Roy Esh joins #FinanceFriday, discussing the impact of Robo Advising and Robo Investing and Artificial Intelligence on wealth building, investment strategies, planning your retirement economics, and challenges. We cover recent issues affecting investment planning in 2021, including the GameStop / Robinhood Markets controversy and other issues. In this great conversational #FinanceFriday, it was fantastic to talk about wealth building, investing, the pandemic, and other issues in the news.

Bette Hochberger:

Welcome to Finance Friday. And today, my guest is the illustrious Roy Esh.

Roy Esh:

In the flesh. Yes.

Bette Hochberger:

Sort of. I would say IRL, but we’re not really, really here. We’re like talking heads. Roy has been a dear friend of mine for many years, ridiculous number of years. Personally, my life insurance guy, my go-to, my favorite one in the world, has mine, handled business stuff for us for a long time. So I was thrilled to have him on because he knows so much about so many things. And today we’re going to talk about some really interesting things, and this is stuff that’s really over my head. I know a lot about a lot. I don’t know a lot about this. You want to start, introduce yourself a little? Tell us a bit about yourself?

Roy Esh:

Yeah, I’d love to. So my name is Roy Esh. I’m a financial advisor licensed in many, many states, and my main office is in Aventura, but when I’m not there, I’m working from home, and I help people do really smart things with their dollars. So I focus in a few different areas of financial planning. The first is wealth management. It’s a fancy way of saying investing. And we make sure that clients are diversified. We make sure that clients aren’t taking on more risk than they’re comfortable taking. And then we also make sure that clients have some dollars that are not on the roller coaster. Invariably, that’s what everyone wants is some dollars that are not on the roller coaster. The second area that we help our clients in is risk management, fancy way of saying insurance, making sure clients have the right amount and the right kinds of insurance in place. Finally, tax management. Now I am not a CPA. I’m not going to be checking boxes and doing your tax return. That’s what she does. But we are strategy people.

Bette Hochberger:

That’s what I’m here for.

Roy Esh:

Exactly. We are strategy people. We make sure that people are being efficient for tax purposes. That’s on the individual side. On the business side, we help with group benefits, 401k, group health, all that good stuff. But that’s what I do. But today we’re going to be talking about some really interesting things that I thought would be nice to bring to the forefront of people’s minds, which is more of, where’s the future in my business? Where’s the future in finance? There’s all kinds of wacky stuff going on. And it’s probably good to keep an eye on it.

GameStop Controversy and Situation

Bette Hochberger:

Can I put you on the spot for a second?

Roy Esh:

Yeah, sure.

Bette Hochberger:

Can you explain that whole GameStop thing? What was that? I know it’s over my head. I know sort of basics of investing, but I didn’t know what was going on there. People were asking me, I’m like, “I don’t know, Google it.”

Roy Esh:

What’s interesting is, it was a chance for the little guys to kind of stick it to the big guys, and it was definitely interesting to watch the whole thing play out, but at the same time, that’s not typical of financial planning. If I’m a financial advisor, I’m not telling any clients to load up and to back up the truck and load up on any one particular stock over another, especially not when there’s speculative stuff going on. But that was an interesting thing to watch. And it was fun to kind of be a cheerleader to see. I mean, no one wants to see anyone fail, but if there’s anyone you do kind of want to see people failing, it’s probably those with the mega yachts. I saw a meme that said, “These poor guys, they can’t afford to redo their mega yacht now. They have to wait another six months to do it now.”

Bette Hochberger:

I know, aren’t we all crying over that? I hate when I can’t redo my mega yacht, God, I don’t want to use the old one, an old yacht.

Roy Esh:

To me, the memes were more entertaining than anything else. I’m so glad we live in this meme culture because without it, you’re watching the news and there’s nothing fun about it.

