Most people leave thousands of dollars on the table by not optimizing their capital gains tax strategy. The difference between holding an asset for one year versus eleven months can mean paying significantly higher tax rates.

At Bette Hochberger, CPA, CGMA, we’ve helped clients reduce their tax liability through smart timing, strategic asset donations, and advanced planning techniques. This guide walks you through the specific tactics that work.

How Tax Rates Actually Work in 2026

Short-Term Versus Long-Term: The Rate Difference That Matters

The IRS treats short-term and long-term capital gains completely differently, and this distinction matters more than most investors realize. Short-term gains, which apply to assets held one year or less, get taxed at your ordinary income rate. If you sit in the 35% federal tax bracket, every dollar of short-term gain faces 35% taxation. Long-term gains, held over one year, qualify for preferential rates of 0%, 15%, or 20% depending on your income level. For 2026, married couples filing jointly can earn up to $98,900 of taxable income and pay zero federal tax on long-term gains. The next tier runs up to $613,700 at the 15% rate, with anything above that taxed at 20%. Single filers get tighter thresholds: the 0% bracket tops out at $49,450, the 15% bracket extends to $306,850.

The number 0% seems to be not appropriate for this chart. Please use a different chart type.

This structure alone explains why waiting eleven months instead of nine months to sell an asset can save thousands in taxes. The gap between 35% and 15% on a $100,000 gain equals $2,000 in federal tax alone. Understanding how capital gains tax works helps you time asset sales strategically.

State Taxes Compound Your Federal Bill

State capital gains taxes add a real burden that many investors overlook. Nine states impose no capital gains tax at all, but most states tax gains as ordinary income, layering on another 5% to 13% depending on where you live. Washington state introduced a 7% capital gains tax starting in 2025, with a 9.9% rate on gains exceeding $1 million. High earners in California or New York face combined federal and state rates exceeding 50% on short-term gains.

The Net Investment Income Tax Layer

The high-income Net Investment Income Tax of 3.8% applies to investment income for single filers earning over $200,000 and married couples over $250,000, adding another layer of cost. A $500,000 gain generates $50,000 in NIIT alone before state taxes apply. Location and timing decisions compound significantly when you factor in these layers.

The difference between a gain taxed at 15% plus state tax versus 35% plus state tax plus NIIT can easily reach six figures on substantial asset sales. Understanding which tax brackets apply to your specific situation requires mapping out your income, filing status, and state residency. This analysis determines whether you should accelerate or defer asset sales into the following year.

