Cryptocurrency losses might feel like a setback, but they’re actually a powerful tax tool. The IRS allows you to deduct capital losses from digital assets, which can significantly reduce what you owe in taxes.

At Bette Hochberger, CPA, CGMA, we help clients turn crypto losses into real tax savings. This guide shows you exactly how to claim these deductions and avoid costly mistakes.

What Qualifies as a Deductible Crypto Loss

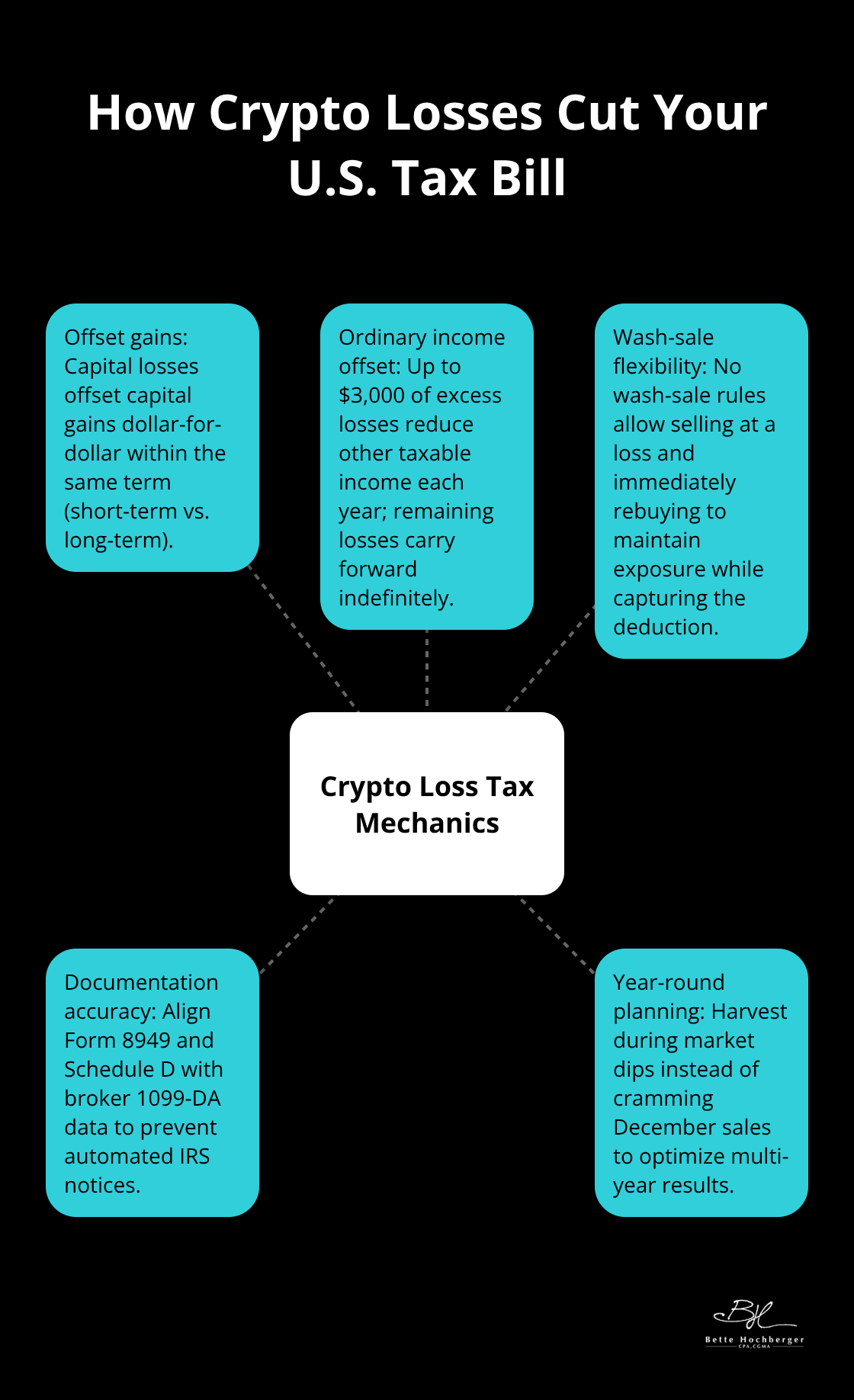

The IRS treats cryptocurrency as property, not as a security, which means every sale or trade triggers a capital gain or loss calculation. A deductible crypto loss occurs when you sell digital assets for less than your cost basis-your purchase price plus any acquisition fees. If you bought Bitcoin at $45,000 and sold it at $38,000, you have a $7,000 capital loss. This loss only becomes real and claimable when you actually execute the sale or trade. Simply watching your portfolio decline in value generates no tax deduction until you take action. Many crypto holders miss opportunities because they assume losses are automatic tax benefits when they’re actually only deductible once a taxable event occurs. The IRS estimates that roughly 75% of crypto holders have not been fully compliant with reporting requirements, and failing to document losses properly is a major reason why.

Timing Matters More Than You Think

Short-term losses (assets held one year or less) offset short-term gains dollar-for-dollar and are taxed as ordinary income, potentially costing you up to 37% in federal taxes for 2025. Long-term losses (assets held more than one year) offset long-term gains, which are taxed at preferential rates of 0%, 15%, or 20% depending on your income level. This distinction makes timing critical.

