you’re paying someone out an allowance for a dismissal or separation, that would be included, payments for health insurance, for retirement and all those taxes that go along with it.

Also, there’s a limitation on how much payroll costs you can do. So they’re capping it at 100,000. So for example, if you had somebody who makes 150,000, that works for you, you’re only able to include up to the first 100,000. So they’re really trying to help the small, small businesses. So as I said, it does not include employee compensation over a 100,000. If the employee’s principal residence is outside of the US, so say you’ve got an employee under books and they live in, I don’t know, Italy, their wages are not includable in that. Most small business don’t have that situation, but you never know.

Then taxes imposed under IRC section 21, 22, 24, which covers things like dependent care, childcare and that kind of stuff. Those don’t count. You’re like FSA type situations. How are we calculating this loan? So 250% of the average monthly payroll costs. Now there’s a couple of ways that they’re going to look at this, especially if you’ve got a seasonal business. Although really, when my colleague and I went and looked through the bill, it gave us the same sections of the year to use whether you were in business all year, or you were seasonal, which was March 1st through June 30th.

So that means you’re going to have to pull your payroll data, or you’re going to have to pull up your payroll tax returns, your payroll journals, all that information. I hope you’re using a fantastic payroll service, like Gusto. Actually, got an email last night from Gusto that they’re automatically pulling those reports for clients. So if you need that and you’re using Gusto, and if you’re my client, just let me know if you need it, I can get those reports very easily for you. If you were not in business for the last 12 months, you are able to pull the beginning of the year information. I’m pretty sure it’s all of January and February, the February might not be 100% that entire month. I’m fairly certain it is, but we’ll have to double check on that.

I’m going to hop over and take a look at the questions real quick, because this is getting a little… someone asked, “When does PPP open?”

The banks are allegedly taking application starting today. I don’t know that the banks and the SBA are able to transmit all that information, but I know the bankers that I spoke with who are going to be participating in this and that they were doing everything they could to get that in. One of them even emailed me something. And they said, yes, absolutely. They have a short questionnaire that they are taking starting today. This is some examples of just how would you do this calculation?

I don’t know how to make my screen bigger. I’m sorry. So we’re going to start with, if you’ve got 20 employees, which is kind of nice size small business, and this is your payroll costs, sorry, typo over here on the dates. They’re not correct. I wasn’t able to fix that. We’re going to divide it by 12 to get you your average. And you take the average multiply by 250,000. Here is your loan amount. And you see your 20 employees, which is a pretty big, small business, that you’re not getting anywhere near that $10 million limit.

Again, if you’re a zero, no employees, well, that kind of sucks. That would also be if you’re running as a sole proprietor, or if you’re running at a loss you might end up in a situation kind of ineligible. Now for a lot of my clients, you’re kind of in the C and D category. So you might be able to take a loan more in this range, like the under 50,000, which could be very helpful, especially if you have employees because this, again, it’s going to make sure that you can keep them working for you. All right, hold on. I’ve got some more questions.

Is it better to go to banker than to SBA? So here’s a good question. The PPP is funded by the SBA, but you have to go through a bank. I think I have a slide later on that talks about that. Hey, here it is, I think. So you have to go through a bank or a third party lender. The SBA put out a list of their top 100 lenders. Basically, this is being pushed out to the banks and lenders that are already SBA lending. It was the easiest way to get these new loans out.

They are trying to bring new lenders on, but SBA, just like the IRS has sent just about everyone home. So it’s really hard for them to get new banks on board. I would say if you’ve got a banking relationship already, go to that bank. If you don’t or you don’t like your bank, or they’re not doing these kinds of loans you can contact me. I’ve been in touch with multiple associates at banks asking, “What are you doing? Are you getting set up?” And they were all ramping up to get this done. So I could send you to four different people off the top of my head to see what they’re going to do.

So this is a moment… eligible for forgiveness. The forgiveness is not automatic. It’s eligible. It’s max two years.of term, interest rate, 1%. Sorry, some of this is repetitive, but it’s a lot of information. And so we want you to make sure you got it all. I think there’s only one of these loans per entity or tax ID. So if you’re like, say you’re a store that has multiple locations, but they’re all under one tax ID, then you’re only able to get one loan.

The biggest thing, there’s no collateral and no personal guarantee. That is completely unheard of with SBA loans. That’s totally not normal. I was on a call with Congressman Ted Deutch and the local District Director for the SBA, and she was like, “No collateral, no guarantees.” She was like, “Yeah, we do a credit check, but even if your credit sucks, you should apply if you need this. There are other SBA loans that are also available, that they’re being very, very lax about who they’re lending to right now, because they’re just trying to keep everybody’s doors open.

Wrong direction, go this way. I mean, hop over to the questions. Payroll wages are gross or net? They are gross it’s going to be your payroll wages. But for the payroll costs, it’s going to include also the taxes and benefits, all that kind of stuff.