How to Profit From Losses and Strategic Timing

Tax-loss harvesting Offsets Gains

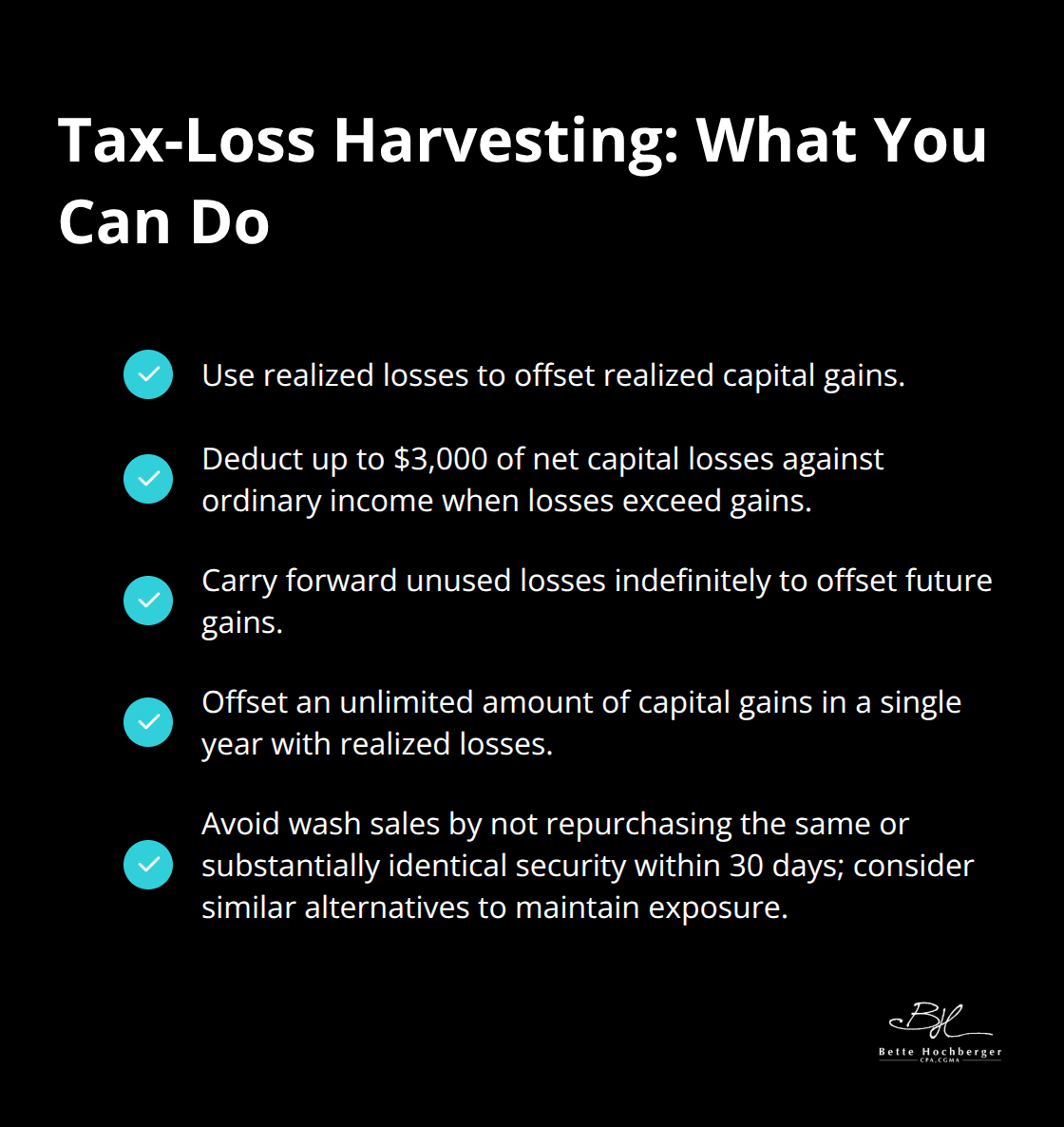

Tax-loss harvesting ranks among the most underutilized weapons in your capital gains toolkit, and the math is straightforward. When you sell an investment at a loss, that loss offsets capital gains. If losses exceed gains in a year, you deduct up to $3,000 against ordinary income, then carry forward the remaining losses indefinitely to future years. The IRS allows you to offset an unlimited amount of capital gains in a single year with realized losses, making this strategy particularly powerful when you hold a concentrated position with substantial gains.

A client holding a $500,000 gain alongside a $200,000 loss in underperforming investments can eliminate tax on $200,000 of that gain, potentially saving $30,000 in federal tax alone at the 15% long-term rate. The wash-sale rule blocks you from purchasing the same or substantially identical security within 30 days before or after the loss sale, but you can immediately purchase a similar competitor stock or fund to maintain market exposure.

Direct Indexing Makes Loss Harvesting Systematic

Direct indexing, where you own individual stocks instead of a mutual fund, makes systematic loss harvesting feasible throughout the year rather than only at year-end, since you control which specific shares to sell. This approach transforms capital gains management from an annual event into an ongoing process. You identify underperforming positions, realize losses when they occur, and maintain your desired market exposure through strategic replacements.

Holding periods Determine Your Tax Rate

Holding periods determine tax brackets more than most investors realize, and the difference between short-term and long-term treatment justifies waiting. An asset held short-term faces ordinary income rates up to 37%, while the same asset held long-term qualifies for the 0%, 15%, or 20% long-term rates. For married couples, staying under $98,900 of taxable income in 2026 means zero federal tax on long-term gains, making it worth timing sales to stay in that bracket.

