VC funding transforms your startup’s financial landscape, but it also creates complex tax obligations that many founders overlook. The equity grants, timing of income recognition, and multi-state operations introduce challenges that require strategic planning.

At Bette Hochberger, CPA, CGMA, we’ve seen firsthand how the right VC funded taxation strategies can save startups thousands in unnecessary taxes while keeping them compliant. This guide walks you through the essential tax considerations every venture-backed company needs to understand.

What VC Funding Does to Your Tax Situation

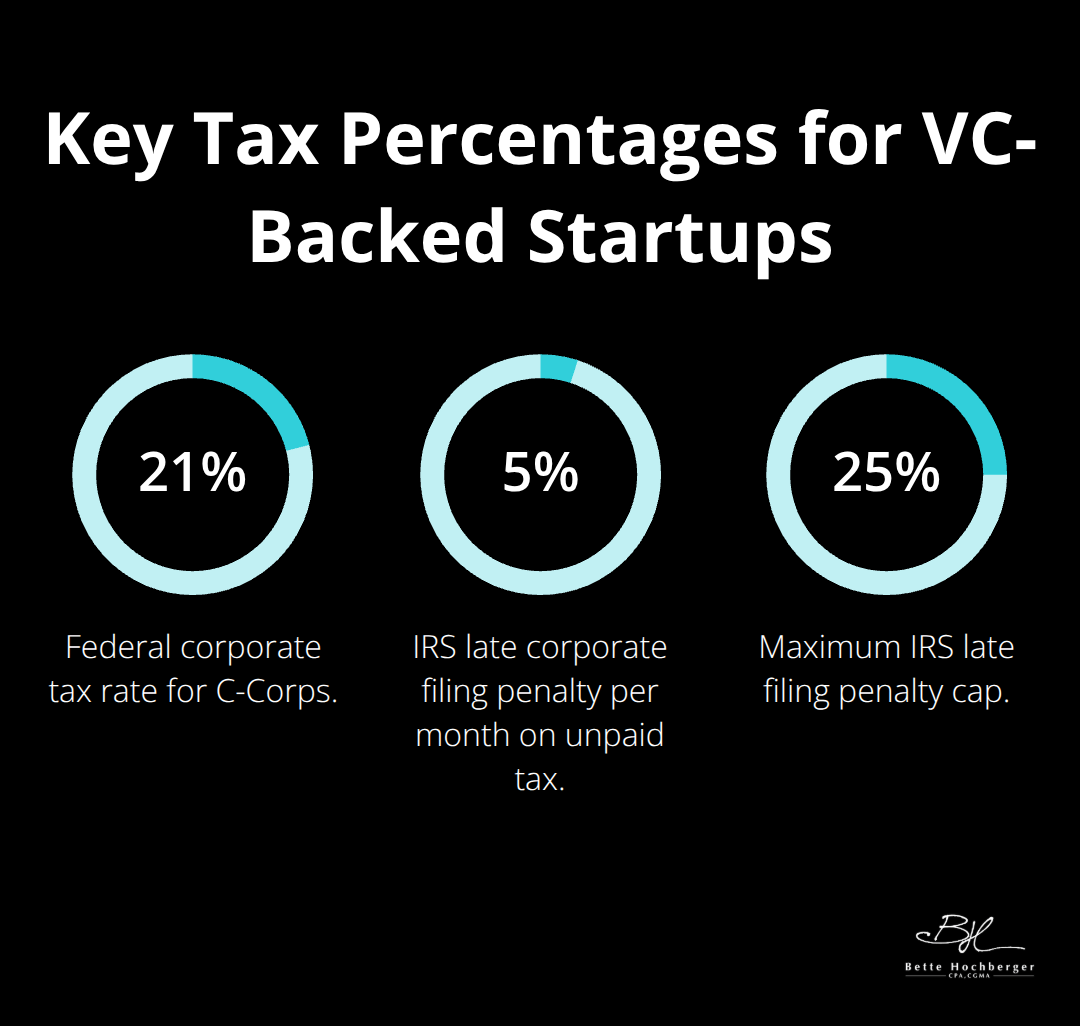

VC funding creates immediate tax consequences that most founders don’t anticipate until they’re filing their first return. The moment you accept investment, your startup’s tax position shifts dramatically across federal, state, and payroll obligations. The federal corporate tax rate for C-Corps sits at 21%, which shapes every decision about when to recognize income and which deductions to claim.