Robo Advising

Bette Hochberger:

No, there’s nothing fun on the news otherwise. Oh my goodness. So after putting you on the spot for that one, so can you tell us a little bit about this here at robo advising? What does that mean? Because I picture legit robots, like a Roomba, but now it’s cleaning the floor, it’s picking your stocks for you. So what is it really? Because I don’t think that’s actually what it is.

Roy Esh:

So interesting about robo advisors is the fact that, well, let’s just back up and just talk about what computers are. Computers are basically hardware that runs on software. Software, a fancy way of saying software is algorithms. So essentially, these robo-advisors are not, if you saw the movie, Will Smith, I Robot, they’re not metal things that look like Terminator that are doing calculations, but their software, the CPU that works inside, is pretty much like that. Where they can run hundreds of thousands of different calculations, looking back at previous returns, factoring in inflation, and they can really do quite a bit in a very short amount of time that humans can’t do, as far as calculations.

Roy Esh:

At the same time, there are some biases that are built in to these things. Because the people who designed the software are have faults. They’re people. So look, the last thing I want to do is whip out my crystal ball and tell you what the future is going to be. But what I can tell you is that the trend has been that there has been a lot of money going to robo advisors. Now, where I stand on it. So the way we leverage robo-advisors is we use quite a bit of sophisticated software ourselves. And you can actually subscribe to these robo-advisors and you can come up with an allocation, and make your investment portfolio revolve around whatever their recommendations are. The only thing is, if you don’t have a conversation about what your goals are, if you don’t have a conversation about what your risk tolerance is, if you don’t have a conversation about what your threshold for pain really is when you see your account down, there could be some issues. So what the robo-advisors are doing now is they have people you can talk to, right? Now, it’s not people you’re meeting with, it’s people you’re talking to on the phone.

Bette Hochberger:

Are they real people?

Roy Esh:

Yeah. They are real people.

Bette Hochberger:

Okay, it’s not a chat bot or something like that, that’s going to have pre-planned, “Yes, no?”

Roy Esh:

I actually have a story about a chat bot. I gave it a shot once. I had an issue with my electric piano, my daughter is taking piano lessons and I went onto the website and all they offered was a chat button. I’m like, “Let me give it a shot. Maybe this robot can help. I don’t know.” So sure enough. Yeah, it just didn’t do anything. It didn’t have a solution to figure out that I needed to do a hard reboot on it. That’s all you had to do. Thankfully, Google search is what helped my case, and YouTube.

Bette Hochberger:

YouTube, you can kind of figure out anything from YouTube, At this point. How to do your taxes. I put those videos up sometimes. Anyway, digression. Okay. So these robo advising companies are starting to have, they have to have a human touch, I guess. They can’t do it all on the computer.

Roy Esh:

Correct. Correct. So, the way I see it is either you’re going to have a robo advisor with a human element, or you can have the human element with the robo advisor software and technique. So this stuff that we used, so I think what would be helpful, Bette, is if I give kind of a rundown of the different tech that I use in my business, and then I can kind of back into and show you where the robo-advisor aspect of it fits in. Is that okay?

Artificial Intelligence in Finance

Bette Hochberger:

Yeah. You know what though? I just want to give you a corollary to my industry. So, I mean, I don’t know how accounting tech normal people are. I hear about all the time, because in the industry, we’ve been hearing for years, “AI, you’re never going to do bookkeeping again. It’s all going to be smart computers, intelligent.” And every once in a while, there’s these companies, I’m not going to name names, but they come out and they say, “Oh, there’s no people, we don’t need people. Our algorithms are so smart. We can do all your bookkeeping for you.”

Bette Hochberger:

And you know what happens to the people who use those companies? They come to me afterwards to fix it because the computers are not that smart. Believe it or not, it’s actually shockingly hard to make a computer be able to think about transactions, at least on the accounting perspective, to think about transactions the way a human does. It can’t differentiate, “I went to Macy’s on my business card and that’s a personal thing,” versus, “I bought a gift for a client at Macy’s and now it has to go somewhere else,” because it can’t ask you the questions and have the conversation and find out what is the intent behind things? So it’s funny to hear that this is kind of invading everywhere. It’s not just my industry.