Charitable Donations Eliminate Capital Gains Tax Entirely

Donating appreciated assets held longer than one year to charity solves the capital gains problem entirely while generating a deduction at fair market value. If you own stock worth $100,000 with a $30,000 cost basis, selling it triggers $30,000 in taxable gain, but donating it to charity avoids the $4,500 tax bill at 15% and lets you deduct the full $100,000 fair market value. Donor-advised funds simplify this approach by accepting your appreciated stock, avoiding capital gains immediately, then distributing to charities over time on your schedule.

This strategy works especially well for concentrated positions in company stock or real estate where you want to diversify without triggering massive tax bills. The combination of loss harvesting, strategic timing, and charitable giving creates a powerful framework for managing gains, but these tactics only work when coordinated with your overall income picture and long-term wealth goals. Advanced planning strategies-including trusts, gifting structures, and basis step-ups-extend these concepts further and address more complex situations.

When Your Assets Pass to the Next Generation

The Step-Up in Basis: Your Heirs’ Tax Shield

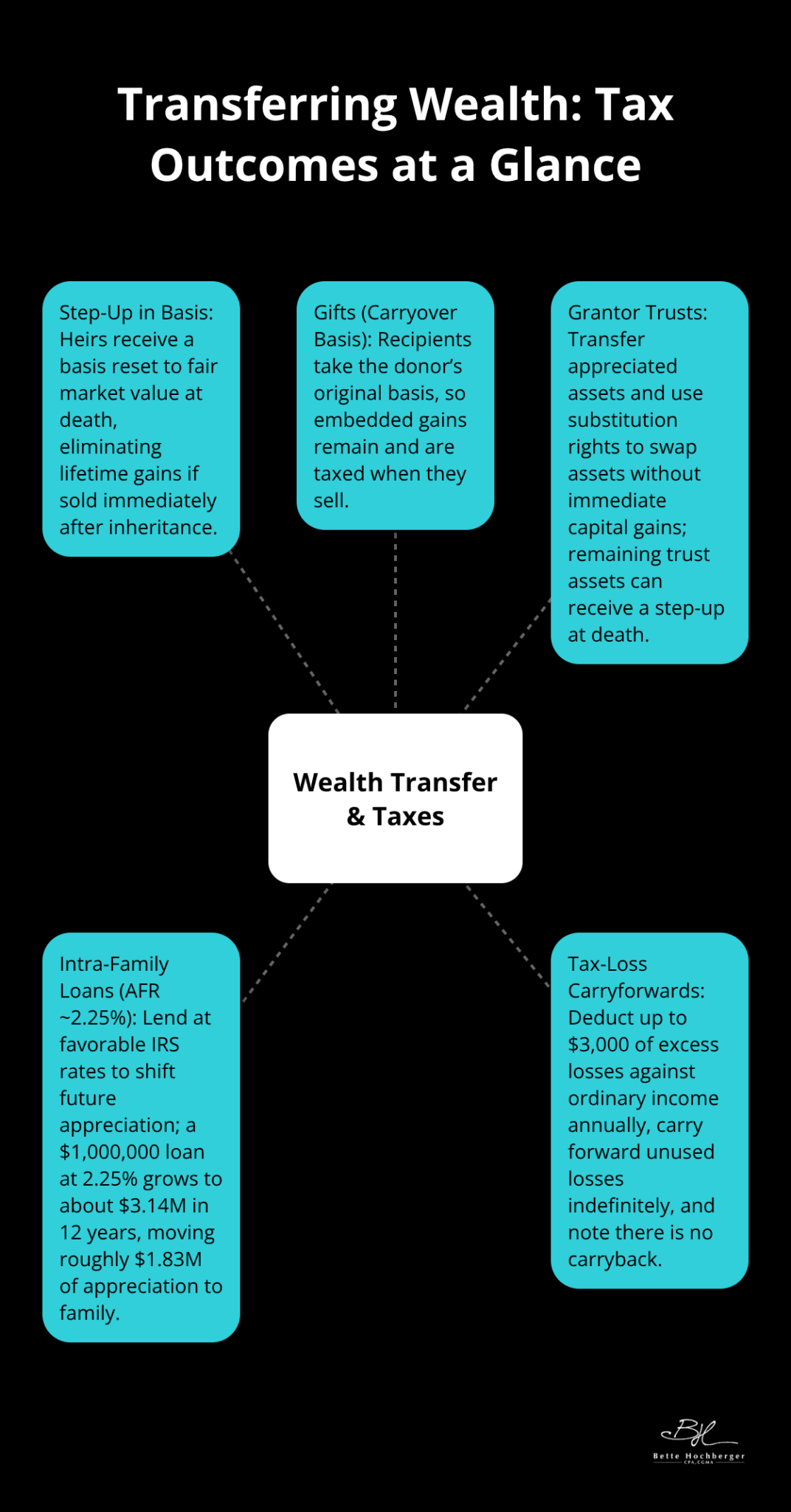

The step-up in basis at death represents one of the most powerful tax advantages available, yet most people never plan for it intentionally. When you inherit an asset, the IRS resets your cost basis to its fair market value on the date of death, eliminating all accumulated gains from the original owner’s lifetime. A stock purchased for $50,000 that grows to $500,000 triggers zero capital gains tax for your heirs when they inherit it and sell it immediately at that stepped-up basis. This mechanism alone makes holding appreciated assets until death financially superior to selling them during your lifetime in many situations, particularly for real estate and concentrated stock positions.

Gifts Transfer Your Tax Problem to Recipients

This advantage only applies to inherited assets, not to gifts made while you’re alive. Gifts transfer your original cost basis to the recipient, meaning they inherit your tax problem along with the asset. A $500,000 gain on gifted stock remains a $500,000 gain for the recipient, taxed at their rates when they eventually sell. The distinction between dying and gifting fundamentally changes the tax outcome, making the decision about when to transfer wealth extraordinarily consequential.

Grantor Trusts and Substitution Rights

Advanced structures like grantor trusts let you shift wealth tax-efficiently while you’re alive, though they require careful structuring to work properly. A grantor trust allows you to transfer appreciated assets into a trust while maintaining control through substitution rights, enabling you to swap appreciated assets for cash without triggering capital gains immediately. When you die, heirs receive a stepped-up basis on the remaining trust assets, preserving the tax benefit. These strategies work best when coordinated with your overall estate plan and income picture, making professional guidance essential to avoid missteps.