Is there a bank I recommend? Ask me not on here. I don’t want to have this recording making recommendations. I am going to be putting this up on YouTube and I don’t want to get myself in trouble. Does payroll costs cover things like the costs of running payroll? That’s a fantastic question. I don’t know for sure. It seems to be specifically related to the employees, but I would say that it’s probably arguable and we will probably find out more or later.

Download PPP, send to banker. Every bank is going to be different. Most of the banks that I’ve spoken with said that they are going to have an online form of some sort, because there’s a lot of information that they have together. And no banks want a bunch of people standing around in the bank spreading disease everywhere.

Let me see. All right, I’m going to add this, someone asked one loan, so I can’t apply for bridge SBA, PPP, home refi. I’m going to get to that later. We went to our bank was told we need to have applied for a loan prior to February 15th. That is probably not the SBA 7(a) emergency disaster loan. That would be some other loan because this, you can’t apply it until today. So, all right, let me get back into your, how do we get these loans forgiven? I’m just going to put my tax hat back on for a second. What’s super crazy here is it’s not just forgiven because forgiven debt is taxable. These are forgiven and just wiped away, right? There’s no tax implication at all for getting these loans and having them forgiven. It’s just poof, gone, which is kind of unheard of. It’s really amazing.

So allowable costs; they keep changing the rules a little bit, but they said, it’s got to be at least 75% used for payroll because that’s really what they want. They want everybody keeping their employees on. Costs that cover benefits insurance payments, things like that, salaries, commissions. Now, here’s where we get into that other 25% payments of interest, just interest on a mortgage obligation. All right, but you cannot prepay. It’s only normal interest payment. Rent, if you’re under a lease agreement, utilities and interest on a debt obligation incurred before the apocalypse started. All right. So if you go and take out another loan, things like that, it’s not going to include that. Now it’s going to be things that you already had in place. They’re trying to make everyone whole.

So again, at least 75% must be used for payroll costs. I cannot drill that into your head enough. All right, now, things can reduce your forgiveness. If you decrease your employee headcount. If you end up with less employees than you did last year, which is the year that they’re using to calculate. If you do not restore your employees and salary levels by June 30th. So say for example, you laid off your workforce and you told them, “Hey, go get unemployment,” which is a fantastic thing to do right now.

If you can’t weather the storm, as it’s going through, send everyone home, you’re not laying them off. You’re really what we call furloughing them. You’re going to tell them, “I’m going to hold your job available when I can reopen. And when I have something productive for you to do in the business. Go on unemployment for now,” but then you have to bring those people back.

So if you have three people that work for you and you tell them, “Hey, you’re furloughed until we’re up and running again,” you need to get those three people back at the same salary level by June 30th. I know it’s a little bit confusing, but yes, you can lay off your workforce. You’re not really laying them off. We’re calling it a furlough. Lay off implies their position has gone, furlough them, tell them, get on employment, bring them back by June 30th. And you have to maintain the same salary level. So that’s kind of the same thing.

You need to do this all in the eight weeks from when the loan starts. So if you apply today, don’t expect the loan to be funded Monday. It’s probably going to take a couple of weeks for this all to process. Still not clear if the banks take your application, if they can pass it along yet? I don’t know. I just know that take up starting today.

You’re going to have to figure out how to document all of these costs. We have some suggestions as accountants. My first suggestion would be if you get this loan, whatever funding they give you, put it in a separate bank account. Don’t put it in your normal operating account. Don’t put it into your payroll account, put it into a separate account. What that’s going to do is in your system, if you’re using QuickBooks or whatever, you’re going to be able to much more easily identify where those dollars went.

This is so important. If you’re not normally up to date on your books, if you’re one of those, “I wait until the end of the year,” you’re going to get screwed because you’re not going to be able to piece this back together. It’s way more complicated than when you just need to do your taxes.

Because when I need to do someone’s taxes, I can take kind of any garbage they give me, make it work. Get the tax returns done. That is not the case here. They’re going to want to verify specific transactions. Don’t know how that is going to happen at this point. I don’t know if they’re going to have forums or what, but as far as applying for the loan, you have to make certifications on the application that you’re going to use it just for the payroll and those mortgage interest, et cetera. You’re going to have to document all of this.

So this is where if you don’t have a good bookkeeper, if you don’t have good bookkeeping you need to get it together and set it up. Obviously, you can always come to me. I do this stuff all day, all night, we’d get you set up. We can even do your bookkeeping if you want. You know, it’s not, not a sales call here. I’m just telling you there are resources out there. I know other bookkeepers who are fantastic. I can put you in touch with, but this is so, so important because this is the crux of the loan being forgiven. All right, this is put a big highlight on this.

All right. Let’s move on to the free $10,000. Somebody has her school districts receiving any help with non-instructional employees. I’m the school treasurer working from home a few hours a week. I have no idea. School districts are not able to apply for these because they’re a part of the government. And this is only for businesses. If you’re maybe part of the PTA, if the PTA is its own non-profit, they could probably get help. And it would probably fall into what we’re going to talk about now. So this is the free $10,000. All right. Free.

