Short-term rental taxes are one of the most misunderstood areas of tax law for property owners. Many hosts miss deductions worth thousands of dollars each year simply because they don’t know what qualifies.

At Bette Hochberger, CPA, CGMA, we’ve helped countless rental property owners navigate these rules and reduce their tax burden. This guide covers the deductions you can claim, the compliance mistakes to avoid, and how proper record-keeping protects you.

Understanding Short-Term Rental Income and Tax Obligations

What the IRS Actually Counts as Rental Income

The IRS doesn’t care what platform you use or how casually you started hosting. If you rent a property for more than 14 days per year, you must report income. The 14-day threshold under IRC Section 280A marks the hard line. Rent for 14 days or fewer and use the property personally for more than the greater of 14 days or 10% of rental days, and you owe nothing on that income. Cross that threshold, and the IRS expects a Form 1040 with Schedule E attached.

The IRS tracks rental income through 1099-K forms when gross payments exceed $20,000 and you have more than 200 transactions, or through 1099-NEC forms for income over $600 from a single platform. Platforms like Airbnb and VRBO report directly to the IRS, so underreporting carries real risk. Hosts caught off guard every year fail to realize that 15 days of rental activity triggers full reporting obligations.

How the IRS Classifies Your Rental Activity

The way you classify your rental activity determines your tax burden. If you provide substantial services-daily cleaning, concierge, meals, tours, or guest assistance-the IRS treats this as a trade or business on Schedule C, which means self-employment tax applies. If you provide minimal services like heating, water, or basic cleaning between guests, you report on Schedule E with no self-employment tax. This distinction matters because Schedule C can add 15.3% to your tax bill through self-employment tax on net income.

Material participation tests shift how losses flow through your return. If you pass one of seven IRS tests-working more than 500 hours annually, performing substantially all the work yourself, or meeting other participation thresholds-losses can offset non-passive income instead of remaining trapped on your rental schedule. Most hosts fail these tests because they don’t track hours or document participation properly.

The average stay length also triggers different rules. Properties with stays averaging seven days or less can qualify for non-passive treatment if you materially participate, while 30-day averages allow business treatment with substantial services. You must calculate your actual average stay from your booking records to determine which rules apply to your situation.