Intra-Family Loans at Favorable Rates

Intra-family loans using the IRS Applicable Federal Rate (currently around 2.25% for long-term loans) allow you to loan money to family members at favorable rates while shifting future appreciation to them tax-free. A $1 million loan at 2.25% grows to approximately $3.14 million in twelve years, with roughly $1.83 million of appreciation transferring to your family without gift tax consequences. This approach converts what would otherwise be taxable income into a family wealth transfer mechanism.

Tax-Loss Carryforwards Extend Your Deductions

Tax-loss carryforwards provide flexibility when harvesting losses exceeds gains in any single year, letting you deduct up to $3,000 of excess losses against ordinary income annually while carrying unused losses forward indefinitely to offset future gains. This carryforward mechanism transforms a challenging year with large losses into a multi-year tax advantage, particularly valuable when you realize substantial gains in subsequent years. The IRS allows no carryback of losses to prior years, meaning you cannot recover taxes paid in previous years, only reduce future liability.

Final Thoughts

Capital gains tax strategy requires you to coordinate multiple moving parts: timing, asset selection, charitable giving, and generational planning. Waiting eleven months instead of nine months to sell an asset saves thousands in federal tax alone, while tax-loss harvesting systematically offsets gains throughout the year. Donating appreciated assets eliminates capital gains tax while generating charitable deductions, and holding assets until death provides your heirs with a stepped-up basis that wipes out accumulated gains.

Implementing these tactics requires you to understand your full financial picture, including your state of residence, current income level, investment timeline, and estate goals. A strategy that works brilliantly for one investor may create problems for another, which is why personalized analysis matters far more than applying generic approaches. Your specific circumstances determine which tactics deliver real savings and which ones create unnecessary complexity.

We at Bette Hochberger, CPA, CGMA help you map out your current gains, losses, and income, then evaluate which tactics apply to your situation. If you hold concentrated positions, substantial unrealized gains, or complex assets like real estate or business interests, contact us to discuss your capital gains tax strategy and identify the specific opportunities in your portfolio.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}