Real estate investor taxes are costing you thousands in missed deductions every year. Most investors leave money on the table simply because they don’t know which expenses qualify or how to structure their portfolios for maximum tax efficiency.

At Bette Hochberger, CPA, CGMA, we’ve helped countless real estate investors reclaim deductions they didn’t know existed and implement strategies that dramatically improve their cash flow. This guide walks you through the deductions you’re missing, the planning strategies that work, and the tax-efficient moves that put more money back in your pocket.

Common Real Estate Tax Deductions You’re Missing

Mortgage Interest and Property Tax Deductions

Mortgage interest and property taxes form the foundation of real estate deductions, yet many investors claim them incorrectly or fail to separate them from personal use portions. Mortgage interest on rental debt remains fully deductible as a business expense, and the IRS treats rental property taxes through business deductions rather than the SALT cap that limits personal property taxes. The critical mistake occurs when investors own properties with mixed use-a rental unit plus a personal residence on the same lot. You must allocate expenses based on actual rental versus personal use, typically using square footage or room count. If your property generates 70% rental income, you deduct 70% of the mortgage interest and property taxes as business expenses. This separation is where substantial money gets left behind.

Accelerating Deductions Through Depreciation

Depreciation offers even greater opportunities, especially through cost segregation strategies that most investors ignore entirely. Standard residential rental property depreciates over 27.5 years using straight-line depreciation, but cost segregation breaks a property into components with shorter recovery periods-5-year, 7-year, and 15-year property-potentially accelerating deductions in the first year. Bonus depreciation, restored for qualified property placed in service after January 19, 2025, allows you to immediately expense certain assets rather than spreading deductions across years. The 2025 Section 179 deduction limit reaches $2,500,000, with the deduction reduced only when property placed in service exceeds $4,000,000.

Operating Expenses That Count

Operating expenses extend far beyond what investors typically claim. Maintenance costs qualify under a specific framework: the De Minimis Safe Harbor covers invoices up to $2,500 per item, and the Routine Maintenance Safe Harbor protects regular upkeep as current deductions rather than capitalizable improvements. Repairs that restore property to working condition are immediately deductible, while improvements that extend useful life or adapt property to new uses must be depreciated. Travel costs to collect rent, manage property, or attend to tenant issues are deductible with proper records, though commuting between your home and a rental property generally remains non-deductible. Professional services-accounting, bookkeeping, legal advice tied directly to rental operations-reduce your taxable income dollar-for-dollar. Insurance premiums for liability, errors and omissions, and general coverage all count. Staging costs, cleaning, and minor improvements before listing a property for sale or lease are deductible.

Tracking Mileage and Utility Costs

The IRS standard mileage rate for business driving related to rental activity is 70 cents per mile in 2025, making detailed mileage logs essential. If you drive 12,000 business miles annually, that generates an $8,400 deduction before parking and tolls. Few investors track this consistently, yet it accumulates quickly across property visits, contractor meetings, and tenant interactions. Utilities, property management fees, and even a portion of your internet bill-allocated to your business use percentage-belong on your tax return. These smaller deductions compound throughout the year and significantly reduce your overall tax burden when you claim them systematically.

The deductions you claim today directly affect the cash flow you retain tomorrow. Strategic planning around these expenses requires more than just knowing what qualifies; it demands understanding how to structure your portfolio and time your deductions for maximum impact.

Strategic Tax Planning for Real Estate Portfolios

Entity Structure Selection and Tax Implications

Your choice of entity structure determines whether you pay taxes on rental income once or twice, whether losses offset your other income, and ultimately how much cash stays in your pocket. Most real estate investors default to a sole proprietorship or basic LLC without considering the tax implications, costing themselves tens of thousands annually. An LLC provides liability protection but does not automatically optimize your tax position. If your net rental income exceeds $75,000, electing S-Corporation taxation can reduce self-employment taxes significantly. An S-Corp allows you to take a reasonable salary and distribute the remainder as dividends, which bypass the 15.3% self-employment tax. A real estate investor earning $100,000 in net income might save $6,000 to $9,000 annually through an S-Corp election, though you must weigh this against additional accounting and payroll costs of roughly $1,500 to $3,000 per year. C-Corporations rarely make sense for rental real estate due to double taxation, but partnerships and LLCs taxed as S-Corps create flexibility for multi-property portfolios. When you own properties jointly with a spouse, a Qualified Joint Venture election allows you to file two separate Schedule Es while maintaining the liability protection of an LLC, potentially simplifying future property transfers and estate planning.