I’m going to tell you what my experience has been so far. A week ago, Friday, I pulled all the information for applying for this EIDL loan. The economic injury disaster loan. I pulled the information from SBA. I gathered the forms that it said that I needed, looked at it over the weekend. Monday I went to start filling out those forms, went to upload it and saw they had changed the website.

And it was super confusing and anyway, because really wasn’t clear what you needed. They said, “Here, take these forms,” and some of them really didn’t apply to my situation. And I wasn’t sure what I was filling out. When I went on Monday to upload them. They said, “Oh, if you’re applying for this click here.” So between last Friday and last Monday, they changed it from a complex confusing website, list of forms with an upload feature to a web form. All right?

It says on that web form right now that it takes about two hours to get it done. I got it done in five minutes. If you have your information, it’s not that bad. EIDL alright, this is the $10,000 that everyone’s talking about and I highly encourage you to go to the SBA website and go fill this out if you have not done so already, right? The funds are limited. It’s, I believe a first come first serve. This part is not eligible for forgiveness under the PPP. And basically what’ll happen is if you get this and then you apply for the PPP, they’re going to refinance this part into the PPP. So if you get 10,000 from the EIDL and then say, you get 50,000 from the PPP, PPP is really only going to be another 40,000.

So you’re not going to get 10 plus 50. You’re going to have the 10, they’re going to say, “Okay, we already gave you 10.” That’s why they’re calling it an advance, right? You might see that it’s a loan advance. That’s the advanced part. So you would in total get 50,000 with PPP, but the PPP is only going to give you an extra 40. This is also available for small businesses and non-profits, 500 employees or fewer.

The interest rate’s 3.75 for business, 2.75 for nonprofit, because there is that loan component. We’re not talking about that $10,000 that’s if you apply for this EID loan beyond the 10,000, right? And that this can be used for payroll as well and other operating expenses. Okay? So you need to think about carefully, what are you going to use this money for? Because you can’t double dip and use the PPP for payroll and use the EIDL for payroll as well. Only one of them is going to be for payroll.

So if you’ve still got a lot of other operating expenses, you could potentially need the EIDL and the PPP, you just have to, again, document. This is where you need good books. You need to be on top of it, probably every week. Probably not even every month. It’s probably going to be a weekly record, keeping hell to get this money, but it’s worth it to have a forgiven loan that’s backed by the government. Okay?

That’s all I’m going to say. Beat that dead horse record, keeping record, keeping record keeping. Let’s move on the grant. This is the free $10,000 free, right? We’re going to call it air quote free. I applied Monday. They’re supposed to fund it within three days. It’s now Friday, there has not been a $10,000 deposit in my bank account. All right?

I don’t know what’s going on behind the scenes. They are claiming it’s available within three days. Clearly that is not the case. If you have done this EIDL grant application and you got your $10,000, please let me know. Because so far I have not heard of a single person actually getting this money. The biggest and best thing about this, is that this $10,000 does not need to be repaid. The webinar I was on with Congressman Deutch, he said, “This does not need to be paid back. Go apply for it.” All right? Straight from Congressman.

If you go through the EIDL application, that website, there is a box at the very end that says your check here and says, “I would like to request the advance,” check that box. If you didn’t check that box $10,000 is definitely not coming. All right? And as I said before, if you get the PPP, the loan afterward, they’re going to subtract this, right, that advance right out of it. All right, hold on. I’m going to stop for a second. Check out our questions.

Okay. Someone else said, it took them five minutes to apply both at the same time, five for one first, and then the other. The EIDL has been available to apply for since Monday, the SBA, 7A, the PPP, you can only start applying for it now. Yes. You can apply for both. You just have to think about, “What am I going to use this money for?” Okay? Oh, let me back up a second on the PPP. The SBA lady director said that you could get this and not use it, right? If you go and you qualify for the PPP, you don’t have to take it. You’re not under an obligation to take it. You can request more. If you find out you need more, later you can request it to be to, to shrink the loan if you don’t need as much.

But if you think you might need it, go ahead and put in the application. The only thing it’s going to cost you is some time, right? Time and some gathering of information. Someone else asked, “If you start a sole proprietorship business in January, had no revenue to show in 2019 are there possible options? There were a couple of contracts and pipeline, March, blah, blah, blah. They’d be eligible for unemployment.”

Eligible for unemployment, I am not sure. I would say it depends on your state. Try it and see. They might give it to you. Oh, one tax thing about unemployment. As of right now, unemployment is still taxable. Okay? That could change. I have not heard anybody say, “Here, go on. It’s unemployment and we won’t tax it. So you either need to withhold on it, if you have that option, when you apply for unemployment or you need to set aside money, even if it’s just mentally set it aside.