Roy Esh:

Here’s another thing. Here’s another thing. Before I got into finance, I was a consultant for a software company and there was an internal joke that we used to say when people were using software, was, “Maybe it’s just an ID10T error” An ID10T error was our way of saying user error, because if you spell out ID10T, it spells out “idiot.” Okay?

Bette Hochberger:

Yeah, I kind of figured.

Roy Esh:

No, but that’s really what software is, is garbage in, garbage out.

Bette Hochberger:

It doesn’t actually think for you.

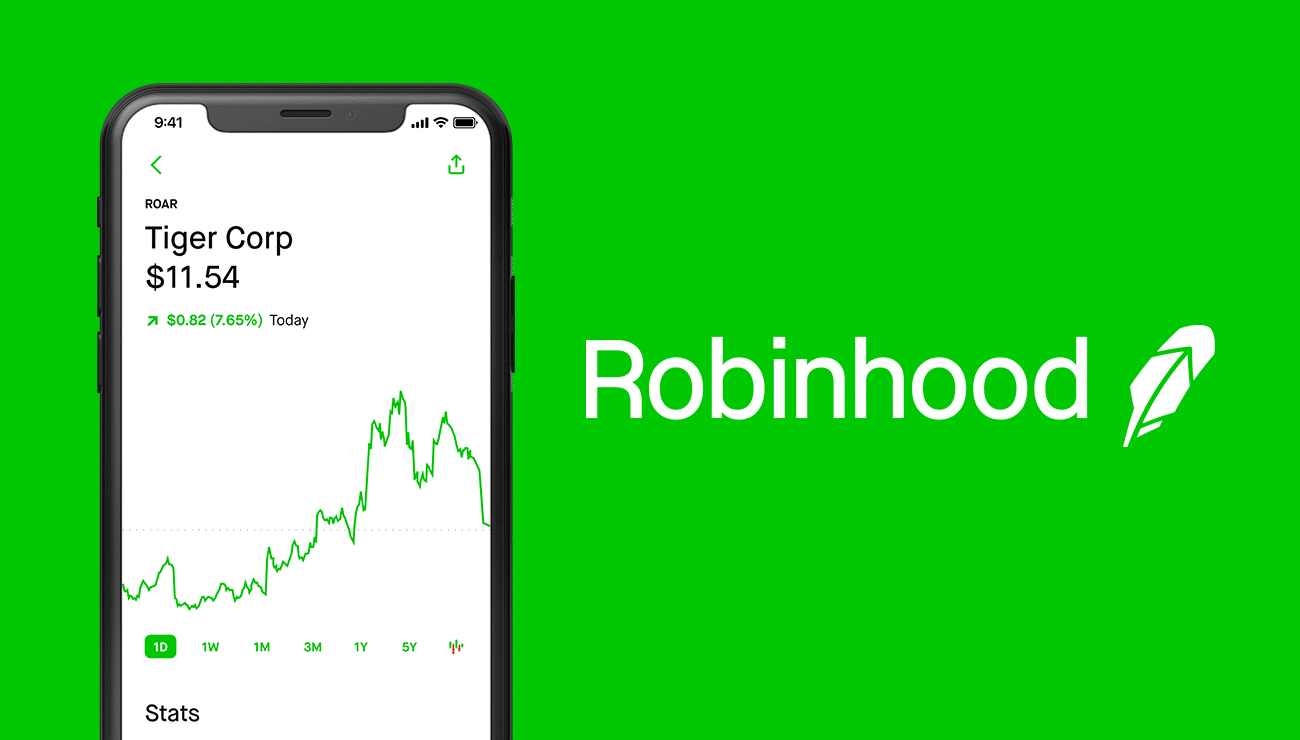

Robinhood Market

Roy Esh:

Correct. So I don’t know about you, but the way I would want my financial advisor, if I were in my client’s shoes, is I think I would prefer the human element that utilizes the technology, the human that uses all the state of the art, whatever is readily available today. And then that they’re going to keep pace with what’s to come. That’s what I would want. I don’t know if I’d want to deal directly with the robo advisor and then if there were issues and then maybe there’s a human on the other end, but who knows their qualifications? And that’s really the direction that I see in my practice, in my business.