1031 Exchanges and Deferral Strategies

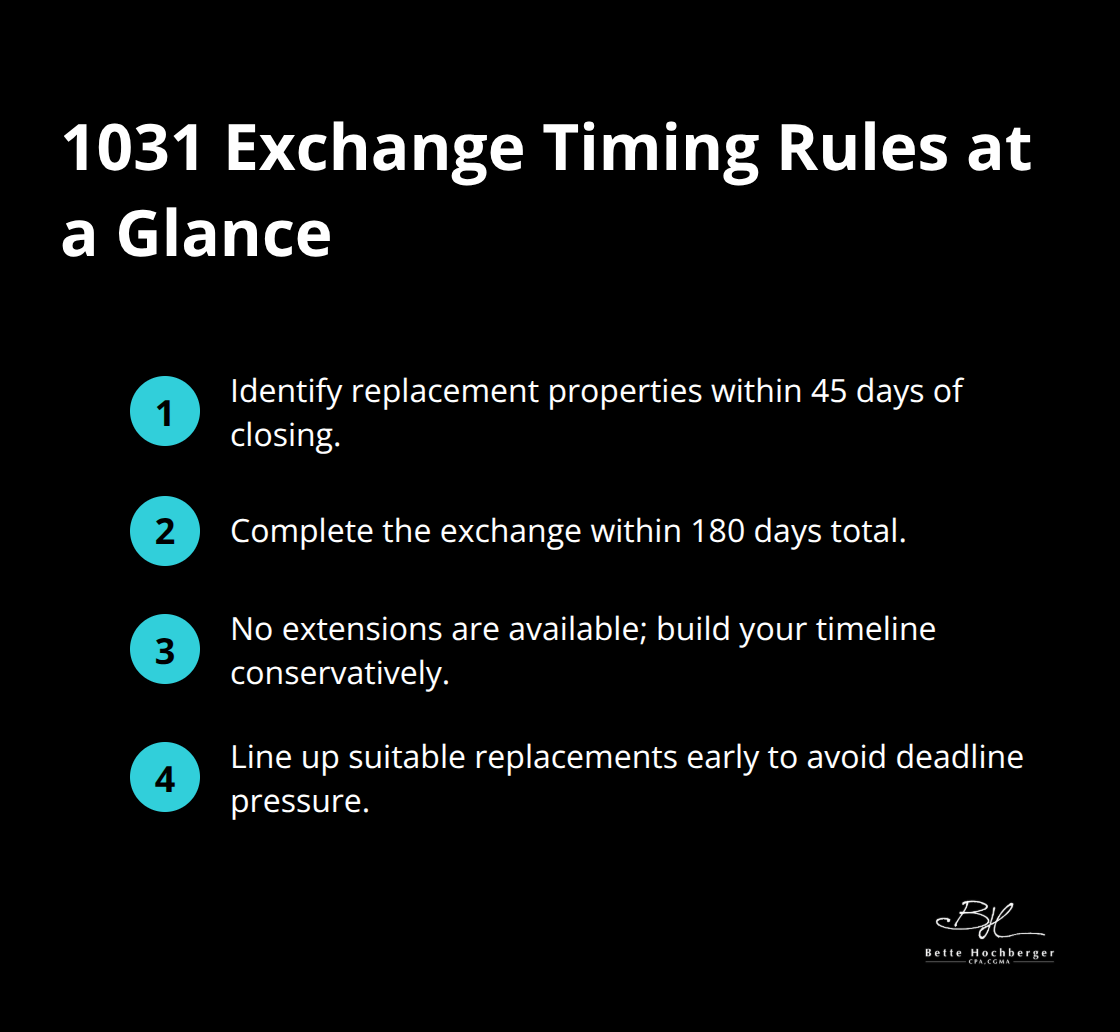

A 1031 exchange lets you defer capital gains indefinitely by reinvesting sale proceeds into like-kind real property, but timing and identification rules are unforgiving. You have 45 days from closing to identify replacement properties and 180 days total to complete the exchange, with no extensions available. Many investors miss these deadlines because they underestimate the complexity of finding suitable replacement properties in a compressed timeframe.

Cost segregation complicates 1031 exchanges because personal property components may not qualify as like-kind real property, potentially disqualifying portions of your exchange and triggering unexpected taxes. The structure you choose today affects your ability to offset losses against other income, claim Real Estate Professional status, and execute 1031 exchanges without triggering unexpected tax consequences.

Passive Activity Loss Rules and Real Estate Professional Status

Passive activity loss rules restrict your ability to deduct rental losses against W-2 income unless you meet specific thresholds. If your Modified Adjusted Gross Income falls between $100,000 and $150,000, the $25,000 passive loss allowance phases out entirely, eliminating deductions you could claim at lower income levels. Real Estate Professional status, achieved by performing more than 750 hours of services during the tax year in real property trades or businesses in which you materially participate, converts passive rental losses into active business losses that offset ordinary income without limitation. Contemporaneous time logs documenting date, hours, tasks, and specific properties provide the documentation the IRS demands to substantiate REP status. Courts consistently reject inflated or post-hoc hour claims, making consistent record-keeping the difference between a successful REP position and an audit that disallows your deductions. Grouping elections under Treasury Regulation 1.469-9(g) allow you to treat all rental real estate activities as a single activity, making the 750-hour threshold and material participation tests substantially easier to satisfy across a multi-property portfolio. These strategic moves transform how your portfolio operates from a tax perspective and directly influence the cash flow strategies you can implement moving forward.