Know that come April from what we know right now, it will be taxed as income. Unemployment. I’m just talking about unemployment. As far as you started the business in January, didn’t really have any revenue. You should be able to get the EIDL $10,000 free money grant at advance should be. Like I said, I applied for it on a Monday, haven’t gotten diddly squat in my bank account. I was really hoping I’d wake up today, there’d be a $10,000, extra sitting there. So far, nothing, but there’s no harm in putting in these applications. Okay?

What are the websites to go on? If you go to sba.gov/duh, I think disaster. I will check and make sure. Can you apply for multiple S-corps? You can, as long as they have different EINs, which I would imagine if you have different S-corps, they have different EINs. You could do, you could theoretically do this $10,000 for every single business. If you have multiple businesses, you could do it for each one.

Did you get an email confirmation? I did not get an email confirmation for my EIDL. I got a confirmation screen, a number that I printed. I heard of people very early on, like if they went last Friday and put in for the EIDL in the super complex upload random file way, they said they did get a confirmation. And what they were saying was what they being the SBA was saying, if you, even, if you got, you know, submitted it, go back and do the streamlined online version. So who knows?

If the person has two W2 jobs, get separately, laid off, do they get unemployment? If you file for it, you should get unemployment. I don’t think it matters how many jobs you have. I think they, they do it in a percentage of what you get paid. I haven’t filed unemployment personally in a long time. So not that I’m not that curious. Separate bank account for EIDL. This is my suggestion actually, is if you get that EIDL, because I’ve had a lot of conversations.

People are like, “Well, I don’t really believe it’s going to be free. I don’t believe they’re going to not want me to repay it.” And what I’m telling people is if you’re concerned about that, apply for the grant. If and when the $10,000 comes in, open another bank account and park it there. Okay? Just sit it there. Then if they say, “Oh, hey, by the way, yeah, it’s really a loan and you’re going to pay interest if you don’t use it, blah, blah, blah. And you don’t want to deal with it, send it back. Just pay it off.

What if you forgot to check the box? I would say one of two things, either go and do the application again and check the box this time, or you might be screwed. I have no idea. This is so new. So, many unknowns. I mean, at this point, who knows if the money is even going to show up because I haven’t heard of a single person getting it. I would say probably just go put the application in again, check the box. Is EIDL for multiple S-corps, not tracked to ultimate beneficial owner? Do they ask if owner has multiple entities? So they actually are not asking if there’s, if the owner has multiple entities. The form asks if, well you have to list all the people who are owners. Will they eventually say, “Oh, hey, you own three different S-corporations?” 100%.

“We gave you this three times. That’s not what we meant to do.” Maybe. As of right now, no idea, but good question. I’m working with some clients. Only half of my income has been significantly reduced going to apply for unemployment or do I need to have no income coming in right now for a small business? That is another good question. I believe you would probably have, well, I think it might depend on what your business structure is, first off. And second, I don’t really know the answer to that. What I will say is you could always try, right? It’s a little bit tempting, with that extra $600 a week. I don’t know who isn’t like, “Oh, you know what would be great right now? An extra $600.? I have colleagues who said, “Yeah, I have an S-corp, but I put myself on unemployment.”

I myself have not done this yet. Mostly because I’ve been hearing horror stories about the Florida Department of Revenue website and taking hours and hours and hours to get that process done only to be kicked out near the end. I remember the last time I went on unemployment, it was a nightmare. It was years ago. It was before I started my firm. Oh my God. It was terrible. It was such a nightmare. But I can’t imagine it’s any better right now. With all of these programs, what I’m going to say is, it’s so chaotic that you might as well try, right? There’s not harm and trying. And if you’re worried about it, again, you can always go and throw that money into a separate bank, pay it back if it turns out it’s not what you thought it was. All right. So what do we know now? Right.

We covered all the programs. What do we know now? I want to try to wrap this up and leave time for questions. The question, if questions that aren’t answered. We probably will end up going over the hour, but I want to get through the slides before the hour’s up. So what do we know? The SBA and the IRS have to rapidly build systems to process and verify all this data. The IRS, I told you before, the IRS is closed. They are working on skeleton crews, they’ve suspended a lot of their collection processes. I don’t recall, they might have stopped payment plans. I think that’s what I had been told. Not 100%. I can verify though, if you’re on a payment plan and you’re wondering. I could look into that for you. Lenders are going to have to decide if they want to participate in this.

So far, every banker who I know that I spoke with, if their bank already did SBA, they were planning on doing this, but that doesn’t mean your bank will. And it doesn’t mean that they’re the best option for you also. There’s I think it’s like 100. It’s the top 100 list that the SBA puts out. You could look at them. You could look at anyone. Expect a period of chaos for some weeks before money can hit the street with these programs. As I said, I applied on Monday, was supposed to have a three-day turnaround on the EIDL, still waiting. Still waiting for my $10,000. So that money hasn’t hit the street. I don’t know if anybody who’s gone on unemployment is getting that extra $600 or not. Nobody’s told me specifically, and I haven’t heard any stories about it yet.