State and Local Tax Compliance Isn’t Optional

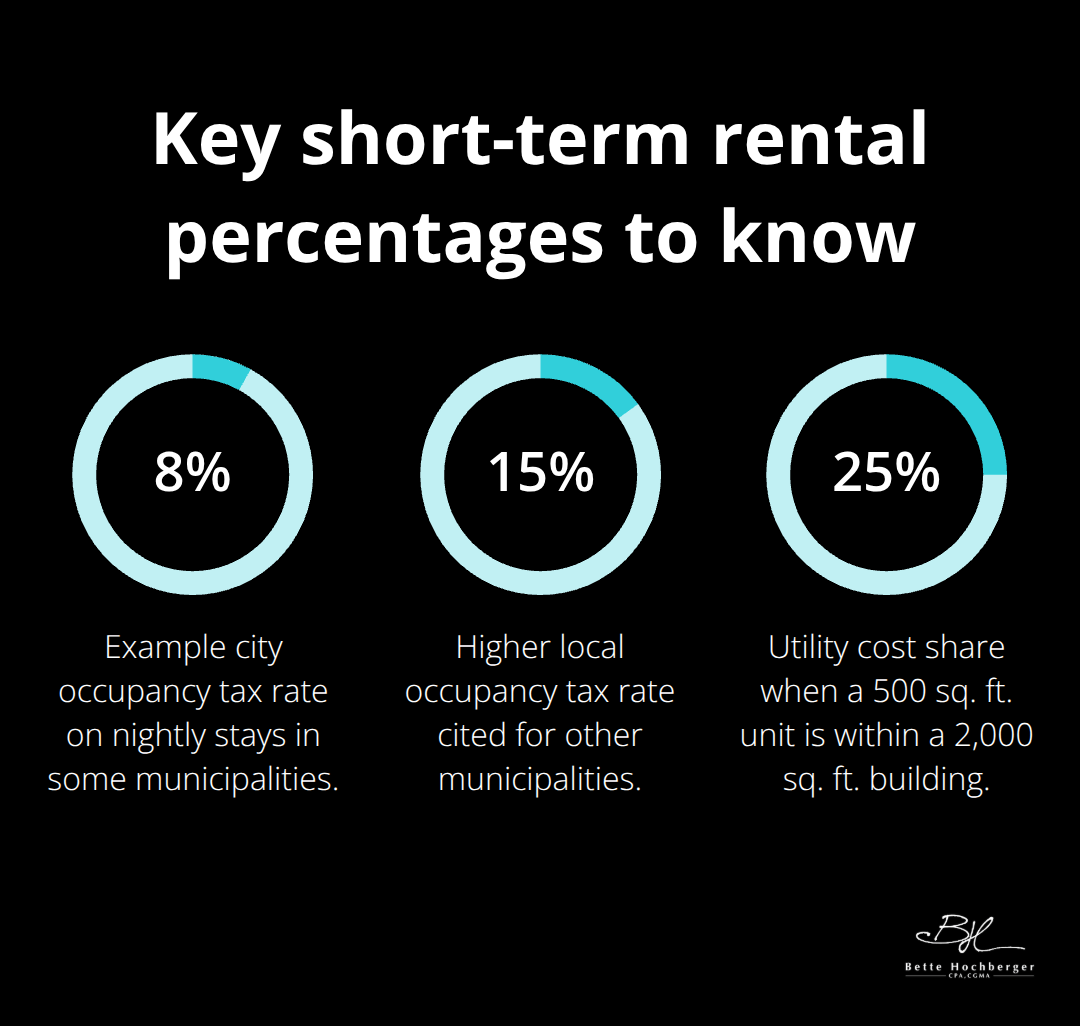

State and local occupancy taxes are separate from federal income tax and vary dramatically by location. Some municipalities tax nightly rates at 8%, others at 15% or higher. Many hosts ignore these because platforms don’t automatically remit them in all jurisdictions. You remain responsible for calculating, tracking, and paying these taxes quarterly or monthly depending on local rules.

Research your specific municipality before listing-some areas ban short-term rentals entirely, others require permits costing hundreds of dollars annually. Many cities have specific laws governing short-term rentals, including licensing requirements, zoning restrictions, and tax obligations. UK hosts face additional complexity as HMRC now requires platforms to report hosting earnings directly starting in 2025, with hosts declaring income in Self Assessment tax returns. The personal allowance sits at £12,570, with basic rate tax at 20% on income up to £50,270. Furnished Holiday Lettings status was abolished in April 2025, so most UK hosts now treat income as standard residential rental income with different relief options available.

Missing these local requirements invites penalties far exceeding the tax owed. Document your jurisdiction’s specific rules in writing and set calendar reminders for payment deadlines. Understanding these obligations sets the foundation for identifying which deductions you can actually claim against your rental income.

