Venture capital tax planning isn’t an afterthought-it’s the foundation of profitable deals. The difference between a well-structured investment and a poorly planned one can cost you hundreds of thousands in unnecessary taxes.

At Bette Hochberger, CPA, CGMA, we’ve seen too many VC investors leave money on the table because they didn’t think about tax implications upfront. This guide walks you through the real strategies that matter.

How Exit Timing and Holding Periods Shape Your Tax Bill

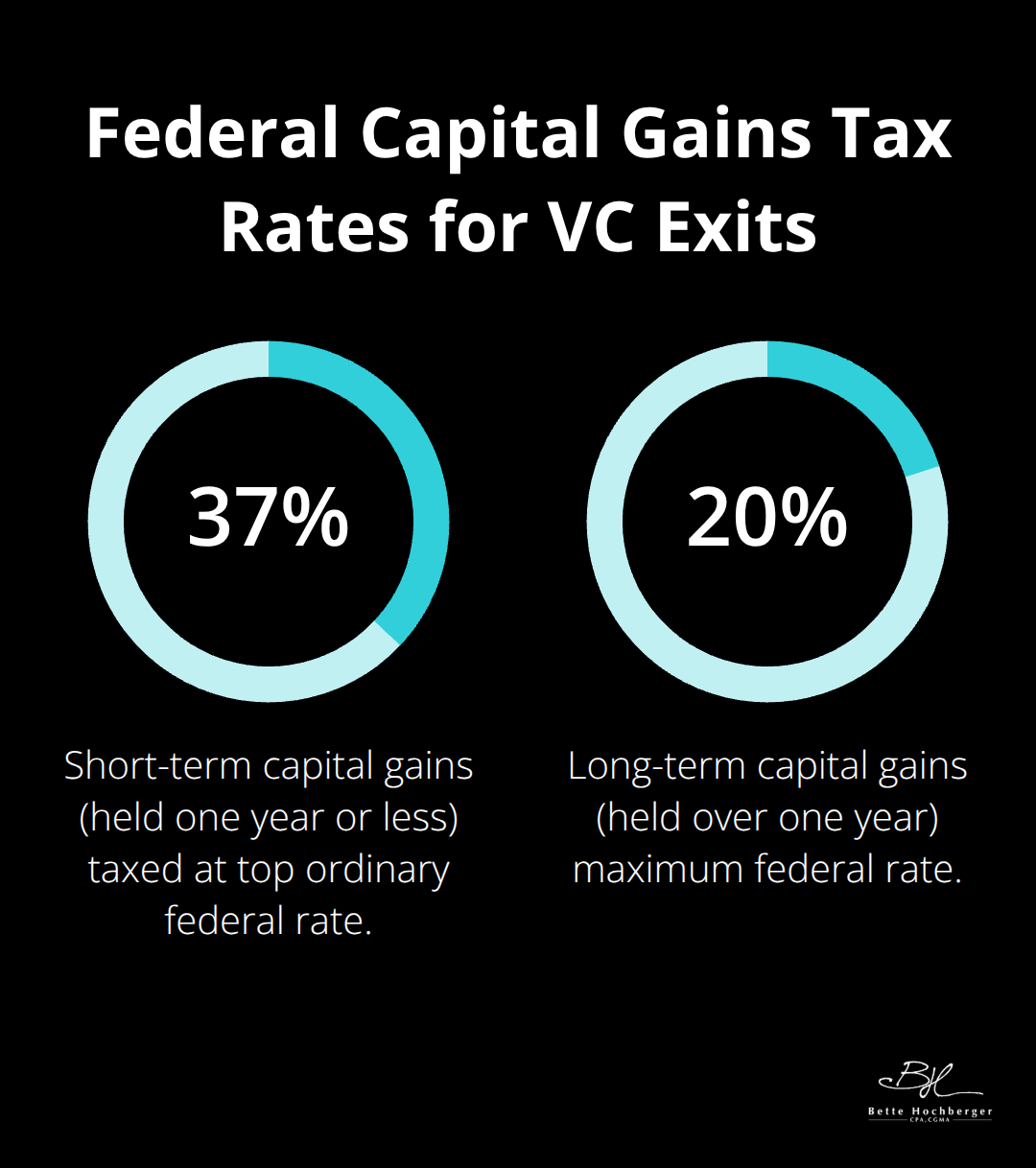

When you exit a venture investment, the tax bill depends almost entirely on how long you held the stake. Short-term capital gains, earned on investments held for one year or less, are taxed at ordinary income rates reaching 37% at the federal level. Long-term capital gains rates, held over one year, drop to a maximum federal rate of 20%-a difference that can easily save you six figures on a multimillion-dollar exit. A $10 million gain taxed at 37% costs $3.7 million, while the same gain at 20% costs $2 million. This isn’t theoretical; it’s the primary reason serious VC investors plan their exit timing around the one-year mark.

You should structure acquisition discussions and exit strategies with your tax advisor months in advance, not weeks. If you’re close to the one-year holding threshold when an acquisition offer arrives, delaying the close by a few weeks can shift your entire gain into long-term treatment. Many founders and investors miss this opportunity because they negotiate exit terms without consulting their tax team, then lock in short-term rates they could have avoided.

Carried Interest Requires Active Tax Planning

Carried interest, the profit share GPs take from fund exits, sits in a unique tax position. It qualifies for long-term capital gains rates if your fund meets specific conditions, including a three-year holding period on the underlying investment. However, this treatment remains actively debated in Congress, and the rules stay complex. If your fund structure doesn’t meet the requirements, the IRS taxes carried interest as ordinary income, eliminating the preferential rate entirely.

You need to verify with your fund’s legal and tax advisors whether your carried interest qualifies, and if not, whether restructuring the fund’s holding period or deal structure could unlock that benefit. The difference between ordinary and long-term rates on carried interest proves substantial-a $5 million carry taxed at ordinary rates (37%) versus long-term rates (20%) leaves you $850,000 lighter.