Bette Hochberger:

Yeah. I think it’s a neat idea. I think it’s almost like a neat idea if you’re not that savvy of an investor that you think, “Oh, a robo thing, it’ll just be right. The computer will just figure it out for me.” So maybe we can segue a little bit into some of these smaller things that are a little more accessible to the general public, letting people get into investing in, I guess, a low barrier to entry, would you say? Maybe a Robinhood kind of a thing?

Roy Esh:

Yeah. So if someone were to ask me, “What is Robinhood?” I would say, “Oh, it’s a discount brokerage that you’re able to use from your phone.” That’s really ultimately what it is, is you can buy individual stocks, you can buy ETFs and you’re not doing anything too sophisticated. You’re not constructing crazy portfolios. You’re not really doing what we call, the way we invest for clients is we call it institutional style investing based on modern portfolio theory. What the heck does that mean? It’s a mouthful, but institutional style investing means, think of the Harvard endowment. They’re not saying, “Hey, let’s buy Home Depot over Lowes,” They’re not looking at the quarterly returns and saying, “This is the better move than that.” But they do, if there is an idea that they think construction, or they’re going to make a move in that sector, and they do invest across all different nine asset classes, and that’s essentially how we do it.

Roy Esh:

So you’re not going to get that with Robinhood, but maybe you’re not meant to. So I have some clients that like to be stock jockeys. They like to see what they can do and they like to be speculative. And I tell them, “Have fun. Do that. But when it comes to managing your real wealth, let’s leave that to some professionals out there that stay in touch with what’s going on.”

Bette Hochberger:

What’s going on in reality?

Wealth Building the Right Way

Roy Esh:

Exactly. And make sure that you’re diversified and makes sure that things are invested appropriately. And we can also take advantage of, so here’s another thing by the way, that this is a testament to robo advisors, by the way, I didn’t mention, but there’s a concept called auto rebalancing. Now, auto rebalancing a portfolio is really important because if we determine that a client is a 70/30 allocation, 70% aggressive, 30% conservative. But let’s say that something that’s going on right now is the bond market, interest rates and all that are changing.

Roy Esh:

So there may be a rush into fixed income, and that can affect the equity market. So now your portfolio may be out of whack. Now you may not be a 70/30, according to how you should be. Now, you may be 60/40. So what auto rebalancing does is it takes all the emotion out of investing and it forces you to get back to 70.30. It forces you to buy low and sell high. And that’s how you make money in the market. You want to buy low, sell high. So the robo advisors have introduced the auto rebalancing feature. But then the question is, well, how often should you rebalance?

Bette Hochberger:

That’s what I was going to say, is that actually helpful to be constantly rebalancing? Because I think we do it once a quarter, maybe a couple of times a year, we’re not in there all the time rebalancing our own stuff. Is that really helpful?

Roy Esh:

Yeah. Quarterly is good. Semi-annually is good. Yeah.

Bette Hochberger:

Is it just creating a lot of movement for no real purpose? Not no purpose, but can it have downsides to doing it all the time like that?

Roy Esh:

Yeah. Too much frequent auto balancing in the wrong type of account with the wrong structure, if you’re just buying mutual funds, A share, mutual funds, that kind of thing, then that can create additional fees. So it would be smart to do that in something like a wrap account or something where there’s tax deferral. Where it’s a qualified account like IRAs and 401ks and that sort of thing.