Key Deductions for Short-Term Rental Owners

Mortgage Interest, Property Taxes, and Insurance

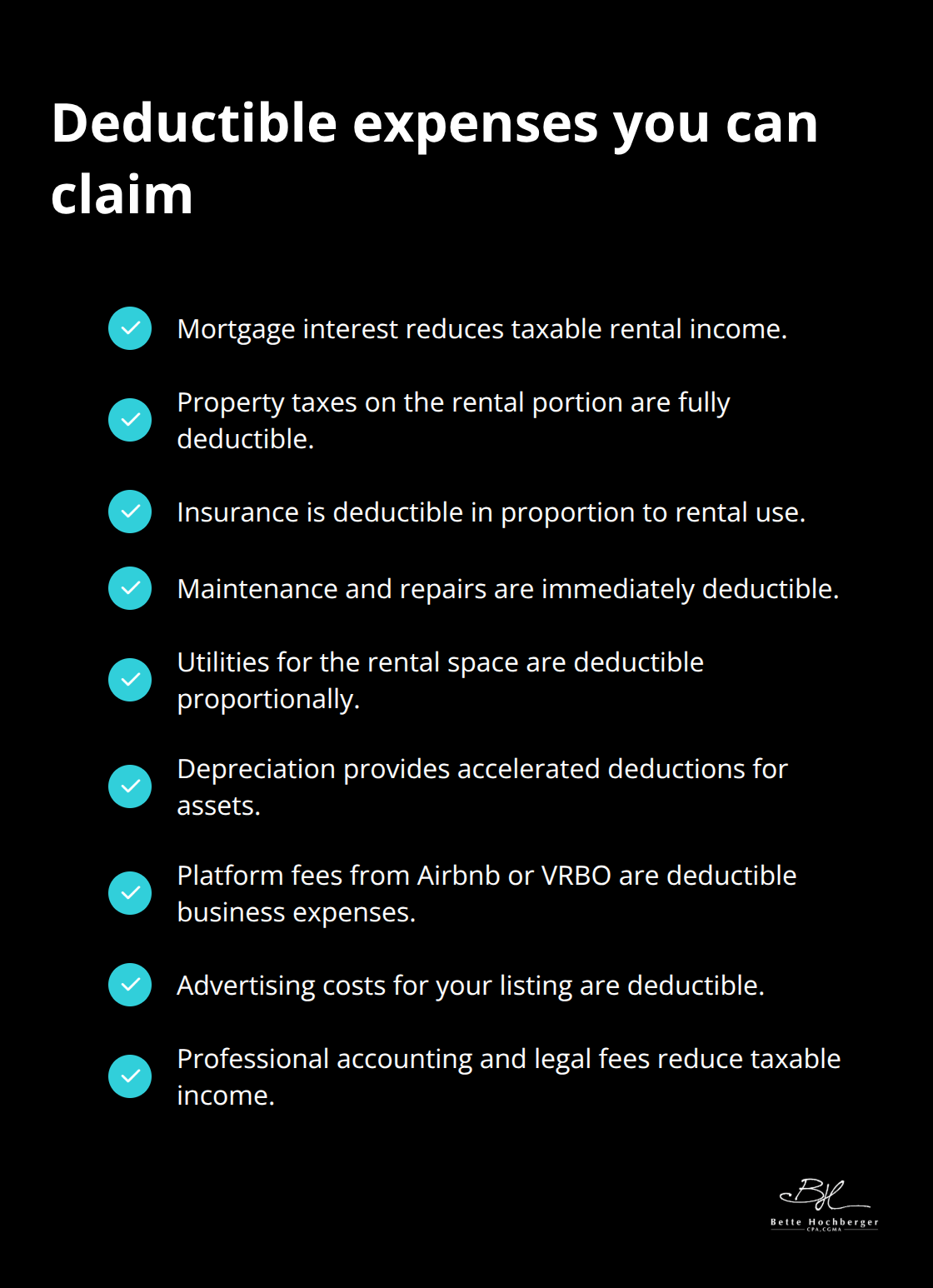

Mortgage interest stands apart from mortgage principal because only the interest portion reduces your taxable rental income. The IRS requires you to separate these on your tax return. Many hosts claim the full payment as a deduction, inflating their write-offs and triggering audits. Pull your annual mortgage statement, which itemizes interest paid, and use that exact figure.

Property taxes on the rental portion are fully deductible whether you own the entire building or rent a single room. If you rent one bedroom in your home, apportion property taxes by dividing the rental square footage by total square footage, then claim that percentage. Insurance follows the same logic-a homeowners policy covering your entire property costs perhaps $1,200 annually. If 30% of your home is rented, you deduct $360 against rental income. This apportionment applies to any shared expense between personal and rental use.

Maintenance, Repairs, and Utilities

Maintenance and repairs are immediately deductible in the year you pay them, while improvements are capitalized and claimed over time. Replacing a broken toilet qualifies as a repair. Renovating the entire bathroom qualifies as an improvement. Repainting walls between guests counts as maintenance. Installing new electrical wiring counts as an improvement. The line matters because repairs save you thousands in immediate deductions while improvements stretch benefits across years through depreciation.

Utilities tied to rental use are deductible. Electricity, gas, water, and internet for the rental space reduce taxable income proportionally. If your unit is 500 square feet within a 2,000 square foot building, claim 25% of utility costs. Cleaning supplies, guest consumables like towels and bedding, welcome baskets, and professional cleaning between stays all count as deductible expenses.