How to Accelerate Deductions and Control Your Tax Timeline

Bonus Depreciation and Section 179 Expensing

The timing of when you claim deductions separates investors who pay thousands in unnecessary taxes from those who retain that money in their business. Most real estate investors treat tax deductions as a reactive exercise, claiming whatever expenses they tracked at year-end. This approach leaves substantial tax savings unclaimed and forces you to pay taxes on income you could have offset with strategic planning conducted months earlier. The IRS provides powerful tools to control your tax timeline, but using them effectively requires decisions made well before December 31st.

Bonus depreciation, restored for qualified property placed in service after January 19, 2025, allows you to immediately expense personal property components rather than spreading deductions across years. The 2025 Section 179 deduction limit of $2,500,000 means you can expense equipment, furniture, and technology in the year of purchase if you plan acquisitions strategically. An investor who purchases a $40,000 HVAC system in December captures the full deduction immediately instead of depreciating it over years. The same applies to appliances, flooring, and building systems that cost segregation studies classify as personal property rather than structural components. This acceleration generates front-loaded deductions that reduce your current-year tax liability and free cash flow precisely when you need it most.

Qualified Business Income Deductions for Real Estate

Qualified Business Income deductions under Section 199A provide an additional 20% deduction on pass-through business income, but real estate investors must qualify their activities as genuine trades or businesses rather than passive investment activities. The IRS safe harbor in Revenue Procedure 2019-7 establishes that rental real estate qualifies for the QBI deduction if you maintain contemporaneous records, perform substantial services, and actively participate in management decisions.

An investor who manages multiple properties personally, handles tenant relations, and approves capital expenditures meets these criteria far more easily than a passive investor who simply collects rent checks.

If your rental business generates $150,000 in net income and qualifies for the full QBI deduction, you reduce your taxable income by $30,000 at no additional cost. This deduction compounds when combined with other tax strategies, creating substantial savings that most investors never claim.

Real Estate Professional Status and Loss Offsets

Real Estate Professional status amplifies your deduction strategy because it converts passive rental losses into active business losses that offset W-2 income without passive activity loss limitations. The 750-hour threshold requires consistent documentation, but investors who maintain detailed time logs treating real estate as their primary business can deduct losses that would otherwise remain suspended indefinitely. Courts consistently reject inflated or post-hoc hour claims, making consistent record-keeping the difference between a successful REP position and an audit that disallows your deductions.

An investor with $100,000 in rental losses who qualifies for REP status offsets that amount against other income immediately rather than carrying losses forward for years. Contemporaneous time logs documenting date, hours, tasks, and specific properties provide the documentation the IRS demands to substantiate REP status. Grouping elections under Treasury Regulation 1.469-9(g) allow you to treat all rental real estate activities as a single activity, making the 750-hour threshold and material participation tests substantially easier to satisfy across a multi-property portfolio.

Strategic Timing for Maximum Tax Efficiency

These strategic moves require planning in advance, not scrambling in March when your accountant requests information about your deductions. Property acquisitions, equipment purchases, and timing of income recognition all influence your final tax position. An investor who coordinates the purchase of depreciable assets with the timing of rental income recognition can substantially reduce tax liability compared to an investor who makes these decisions reactively. The structure you choose today affects your ability to offset losses against other income, claim Real Estate Professional status, and execute strategic tax moves without triggering unexpected tax consequences.

Final Thoughts

Real estate investor taxes don’t have to drain your cash flow. The deductions you’ve learned about in this guide-mortgage interest, depreciation, cost segregation, operating expenses, and strategic timing-represent thousands of dollars sitting unclaimed on your tax return right now. Most investors leave this money behind because they treat tax planning as an afterthought rather than a core business strategy, and an S-Corp election can save you $6,000 to $9,000 annually once your net income exceeds $75,000.

Real Estate Professional status converts passive losses into active deductions that offset your other income without limitation, while bonus depreciation and Section 179 expensing accelerate deductions into the current year instead of spreading them across decades. These moves compound when executed together, transforming your tax position from reactive to strategic, and the difference between competent tax preparation and strategic tax planning often exceeds $10,000 annually. We at Bette Hochberger, CPA, CGMA work with real estate investors to identify these opportunities before they’re lost to the calendar year, helping you structure your portfolio correctly and time your deductions strategically.

Schedule a consultation with Bette Hochberger, CPA, CGMA to identify which deductions you’re missing and which strategies apply to your situation. The cost of that conversation is minimal compared to the deductions you’ll reclaim and the cash flow you’ll retain.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}