This is the government in an unprecedented disaster. They are not built for this in the best of times, and now they’ve got most of the workforce working from home. The government is not set up to work from home. And yeah, so today the banks are supposed to be taking information. I don’t know what kind of information. They might just be creating a waiting list and just trying to figure out, “Hey, who’s interested.”

I don’t think they can even put the applications through. I think they’re just gathering information right now. So what options do we have right now? Unemployment. Even if you’re self-employed, you can go hop on unemployment. If you’re business dried up, don’t feel bad, get on there. The feds know that they put people out of business and they are doing what they can to make it better.

I’m not going to say they’re making it right. They’re just making it better. There’s paid family leave and employer credits available. I didn’t get into that. That’s a whole new other set of situations with, I believe The Department of Labor, has a lot of regulations on that. If you fall into that category and you need help contact me outside of this. Get cash whenever possible to hold you over. We don’t know when this is ending. The president said he wanted it to be done by Easter. That’s not happening. He wanted it to be done by the end of April. That’s not happening. And mid May. We’ll see. I’m getting told to expect my kids to not go back to school this year. This is our reality. Probably at least through June.

Will things change? I don’t know. Will they get better? I don’t know. Will they get worse? I don’t know, but you need to be prepared, right? So get a hold of the cash. If you can still go apply for that $10,000 EIDL grant, I would say, go and do it. Cut and reduce expenses. Apply the golden rule. Okay. So for the business owners, this is super important. I’m always telling people, cut your expenses, cut your expenses, cut your expenses. We all bleed money. I do it. I’m sure you do it too. Go through and pull your credit card statements and pull your bank statements and go through line by line by line and see what you can get rid of. Do you have a subscription that hits you every month that you haven’t looked at in two years? Go cut it. Can you call your mortgage company and ask them to put you on a deferral?

A lot of the mortgage companies are doing that. Whenever I log in my main bank is Bank of America, and I see notifications from them like, “Oh, if you need to put loans on hold, let us know. Car loans all this kind of thing.” But the other thing that you have to think about is, is something you’re cutting. Does it contribute to revenue? You might say, “Oh, I spent a lot of marketing. Maybe I should cut it.” That might be the dumbest cut that you could make, depending on what it is.

Now. Maybe you need to evaluate your marketing and see, is it as effective as it could be, but I wouldn’t get rid of your marketing. I mean, unless you’re doing something that you’ve, I don’t know. If you’re an Airbnb, and you market it, that might be the only people who I could think that it’s probably worth it to just stop their marketing expenses.

Do they decrease costs? Are they essential to operations? You might be thinking, “Oh, I want to cut,” I don’t know, I was going to say marketing again. I think because I’m married to a marketer. I have someone who does SEO for me. Well, maybe I’ll get rid of that. So here’s the golden rule. If that’s another small business owner and you’re going to cut them off, first off, you’re probably not helping your business by cutting that cost. If you’re doing something like SEO or advertising.

But are you also going to end up putting them out of business as a result, then when things pick up again, they won’t be there for you. So you really have to think about what are the ramifications down the line of what you’re looking to cut, but the same time you have to do what’s best for you and for your business.

And don’t forget no matter what, you need to fix your record keeping. If you’re getting any of these programs, you need to have sparkling clean books. Trackable expenses, receipts, all of these things. You need to have this stuff impeccable. I’m going to say a little bit of a pivot on the get cash. Whenever possible, you might want to look at how your business is operating and if you haven’t modernized, now might be the time.

I had an office for a little while. I gave it up to keep everything virtual, but is virtual as I am, I’ve had to buy new software. I’m realizing my computer is too old to keep up with some of this stuff, especially things like Zoom conferences. So I’m going to be upgrading hardware. Use this time to make smart changes for your business and how you operate.

If you always wanted to figure out how to work in the cloud, now is your time. If you have questions, I can help you. I’ve been doing it for a couple of years. I don’t have all the answers, but I can at least point you in the right direction. So what’s next. If you’re going to go apply for that SBA loan, you’re going to need payroll records, prior tax returns for businesses and the owners, have your bookkeeping up to date. Probably you’re okay through the end of December, but they’re going to want to see the beginning of 2020. So you’re going to have to get that caught up, right?

We’re going to add new accounts or classes depending on how you want to track things in QuickBooks, to start categorizing all of these COVID related expenses properly, because remember, you’re going to have to be able to easily show those expenses to get the loan forgiveness. And you might want to also go and open a new bank account. I would imagine the bank that you get the loan from would be able to open a bank account for you fairly easily, if you’re okay with having everything in one place.