QSBS Exclusion Demands Early Tracking

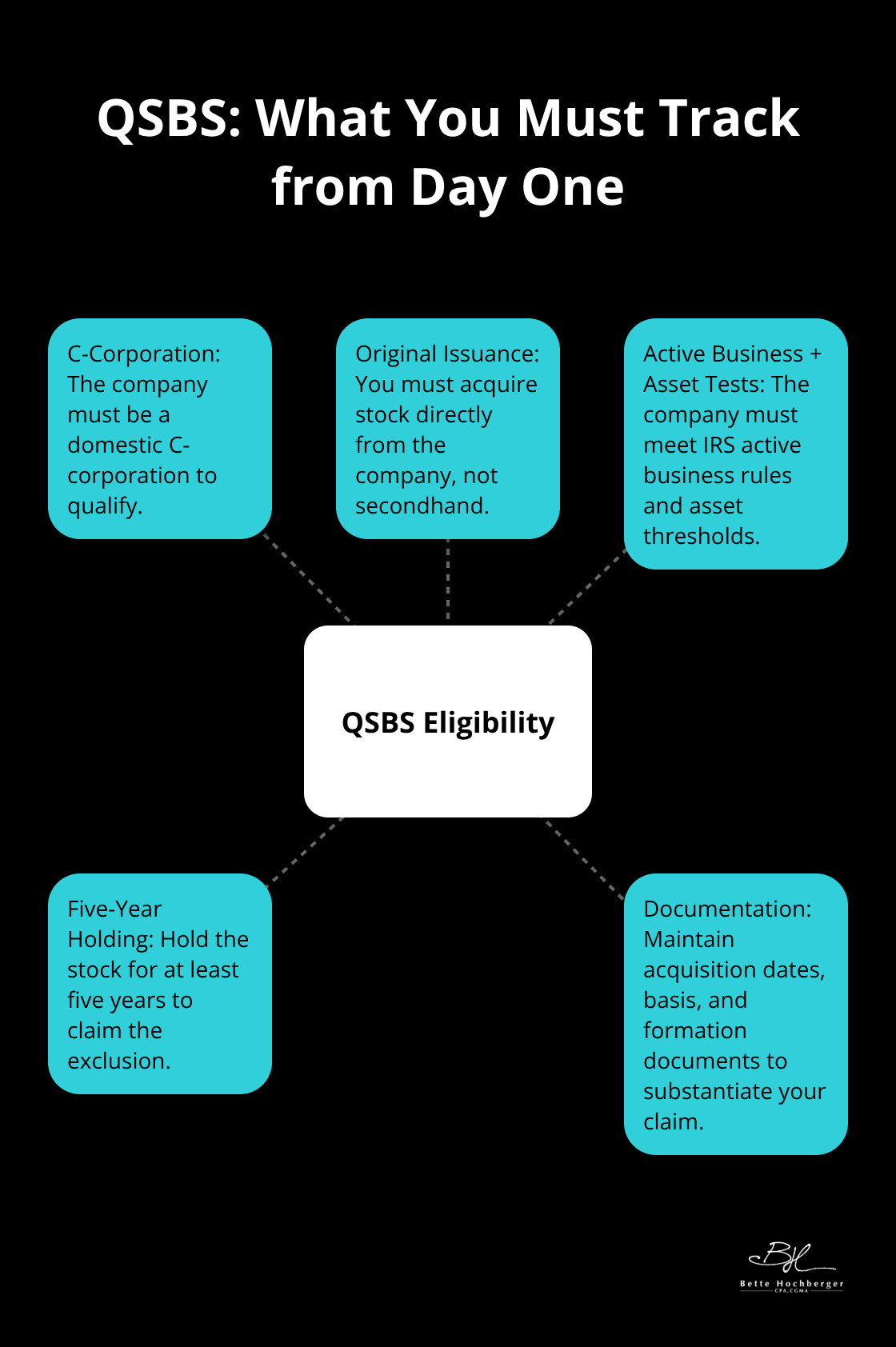

Qualified Small Business Stock exclusions allow you to exclude a portion of capital gains on qualifying investments, potentially excluding 100% of gains if you hold the stock for over five years. The qualification rules are strict: the company must be a domestic C-corporation, the stock must be issued directly by the company (not purchased secondhand), and the company must meet IRS asset tests and operate an active business. You must hold the stock for at least five years to claim the exclusion.

The problem we see constantly is that investors discover they own qualifying stock only after the fact, when they cannot go back and prove the acquisition date or verify the company structure. You need to track QSBS eligibility data for every portfolio company from day one-acquisition dates, cost basis, company formation documents, and annual asset tests. Without this documentation, the IRS will not accept your exclusion claim, regardless of whether you technically qualified.

An integrated fund administration platform flags eligible investments and tracks holding periods automatically, because manual spreadsheets inevitably miss data or lose documentation over five-year periods. This approach protects your ability to claim the exclusion when the exit arrives, transforming what could be a missed opportunity into real tax savings that compound across your portfolio.

How Entity Structure and Fund Timing Drive Tax Outcomes

Pass-Through Structures Shape Your Tax Liability