Depreciation and Equipment

Depreciation accelerates tax benefits significantly. Under current law, bonus depreciation allows 100% immediate deduction for qualifying property acquired after January 19, 2025. Furnishings, appliances, and equipment used in the rental qualify for accelerated deductions. A $10,000 furniture package generates substantial first-year tax savings when properly classified. Cost segregation analysis pushes this further, allocating portions of your property to shorter depreciation schedules.

Operating Expenses and Professional Fees

Platform fees from Airbnb or VRBO are fully deductible business expenses. These reduce your net income dollar-for-dollar. Advertising costs for your listing are deductible. Professional fees for accounting and legal services related to your hosting business reduce taxable income.

Maintain separate records for each expense category and track dates carefully. The IRS expects documentation supporting every deduction you claim.

These deductions form the foundation of your tax strategy, but claiming them correctly requires meticulous tracking. The next section addresses the compliance mistakes that cost hosts thousands in missed deductions and unnecessary penalties.

Common Compliance Mistakes and How to Avoid Them

The Personal-Use Day Trap

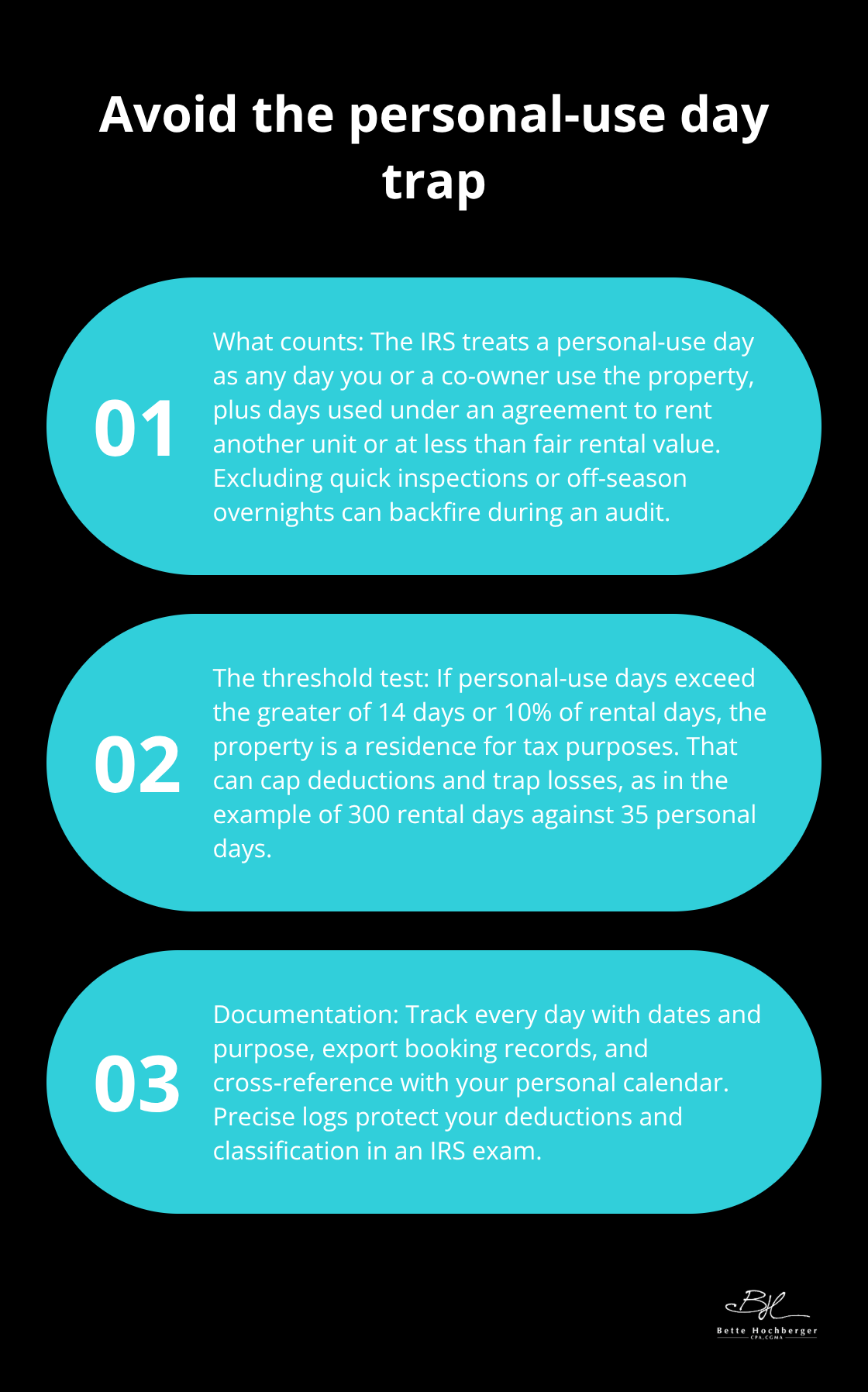

The personal-use day calculation is where most hosts sabotage their own tax returns without realizing it. The IRS counts a personal-use day as any day you or a family member with an ownership interest occupy the property, plus any day someone uses it under an agreement to rent another unit or at less than fair rental price. Many hosts mentally exclude quick inspections or overnight stays during off-season, then face audits when their records don’t match their tax filing. A single miscalculation here can flip your entire property classification from rental to residential, capping your deductions and trapping losses on your return.

The personal-use threshold is straightforward: if personal-use days exceed the greater of 14 days or 10% of your rental days, the property qualifies as a residence. This means your deduction for expenses exceeds your gross rental income gets limited. If you rented 300 days and used the property personally 35 days, you crossed the 10% threshold. Your mortgage interest and property taxes still get deducted on Schedule A if you itemize, but maintenance, repairs, utilities, and depreciation become subject to the gross rental income limitation. This single mistake costs hosts thousands annually.

Track every single day in a spreadsheet or calendar app with dates and purpose noted. When the IRS audits, they want documentation proving your personal-use count. Most platforms show booking dates automatically, so export your rental records and cross-reference them against your personal calendar. If you maintain a second property exclusively for rental, this becomes irrelevant, but mixed-use properties demand precision.

Documentation and Expense Tracking