Bette Hochberger:

You’re throwing out a lot of jargon. Hold on. You’re probably losing people. I know what half of those things are.

Roy Esh:

So tax deferral is a powerful thing, especially for those folks that are in high tax brackets. And if you’re rebalancing too frequently, then what can happen is you may create too many gains inside the portfolio. So what you want to be cognizant of is that in a tax deferred vehicle, have fun. Auto rebalance all day long. Buy, sell, be an active investor, mutual funds are great because they’re actively managed. So those are great to have.

Bette Hochberger:

And you don’t have to do it yourself, right? You get a mutual fund or other kinds of funds. You don’t personally have to know how to do that rebalancing. Some pro, maybe you or somebody else. I don’t know if that’s the kind of thing that you even do, or really dirty guys.

Roy Esh:

No, that’s a really good question. So we use the same software or we use the same mechanisms that a robo advisor would use for rebalancing portfolios. I was just bringing it up that a robo advisor, that’s a good use of robots, right? It’s used to kind of set it up and know that you have an agreement with your client, that you’re going to rebalance your portfolio. So we absolutely use software to do that. I mean, it would be painstaking to do that yourself. And one day when we have an advanced discussion, we can talk about tax loss harvesting, and that kind of thing. That’s more…

Bette Hochberger:

That’s the stuff I like to have those discussions in December.

Roy Esh:

Sure, sure, sure.

Bette Hochberger:

That’s probably actually a good thing to talk about in December. We’ll have to put it on the calendar, come back and talk about it later. Okay. So let’s see. What other kinds of things? Oh, you know what’s interesting though, kind of related to all that, what you were saying, and kind of tying it back to the Robin Hood? I’m in a lot of groups with other CPAs and I see people, tax repayers who are screaming Robin Hood, 1099, transactions that are 100 pages long because people are buying, selling nonstop. And they’re like, “We don’t know what to do with a 100 page 1099 of all these sale transactions.” And some of it affects your taxes. Some of it doesn’t. Wash sales in there if you’re really in and out of stuff. So yeah. It’s funny what people are, what they’re doing, and I think they’re going to have some unintended consequences of having really high tax preparation bills, because the CVA is going to be upset about it.

Roy Esh:

All I can say is, I’m really glad I’m not sitting in your seat and I’m much happier being in mine.

Bette Hochberger:

Yes. Probably. Maybe I should change careers at some point. Usually April 14, that’s when I’m crying and I say, “I’m never doing this again,” until next year. “I’m going to become a dog walker or something like that, where you don’t have this kind of stress.”

Roy Esh:

It’s a shame they don’t have the robo advisors or robots to beat people when they’re creating all that work for you, right? Maybe just send a robot over there, send the Roomba.

Bette Hochberger:

Beat people, run over their feet. I don’t know. Oh my goodness.

Roy Esh:

So I think that there are just a few areas we use AI and that sort of thing, because I mean really, as a hedge, if I were smart, I would tell you, “Oh no, AI is never going to take over what I do.” I would never say that because my crystal ball is just as foggy as everybody else’s. But as a hedge, I might just buy AI ETFs, something like that, right? So I’m going to continue to work in my business, but that’s just a thought.

Bette Hochberger:

Well you know what though? I think that is something you always have to worry about, because even though I don’t believe in my industry, the AI is really out to get me, it’s not going to take over. It’s so far from being really viable as a replacement, but it’s like, “Well, what can I do with that technology? Even if it’s not exactly that technology, how can I utilize other technology? So then instead of being replaced by it, it’s just another tool for me?”

Roy Esh:

Well, what’s interesting is CPA practices tend to get sold over time. So at some point you’re going to have an exit strategy, right? And yeah, it may be in 30 years, but at that point, you better hope that your asset, which is your business, right? You better hope that there’s a good resale value on it, right? Because there’s no reason why a robo advisor needs to buy your practice, right? Because what are they going to do? They’re just there to work, right? So I think that’s going to be something interesting that comes down, years from now. So we don’t have to worry about it just yet.