A venture capital fund structured as a limited partnership operates as a pass-through entity, which means the fund itself pays no taxes. Instead, all income flows directly to general partners and limited partners on their personal tax returns. This structure avoids double taxation and preserves the character of income-long-term capital gains remain long-term on each partner’s return. However, the three core taxable components flow through differently. Management fees become ordinary income to the GP’s management company and reduce taxable income passed to LPs, while realized gains and carried interest retain their character based on holding period. The concentration of value in exits amplifies this structure’s importance: the top 3.6% of exits in 2024 accounted for 78.9% of value, meaning a handful of deals drive your entire tax picture. One poorly timed or poorly structured exit can erase months of tax planning across your other investments.

Special Purpose Vehicles Offer Tactical Flexibility

Special Purpose Vehicles for individual deals or co-investment rounds provide tactical advantages that most VC investors overlook. An SPV holds one investment or a small cluster of related deals, which eliminates the complexity of tracking dozens of cap tables and K-1 allocations. When you structure a deal through an SPV, you control the timing of distributions and can coordinate when each investor realizes gains-something impossible in a commingled fund. If one portfolio company exits ahead of others, you can defer distributions from the SPV until other holdings mature, spreading realized gains across multiple tax years and potentially keeping yourself or your LPs in lower tax brackets. Additionally, an SPV’s simpler structure allows you to allocate carried interest with precision, ensuring that each GP receives only the carry they earned rather than averaging across all deals in a fund.