If you’re paying yourself and employees, you now manage payroll taxes across potentially multiple states, each with different filing deadlines and rates. Many startups treat tax planning as an afterthought-something to handle once revenue appears. This approach costs you thousands in missed R&D tax credits and unnecessary state filings. The R&D payroll tax credit alone can reach up to $500,000 per year for qualified small businesses, according to IRS Form 6765. Yet founders skip this credit entirely because they don’t connect their engineering work to tax law.

The Hidden Tax Impact of Equity Grants

Your equity grants and stock options introduce another layer of complexity that affects both your personal and corporate tax situation. An 83(b) election filed within 30 days of purchasing founder stock allows you to save a substantial amount of taxes on restricted stock. Without this election, you pay ordinary income tax on gains that should qualify as long-term capital gains.

Equity Compensation Requires Immediate Action

Equity compensation isn’t just a financial reward-it’s a tax event that demands planning before your first hire. When you grant stock options or restricted stock units, you create tax obligations for your employees that start the day they vest. If your employees are classified as contractors instead of W-2 employees, the IRS scrutinizes this decision heavily.

The Department of Labor considers behavioral controls, financial controls, and the nature of the relationship when determining worker classification. Misclassification exposes you to back taxes, interest, and penalties that can drain your runway. Establish a proper payroll system from day one, even if you’re pre-revenue. This prevents the costly mistakes of incorrect withholdings and multi-state compliance failures.