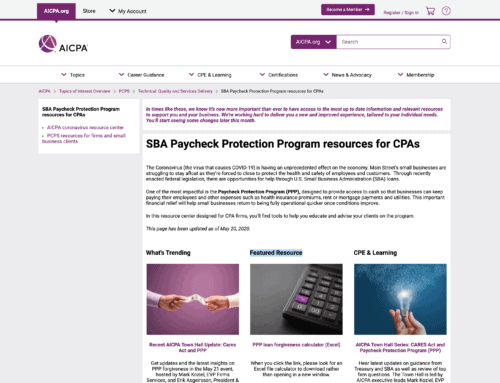

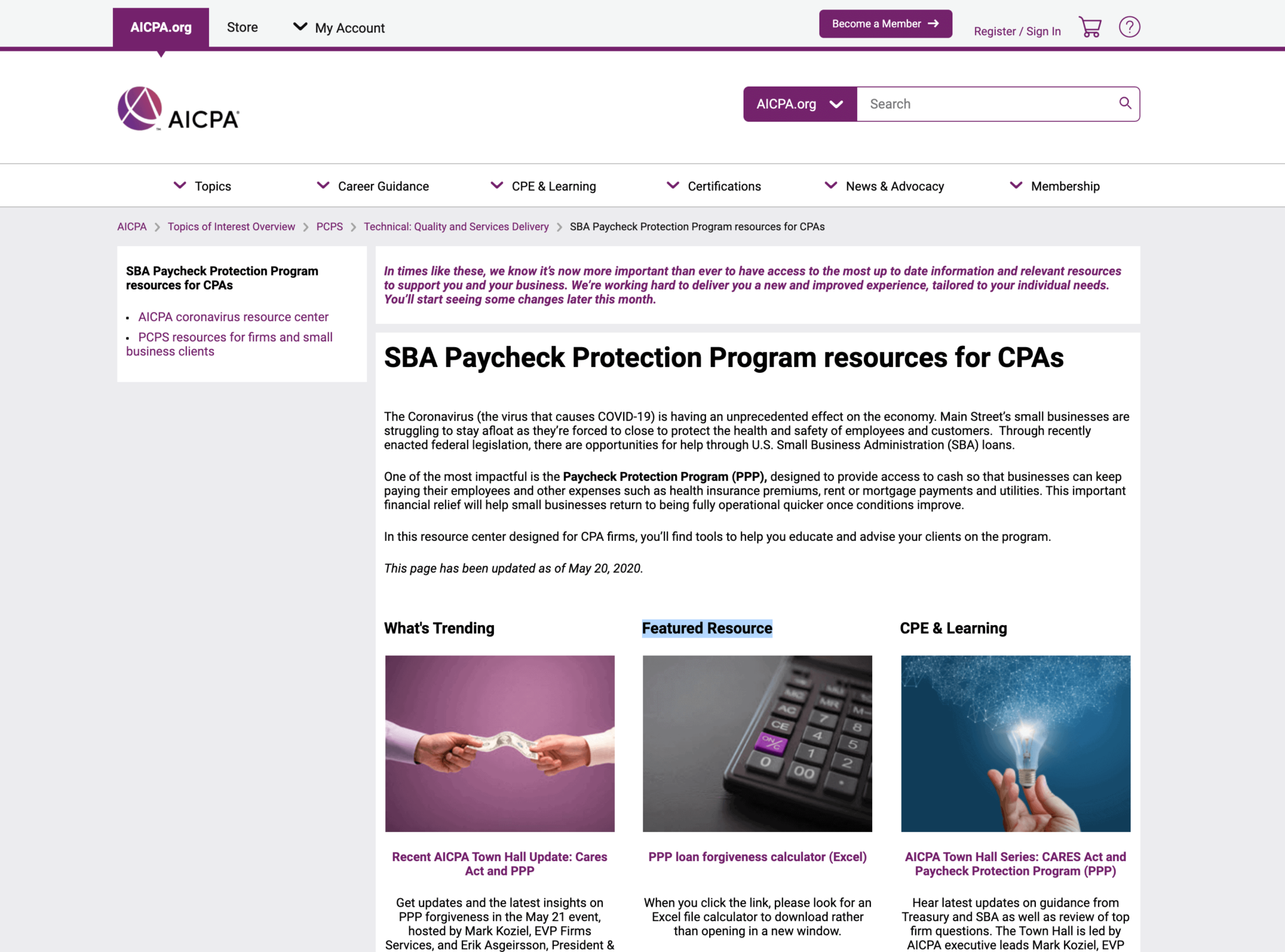

Okay. 11:58. I can’t believe we got through all of that information just under an hour. I’m putting stuff out on Facebook whenever possible. If you are going to apply for these loans and you need assistance, you can go to this. This is a special page we put up just for COVID-19 dealing with this stuff. It is not the easiest process to even figure out what you should be doing, what you qualify for.

I am here to help you. If you need things like book keeping, tax returns filed, if you haven’t filed your tax return for 2018-2019. We could try to help you get that done as quickly as possible to get that all into place for you. It’s first come first serve. We can’t help everybody. I’m trying to help as many people as possible, do as much as possible, put out as much information as possible because at the end we are all in this together.

As much as it sucks. So let me see what else we got for questions. Where can I find the EIDL application? Oh, it is here. I might have to throw it in the chat. Let me see what else I got on these. This is whatever. And then, okay. You have to go broke three times to learn how to make a living and probably happening a lot right now. A lot of people are going broke. I’ve throw in the chat. This is the EIDL. Here you go okay.