The Administrative Trade-Off

The downside of SPVs is administrative burden. You need precise cap table management for each SPV to allocate carried interest correctly and generate accurate K-1s by March 15. Manual tracking across multiple SPVs invites errors that trigger IRS penalties and delays LP filings. Many firms use integrated fund administration platforms to automate this work, since spreadsheets inevitably create gaps in documentation. The key decision point is straightforward: if you run a fund larger than $50 million with 20+ portfolio companies, the SPV approach becomes unwieldy. If you handle selective co-investments or smaller funds under $10 million, SPVs give you meaningful tax flexibility that a commingled structure cannot match. This flexibility extends to your next strategic consideration-timing distributions and managing when your LPs recognize income across multiple investment vehicles.

Where VC Investors Lose Six Figures Every Tax Season

Estimated tax payments Prevent Penalty Spirals

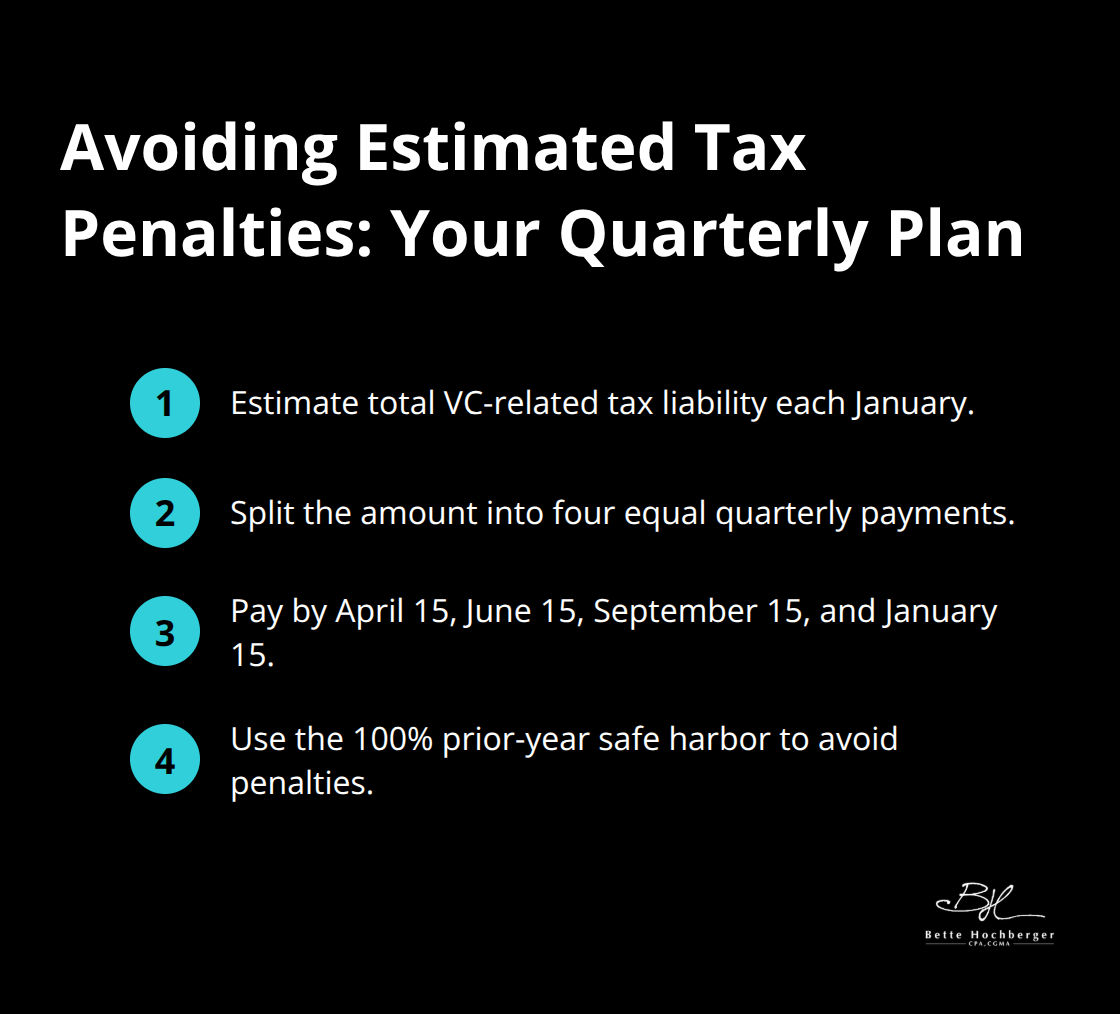

The IRS assesses penalties on unpaid estimated taxes if you fail to remit quarterly installments throughout the year. If you receive $2 million in carried interest from a fund exit in April but skip estimated payments, penalties can accumulate significantly on the unpaid amount. Over twelve months, that penalty alone could reach substantial figures-money that careful quarterly planning eliminates entirely. The solution requires calculating your expected tax liability from all VC sources each January, dividing it into four equal quarterly installments, and remitting those payments by the April 15, June 15, September 15, and January 15 deadlines.

Many investors treat estimated payments as an afterthought because VC income arrives unpredictably. The IRS penalizes you regardless of income volatility. Safe harbor rules protect you: if you pay 100 percent of your prior year’s tax liability spread across four quarters, you avoid penalties even if your actual tax turns out higher. This approach costs nothing upfront and protects you from six-figure penalty exposure on every exit.

Documentation of Investment Intent Determines Your Tax Classification

The IRS distinguishes between investment activities (taxed as capital gains) and dealer or trading activities (taxed as ordinary income at rates up to 37 percent). Inadequate records allow the IRS to reclassify your entire portfolio as dealer stock, converting long-term capital gains into ordinary income. The IRS examines frequency of sales, short holding periods, and active marketing or promotion to classify you as a dealer, but weak documentation makes their case straightforward.