QSBS Status and Long-Term Wealth Building

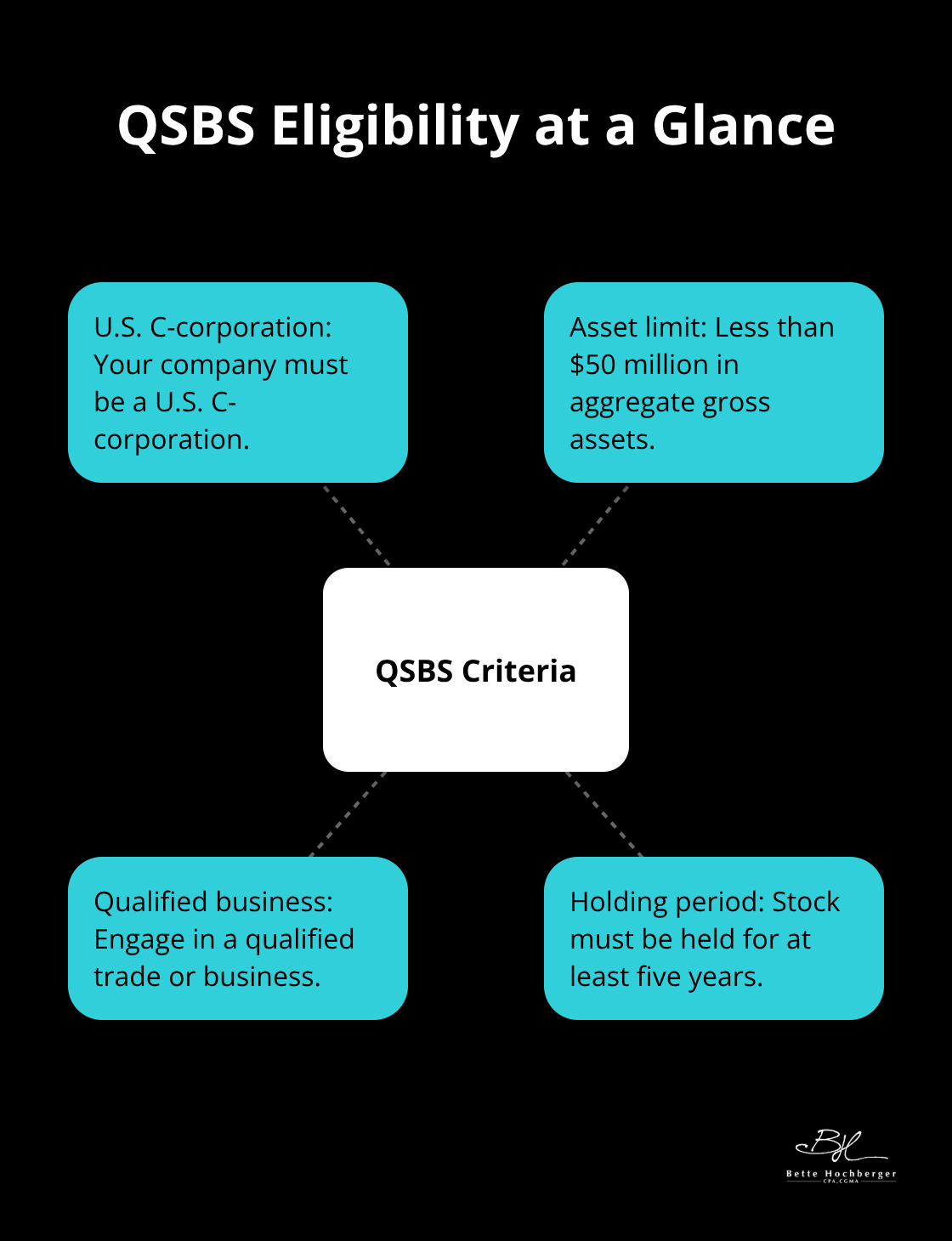

For your equity grants, Qualified Small Business Stock (QSBS) status matters enormously if your company qualifies. Your business must be a U.S. C-corporation with less than $50 million in aggregate gross assets, engaged in a qualified trade or business, and held for at least five years. Most early-stage tech startups meet these criteria during their early years.

If you hit these requirements, you can exclude up to $10 million in capital gains federally after the five-year holding period-a benefit that applies to founders and investors alike. This tax advantage compounds significantly as your company grows, making the five-year holding period a critical milestone in your exit strategy. Understanding whether your startup qualifies for QSBS treatment now shapes every decision you make about equity structure and investor communications moving forward.

Strategic Tax Planning for VC-Backed Companies

Timing your income recognition and deductions isn’t about moving numbers around on a spreadsheet-it’s about controlling cash flow and preserving capital during your growth phase. Most VC-backed startups operate as C-Corps at the 21% federal rate, which means every dollar you recognize as income gets taxed immediately. The key is understanding when to accelerate deductions and when to defer income recognition strategically.

Income Deferral and Acceleration Tactics

If you plan to raise another funding round within the next 18 months, deferring taxable income into the following year can reduce your current-year tax bill and preserve runway for that raise. Conversely, if you’ve had an unexpectedly profitable year and won’t raise again soon, accelerate deductible expenses like equipment purchases or professional services into the current year to offset that income. This approach requires you to track your fundraising timeline closely and coordinate with your accounting team.

Maximizing R&D Tax Credits

The R&D tax credit deserves special attention because it directly reduces your tax liability dollar-for-dollar, not just your taxable income. Maximizing R&D Tax Credits allows qualified businesses to claim credits for research and development activities. This includes work on design improvements, testing protocols, and process optimization-not just pure engineering. Document your R&D activities throughout the year rather than reconstructing them during tax season, when details fade and the IRS becomes skeptical of inflated claims.

Entity Structure and Its Tax Consequences

Your entity structure decision affects everything that follows, and changing it later creates unnecessary complexity. If you incorporate as a C-Corp, you lock into the 21% federal rate, but you gain flexibility in timing distributions and can preserve retained earnings for future growth without triggering personal income tax. An S-Corp election rarely makes sense for early-stage VC-backed startups because investors typically require C-Corp status for QSBS eligibility and investor protections.