Bette Hochberger:

Hopefully when we’re retiring, worry about it then. Okay. Roy, you gave us so much great information. And I said in the beginning, we’ve known each other for a really long time. So I got to ask you a weird, put you on the spot question. Do you have any weird hobbies?

Roy Esh:

So this pandemic has opened my eyes to things that I enjoy that I didn’t think I would. So photography has actually become really interesting to me. I know it’s not that weird, but the weird part of what I am attracted to about photography is not taking pictures of leaves with insects on it or anything like that. That to me is not interesting, but I do like capturing people’s faces, right? I don’t know. There’s something about capturing a person and just seeing their face, and kind of encapsulating that moment of that person at that time, and then having it permanent. I don’t know. There’s something about that, that I like. And maybe it’s not that weird.

Bette Hochberger:

Portrait photographer?

Roy Esh:

Portrait photographer. Yeah. But I do not charge for it because it’s not a side hustle. It’s just something that I’m exploring that I’m getting into with lighting, and yeah. It’s cool. It’s fun. It’s a lot of fun.

Bette Hochberger:

Oh, I’ve had to learn a lot about lighting once I started all this online video stuff, because I was like, “Oh, you need this lighting. What color is it? Where’s the angle? Or is it shadows? It’s too bright, it’s too soft.” So yeah, it’s pretty complicated actually. It’s not the easiest.

Roy Esh:

Well you look great. Whatever you’re doing, keep it up.

Bette Hochberger:

Well, I appreciate it very much. Thank you so much. Do you have any last bits of advice for us?

Roy Esh:

I do. I do. So look, when it comes to technology, my take on it is that it’s sink or swim, right? Because if you’re still going to be doing paper applications in 10 years from now, I mean, people are going to lose faith in you. So, so I do believe it’s important to keep pace with technology. And if you are a financial advisor like me, hopefully the company that you hang your licenses with is keeping pace with technology. If they’re not, give me a call and I can tell you why I’m really happy where I am, but one last thing is that Warren Buffet had this old saying, and it’s, “When the tide rolls out, you can see who’s swimming without shorts on.” Right?

Roy Esh:

And it’s such a good way to explain, in these days, with COVID-19 and people are working from home, and you know who’s organized, you know who’s got their act together, and the way it works for act, right? You know who’s got their stuff together and who doesn’t. And I think that this is very much a trying time for people, but at the same time, it’s opportunistic. And that’s it. That’s all I wanted to leave you with. Just that one little nugget.

Bette Hochberger:

You say that though, because I had a call with somebody I met years ago, another CPA. He used to be in Florida, he’s gone. And he’s out of CPA practice, he’s now in industry now, but we had a call a few months back where we were saying that those of us, especially South Florida, we’re not the most tech savvy area. It’s not like San Francisco or New York or Boston, but those of us who have been in the cloud and paperless and everything online and really heavy with the tech, people used to look at us like we were those doomsday, tinfoil hat wearing freaks like, “The day is coming, there will not be paper anymore.” And here we are, COVID. I picked up clients because their CPA’s offices that were traditional brick and mortar, with the paper, and you come in, and you sit there while someone does your taxes, they shut down. They were shut down, not answering phones, not returning calls. And I was like, “All right, well, come to me.”

Bette Hochberger:

And it totally, totally ended up working out in my favor that all those years of being like, “I do everything online,” where people think you’re weird, now everyone caught up to me. So it’s definitely evolve or die. One or the other. Evolve or die. Fantastic. All right. Well, Roy, it has been fantastic having you on. We’re going to put your contact information, whatever info you want, we’ll drop it in here, and definitely have to have you on again. We got to rebalance some loss harvesting and whatever later in the year, we will do it. So, awesome. Thank you. And we will see you all next week.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}