You need written investment memos for every check you write, stating the investment thesis, expected holding period, and business rationale. These memos should live in a centralized data room alongside cap tables, acquisition agreements, and valuation analyses. Without this paper trail, an auditor questioning a $5 million gain has no written evidence that you intended a five-year hold rather than a quick flip. The burden shifts to you to prove your intent retroactively-a position that rarely succeeds.

Income Classification Errors Trigger Automated Audit Flags

Misclassifying partnership income versus corporate income on your personal return creates immediate audit exposure because K-1s from your venture funds report specific allocations that must match your filing. If you receive a K-1 showing $500,000 in long-term capital gains but report that amount as ordinary income on your 1040, the IRS catches the discrepancy through automated matching systems and initiates contact.

The fix is straightforward: reconcile every K-1 you receive against your tax return before filing, verify that income character matches exactly, and hold copies of K-1s and fund partnership agreements for seven years minimum. Many investors file returns without reviewing K-1s carefully, then scramble to amend when audits arrive. Proactive reconciliation takes two hours per fund annually and eliminates this exposure entirely.

Final Thoughts

Venture capital tax planning succeeds when you treat it as a core business function, not a compliance checkbox. The strategies outlined here-managing holding periods, tracking QSBS eligibility, structuring SPVs strategically, and documenting investment intent-compound across your portfolio to save hundreds of thousands in taxes. Start your tax planning before you sign the term sheet, not after.

Discuss holding period implications with your tax advisor when you evaluate an acquisition offer. Verify QSBS qualification requirements before you write the check, so you can track the necessary documentation from day one. Confirm that your fund’s carried interest structure qualifies for long-term capital gains treatment, and if not, explore whether restructuring makes sense.

We at Bette Hochberger, CPA, CGMA specialize in strategic tax planning for venture investors and fund managers. We help you structure deals for maximum tax efficiency, track complex portfolio data across multiple funds and SPVs, and coordinate timing strategies that keep you in lower tax brackets. Contact us to discuss how proactive planning transforms your after-tax returns.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}