Expense tracking failures create significant compliance disasters. Hosts who treat their rental as a trade or business under Schedule C owe quarterly estimated taxes on Form 1040-ES. Missing even one quarter triggers a penalty, regardless of whether you ultimately owe taxes.

Expense documentation requires receipts for every deduction, organized by category: mortgage statements showing interest paid separately, utility bills, cleaning invoices, platform fees, and repair receipts. Digital record-keeping from day one matters enormously. Use a spreadsheet or accounting app to log each expense with the date, vendor, amount, and category as it occurs, not months later when details blur. When audited, the IRS examines whether your records corroborate your deductions. A cleaning expense claimed without a receipt or vendor name raises red flags. A mortgage interest deduction that doesn’t match your lender’s annual statement triggers deeper scrutiny.

Quarterly Tax Payment Obligations

Set up automatic transfers to a separate savings account each month equal to roughly 25-30% of rental income after expenses, then pay quarterly on April 15, June 15, September 15, and January 15. This approach prevents the scramble to find funds when payment deadlines arrive and eliminates the penalties that accumulate when you miss quarters. Maintain both digital and physical copies of receipts for three years minimum, organized by tax year and expense category. This documentation protects you when the IRS questions your return and accelerates the tax preparation process each year.

Final Thoughts

Short-term rental taxes demand attention to three core areas: understanding your federal and state obligations, claiming every deduction you qualify for, and maintaining documentation that withstands IRS scrutiny. The difference between hosts who pay thousands in unnecessary taxes and those who minimize their burden comes down to execution on these fundamentals. State and local occupancy taxes, quarterly estimated payments, and personal-use day calculations create a compliance framework that catches unprepared hosts.

The deductions available to you are substantial-mortgage interest, property taxes, insurance, repairs, utilities, depreciation, and operating expenses reduce your taxable income significantly. Record-keeping separates successful rental property owners from those who leave money on the table. A spreadsheet tracking rental days, personal-use days, and every expense by category takes hours to set up but saves you thousands when tax time arrives, and digital documentation of receipts, platform fees, utility bills, and repair invoices protects you if the IRS questions your return.

Working with a tax professional transforms your rental operation from a compliance headache into a strategic asset. We at Bette Hochberger, CPA, CGMA help rental property owners navigate these rules, identify deductions they miss, and structure their operations for maximum tax efficiency. Our team handles strategic tax planning and preparation designed to minimize your tax liability while keeping you compliant with short-term rental taxes regulations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}