Managing Multi-State Tax Obligations

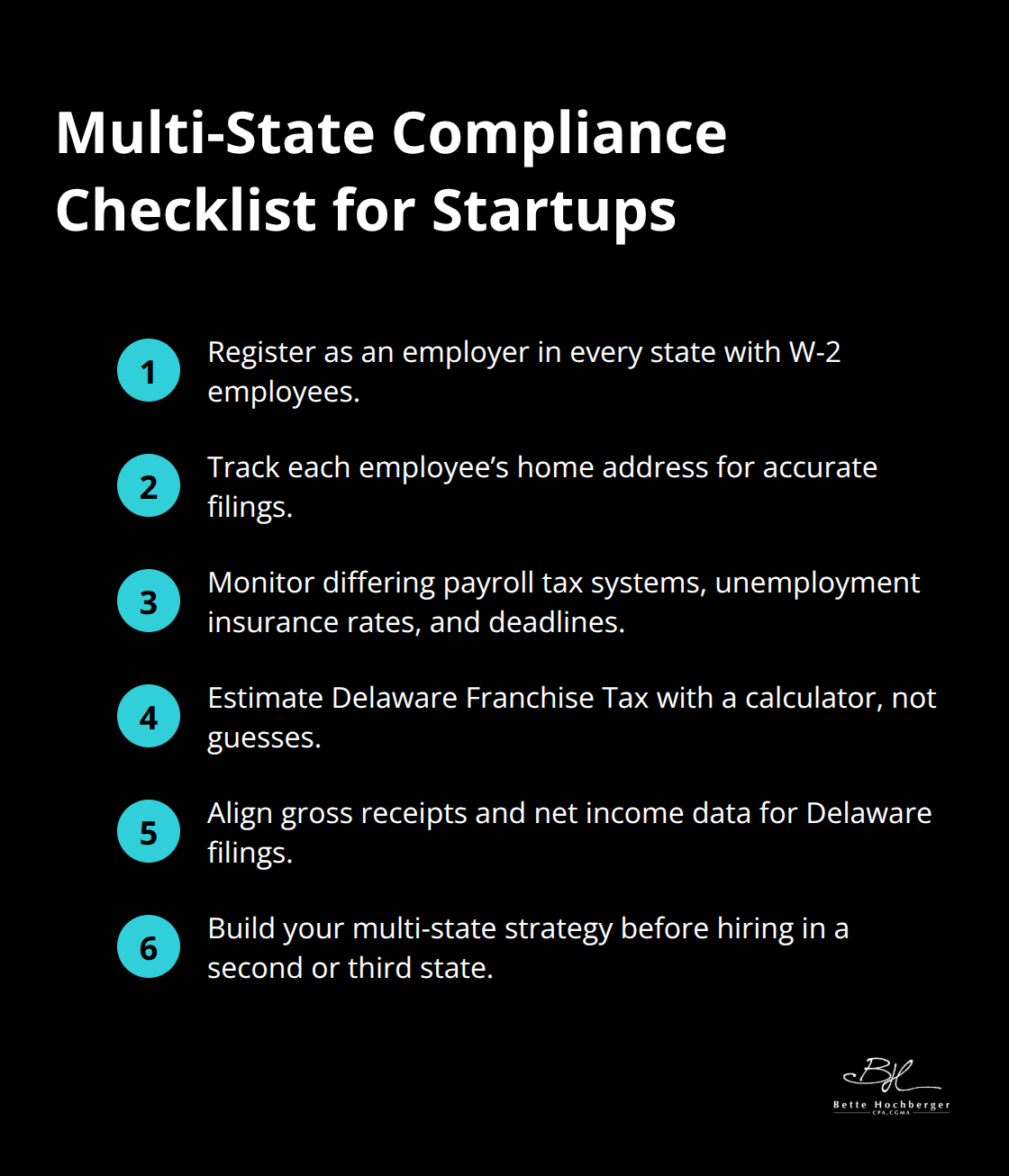

Once you operate across multiple states, your tax obligations explode across jurisdictions. You must register as an employer in every state where you have W-2 employees and track their home addresses to file correctly-missing this step triggers state penalties that compound quickly. Delaware Franchise Tax becomes a common cost if you incorporate there, but the actual liability depends on your gross receipts and net income calculations, which vary annually. Use a Delaware Franchise Tax calculator to estimate your obligations rather than guessing.

If you have employees in California, New York, and Texas simultaneously, you manage three different payroll tax systems, unemployment insurance rates, and filing deadlines. Multistate nexus planning isn’t optional-it’s a survival requirement that prevents double taxation and costly penalties. Establish your multi-state tax strategy before your second or third state hire, not after you’ve already created compliance gaps that require amended filings and back-payment arrangements. This foundation positions you to handle the documentation and record-keeping demands that accelerate as your startup scales.