Another question regarding unemployment. What if all income is dividend? Ooh, well, that is not wages. I have no idea. I think they might ask you if you’ve got income from other sources. This is really for the business owners, if you had a business that you were getting wages out of or net earnings, if you’re an LLC, I don’t know.

I just don’t know the answer to that question. If a bill is able to be placed on a credit card, should I? Oh, that’s a good question. Okay. So I personally don’t like debt. For most people it’s a black hole. Plenty of studies have been done that if you use credit or something, that’s not cash that you are more likely to spend more money, right? So what’s funny is, my husband and I, when this all started going in lockdown, we were like, “You know what? No more credit cards. We need to make sure that we’re not getting ourselves into trouble. Even if we paid the credit cards off in full, normally, we got to watch our cash.” So I would say, unless it’s a huge bill, don’t put it on a credit card, if you’ve got the cash, because you need to consider, “Do I need to spend this money or not?”

That’s really the thought processes. Is this something necessary? If it’s something really big, maybe you need to, but I would say try to avoid getting yourself into debt right now. Who knows what will be, but you don’t want to keep racking up credit card debt to keep yourself in business. For EID, what if Corp or LLC owned by other entity or entities? There’s actually information they ask for that. They ask if your business is owned by another business. So that is information you will have to disclose. I don’t know that it precludes you from getting the grants or the loan, but it will ask for that information to be disclosed. Okay. Someone wants to talk to me by phone. No problem. In case you get PPP and the 10 K grant and park them just in case terms change, how do you later show it went to payroll? Is that not a catch 22 situation?

So if you are getting that money, first off, if you’re not going to use that PPP loan for the payroll, I would say maybe don’t bother applying. The 10K grant, yeah, you can. For either case. The PPP and 10 K grant. What you’re going to do is you can park it in a bank account. If you’ve got those payroll costs, you’re going to take the payroll, you’re going to run it out of whatever account you normally run it from.

And then you just go in to transfer the money from that PPP or EIDL account into your account. So you have a specific audit trail of where did everything go? How did it get there? What did it go to? And if you are, I’m just going to throw this out there. If you DIY your payroll, or if you’re using, I don’t know, some crappy payroll company, you need to get this modernized immediately.

I love Gusto. Said it before. They’re fantastic. They’re being super proactive. They’re helping people with this reporting requirements. Payroll is one of those things you do not want to screw around with. I didn’t even talk about it, but there’s actually the ability to push off your payroll tax payments. I don’t recommend it. I think that’s a terrible situation to get yourself in.

If you are not able to run your full payroll and pay all the costs, you’re better off laying, furloughing your employees and dealing with bringing them back on later. You can furlough them, get the PPP, get the money back in, bring them back on board, pay them. On your side about PPP to expenses, to payroll or net earnings, something like that. Are you saying that if you have not been running a traditional payroll, you can still be eligible for PPP?

Okay. Here, here is the confusion. All right? If you have an S-corporation and you’re the owner, you have to run payroll. If you have not been, shame on you. I have videos about this. I yell at people about this. I have had, I’ve had audits with the IRS where I said, “Why is the client being audited?” And they said, “Because it’s an S-corporation and the owner is not running payroll.”

So if you don’t have payroll and you’re an, S-corporation, get your shit together to run payroll. Net earnings is really a term that we use for self-employed people. So if you’re a sole proprietor or you’re a single member LLC, an LLC, where you’re the only owner and you file schedule C on your personal tax return, that is, that’s considered your net earnings. So what SBA director said was, whenever you take out of your single member, LLC, out of your sole proprietorship, out of your independent contractorship, you can take that money and consider that payroll.

If you’re an S-corporation. I don’t know that that’s the case. There are a lot of S-corps who you maybe pay yourself, not that much, but take out a lot of money as equity distribution or owner draws. I actually have a question into both the Congressman and the SBA lady who ran the webinar that I was on asking for specific clarity on those. If I find that out, I will share it because it can make a big difference for people. If you normally, like say you pay yourself 25,000 on payroll, as your S-corp, but you pull out another 60 as owner draws. If that 60,000 can be included as payroll expenses, that’s really going to change the equation. That’s a lot of money.

Let’s see what else. The EIDL site doesn’t give you option to choose a grant or PPP. Okay. EIDL and PPP are two separate application processes. The EIDL website is to get you into that system, right? And it’s not asking you for, it’s not asking for tax returns. It’s not asking you for financial statements. The only two pieces of financial information it wants is your gross receipts from February of 2019 through January of 2020.

If you don’t have that, I would suggest just using your 2019 numbers. And it wants your cost of goods sold, if you’re in a business that has cost of goods sold. So you could do EIDL, you can do that now. You can do it while we’re still on the webinar. Go fill that out. The PPP, you have to go through an SBA lender. An approved SBA lender who is doing the 7A lending, right?