Building Tax Compliance Into Your Growth Timeline

Tax Deadlines That Demand Immediate Attention

As your startup scales, tax compliance transforms from an occasional task into a permanent operational requirement that directly impacts your ability to raise capital and execute exits. The IRS penalty for late corporate tax filings reaches 5% of unpaid tax per month up to 25%, which means a single missed deadline costs thousands in penalties alone before you address the underlying tax liability. Growth-stage startups must establish a compliance calendar that treats tax deadlines with the same urgency as payroll. Form 1120 for C-Corps is due April 15, while Form 1120-S for S-Corps is due March 15, creating different deadlines depending on your entity structure. Missing these dates signals to investors during due diligence that your financial operations lack discipline.

Quarterly Estimated Tax Payments and Underpayment Penalties

Your quarterly estimated tax payments under Form 1040-ES determine whether you face underpayment penalties at year-end. The IRS calculates these penalties based on the difference between what you actually paid and what you should have paid, compounding the cash flow pressure during months when you manage payroll, contractor payments, and operational expenses simultaneously. Underpayment penalties accumulate quickly if you underestimate your tax liability, so accuracy matters far more than conservative estimates that leave you with refunds.

Real-Time Bookkeeping Systems That Prevent Disasters

Practical compliance begins with a centralized system that tracks every tax obligation across your organization. Cloud-based accounting tools like QuickBooks or Xero allow you to record transactions in real-time rather than reconstruct them months later, which dramatically improves accuracy and reduces audit risk. Your bookkeeping process must separate business and personal funds entirely-commingling accounts voids liability protection and triggers IRS reclassifications that expose you to unexpected tax bills. Establish these systems before you hire your third employee, not after you’ve already created gaps that require amended filings and back-payment arrangements.

Documentation That Protects Your R&D Credits

Document your R&D activities throughout the year by recording which team members worked on qualifying projects, what problems they solved, and how the work improved your product or process. This contemporaneous documentation becomes your defense if the IRS questions your R&D credit claims, which they scrutinize heavily. Collect W-9 forms from every vendor at onboarding and maintain them on file because you must report 1099-NEC payments of $600 or more by January 31. If you operate across multiple states with W-2 employees, register as an employer in every jurisdiction and track each employee’s home address to avoid state filing errors that trigger penalties and compliance headaches.

Multi-State Compliance and Year-Round Readiness

Your goal is to maintain year-round tax readiness rather than scramble in March or April when deadlines arrive and your fundraising timeline collides with compliance obligations. Multi-state operations require you to file payroll taxes, unemployment insurance, and income tax returns across jurisdictions with different rates and deadlines. The complexity multiplies when you have employees in California, New York, and Texas simultaneously-you manage three different payroll tax systems that operate on separate schedules. Establish your multi-state tax strategy before your second or third state hire, not after you’ve already created compliance gaps that demand amended filings and back-payment arrangements.

Final Thoughts

VC funded taxation strategies succeed when you treat tax planning as a core business function, not a compliance checkbox you handle once yearly. The decisions you make today about entity structure, equity grants, and multi-state operations compound over years and directly impact your ability to raise capital and execute a successful exit. Founders who delay tax planning until they’re mid-fundraise or preparing for acquisition face rushed decisions, missed credits, and compliance gaps that slow due diligence and reduce valuation.

The R&D tax credit alone demonstrates why proactive planning matters-qualified small businesses claim up to $500,000 annually in payroll tax credits, yet most startups leave this money on the table because they don’t connect their engineering work to tax law. Understanding QSBS eligibility early allows you to structure equity grants and investor rounds strategically, potentially excluding millions in capital gains after your five-year holding period. These aren’t theoretical benefits; they’re real dollars that stay in your company or your pocket instead of flowing to the IRS.

We at Bette Hochberger, CPA, CGMA work with VC-backed startups to build tax strategy into your growth timeline before complexity overwhelms your team. Our approach combines strategic tax planning with fractional CFO services to manage cash flow and minimize tax liabilities as you scale. The right guidance now prevents costly mistakes later and positions your startup for a smoother fundraising process and exit.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}