So not everybody’s doing it. And if you need some contacts for that reach out to me, I’ll put you in touch. I’m not putting it out here, because this is going out to the internet and I don’t want to get in trouble with anybody. Let’s see what else we got. I mentioned at the beginning couple’s eligible for 2,400, 500 per child. How does one get the money? Okay. We covered this at the very beginning. The IRS is opposed to a direct deposit that money into your account, if on your 2018 or 2019 return, you had that information on there.

If you didn’t have bank information, they’re going to mail you a cheque. And if your address is wrong, hopefully it finds its way to you. Otherwise, they’re going to announce a phone line that you can call and then have the checks re-issued. If you have not filed since 2017, go get your tax returns in. The CARES Act, providing COVID-19 stimulus was rushed through, as is the implementation.

I’ve had a number of clients who fell off the map, come back and say, “Oh, Hey, can we go file those now?” Because they want to get the money. Yeah. Then somebody asks, can you please email replay for those who may have joined late? Yes. I’m going to send, I don’t know if I can send this out depending on how big it is. I’m probably going to put it on YouTube or my website and send out the links.

Last call for questions. Do you know if anyone has received the money from the IRS yet? It is not supposed to go out, I think for a couple of weeks. Maybe next week or so they’re going to start. I don’t know what their timeline is. It’s not instantaneous. Nothing the IRS does is instantaneous.

It’s a very slow organization. They are closed. Their phone rooms are all closed. They sent everybody home. Yeah, no idea when that’s coming. Probably supposed to be April though. Where is the link you post? I don’t know what that means. Julie, go on. If you can clarify your question, where are the link you post? There’s a link in the chat that I posted. It could be that that’s what you are asking for. And then there is also SBA, sorry, that’s for you. That goes slash disaster.

Here’s another good one. This is a lot of information. I might not have sent it. I might not have sent the link to everybody. Hold on. I’ll try again. Okay. So there’s your SBA funding? There’s your free $10,000. And if somebody gets it, please let me know because I really haven’t had anybody tell me that they actually got this money. I’m quitting myself. We see more questions having issues, applying for unemployment once I actually get through, is it retroactive?

I’m going to say that I know the federal part, that wasn’t enacted when all of the shutdown started is retroactive. That’s an extra $600. I don’t know what the States are doing as far as weaving waiting periods and that I’m not sure. But I would say, if you can, go apply for it. Be patient, the systems all are hammered. We’ve never seen unemployment claims like this before. Again, the COVID-19 Stimulus was quickly moved through Congress at record speed.

Oh, something has come up in some of the other webinars, nobody mentioned. So normally if you have employees and they go on unemployment, it hits your percentage that you pay to unemployment. So your unemployment percentage usually goes up. What is going to happen with all these people going on unemployment, especially if you’re an S-corporation owner and you put yourself on unemployment?

We think, we don’t know for sure, but we think that probably everybody’s rates are going to go up. I don’t know how they’re going to fund all of this otherwise, but this is unprecedented. We have no frame of reference for this. This has never happened before. So we just don’t know, but probably everybody’s unemployment is going to go up to help offset this later. This is my conjecture. This is not, this is not law. Nobody has said that this happening. Let me see, posting sending lights. Where does it get posted? It’s in the chat.

No, I don’t know if anyone received IRS money yet. Let me see another question in the chat here. Would at least payment on company vehicle qualifies and approved expense with EIDL? As far as I know, EIDL is for anything pretty much. If it was PPP or asking for, the intra, let me see lease. I don’t know. I think you would qualify in EIDL. Maybe PPP. I mean, this stuff is also changing. There could be things that they just haven’t thought about. They’re thinking about, “We caused businesses to shut their doors, send their employees home. What can we cover with that quickly?” Which was payroll, mortgage, interest, rent. That’s the big things. If you’re a brick and mortar store that you’re getting killed with right now.

I also don’t know if you’re a landlord, I don’t know what kind of help is out there for you. You could probably at a minimum get the $10,000 grant. I asked for specific guidance on people who are renting property. If you’ve got Airbnbs, I have sadly, I have some clients who are Airbnb hosts and they’re getting clobbered because it all got canceled. So it’s a hard time, hard time guys. All right.

So hope this was helpful. I think I got everybody’s questions. If there’s something else, you could try to email me, honestly, my email is so overrun, I don’t know if I’ll be able to get a hold of you. I’m trying to respond to clients first. Obviously you can always become a client if you aren’t one already. I’m doing my best to get as much information out there as possible. And if you need help applying for those SBA loans, reach out to me. It is a service that I’ve started offering, just because of the times we were in.

If you need the background paperwork done, like you might need bookkeeping, you might need your tax returns, et cetera. You know, that’s kind of run of the mill stuff for us. We do it all the time. Reach out and I can always give you a referral to somebody else. If you are just looking for somebody else, I’m not offended, but take care, stay safe and good luck, everybody. Good luck with the apocalypse.

{kind=link}

{kind=link}

{kind=link}