The number 0% seems to be not appropriate for this chart. Please use a different chart type. If you have substantial short-term gains from trading, realizing short-term losses later in the year can directly reduce your ordinary income tax bill. Conversely, if your gains are long-term, you might prioritize long-term losses to offset them at lower rates. The lack of wash-sale rules in crypto-unlike stocks-means you can sell at a loss and immediately repurchase the same asset, giving you flexibility traditional investors don’t have. However, the IRS scrutinizes transactions that lack economic substance, so avoid patterns that appear designed purely to manufacture losses without genuine investment intent.

How Losses Carry Forward and Reduce Future Tax Bills

Capital losses that exceed your capital gains can offset up to $3,000 of other taxable income per year, with any remaining losses carrying forward indefinitely to future tax years. If you realized $15,000 in losses but only $8,000 in gains, you deduct $3,000 against ordinary income this year and carry forward the remaining $4,000 to next year. This carryforward mechanism is powerful for volatile crypto portfolios: a major market downturn can generate losses that shield you from taxes for years to come. Maintain detailed records of every transaction, including the date acquired, date sold, cost basis, and sale proceeds across all exchanges and wallets. Consolidating this data is essential because most exchanges don’t maintain cost basis for you-you must track it yourself. When the IRS introduced Form 1099-DA for digital asset reporting, mismatches between what you report and what the IRS receives on that form trigger automated notices. Using crypto tax software that ingests 1099-DA data and reconciles it against your actual transactions helps you flag discrepancies before you file.

Documentation Gaps That Trigger IRS Scrutiny

Frequent transfers between self-custody wallets and exchanges often lead to missing or incomplete cost-basis data, complicating your reporting and increasing audit risk. The decentralized nature of crypto makes consistent cost-basis reporting across platforms challenging, which is why you need solid data practices from the start. Consolidate cost-basis information from every platform you use and take ownership of your crypto data rather than relying on exchanges to maintain it for you. When you file Form 8949 and Schedule D, the IRS cross-references your reported proceeds against 1099-DA forms they receive from brokers. A mismatch between your return and the IRS’s records can trigger notices, so robust software that ingests and reconciles 1099-DA data becomes your first line of defense. Even if enforcement is limited now, the IRS intends to process new digital asset reporting forms, and data can be reviewed years later.

How to Sell Crypto Losses Without Triggering IRS Penalties

Plan Loss Sales Throughout the Year, Not Just in December

The calendar approaching year-end is when most crypto holders finally confront their losses, but selling in December scrambles your tax strategy and leaves no room for course correction. Smart crypto investors plan loss realization throughout the year, particularly when markets dip and losses accumulate naturally. If Bitcoin drops 20% in March and you hold a position underwater, that’s the moment to evaluate whether selling locks in a genuine loss that offsets your gains from other trades or income.

The math is straightforward: if you realized $12,000 in capital gains from selling Ethereum at a profit and hold $8,000 in losses across three altcoins, selling those losers immediately reduces your taxable gain to $4,000 and shields you from tax on that $8,000 difference. The federal tax savings alone could reach $3,000 or more depending on your tax bracket.

Leverage Crypto’s Unique Advantage: No Wash-Sale Rules

What makes crypto different from stocks is the absence of wash-sale rules, which means you can sell Bitcoin at a $5,000 loss on Monday and repurchase the identical amount on Tuesday without IRS penalties. This flexibility is genuinely unique to crypto and should inform your strategy: if you believe a position will recover, harvest the loss and rebuy immediately to maintain your exposure while securing the deduction.

However, the IRS watches for patterns that lack economic substance, so avoid selling and repurchasing the same asset repeatedly within days or weeks purely to manufacture losses without genuine investment conviction. The transaction must reflect a real investment decision, not a tax-driven scheme.

Record Every Detail of Your Loss Sales

When you execute a loss sale, record the exact date, time, asset name, quantity sold, cost basis per unit, total purchase price (including fees), sale price per unit, total proceeds minus fees, and the resulting loss amount. Most exchanges provide transaction history, but transfers between your exchange account and self-custody wallet can disappear from records, creating gaps that invite scrutiny.

Use crypto tax software like CoinTracker or Koinly that automatically ingests transactions from multiple exchanges and wallets, calculates cost basis using your chosen method (FIFO, LIFO, HIFO, or specific identification), and flags mismatches before you file. The IRS introduced Form 1099-DA for digital asset reporting starting in 2024, and when your broker reports proceeds to the IRS, those numbers must match what you report on Form 8949 and Schedule D.

Match Your Reported Losses to IRS Records

A $2,000 discrepancy between your reported loss and the IRS’s records triggers an automated notice, and explaining the difference months later costs far more in time and stress than preventing it upfront. Specific identification is your best friend here: when you sell a position at a loss, explicitly identify which units you’re selling so you can match them to your purchase records with precision.

If you can’t identify specific units, the IRS defaults to FIFO, which may not optimize your tax outcome and removes your control over the calculation. Maintain a master spreadsheet that consolidates every transaction across all platforms, updated monthly, so you never face December chaos trying to reconstruct six months of trading activity from fragmented exchange records.

Consolidate Your Data Before Filing

Frequent transfers between self-custody wallets and exchanges often lead to missing or incomplete cost-basis data, complicating your reporting and increasing audit risk. The decentralized nature of crypto makes consistent cost-basis reporting across platforms challenging, which is why you need solid data practices from the start.

Consolidate cost-basis information from every platform you use and take ownership of your crypto data rather than relying on exchanges to maintain it for you. When you file Form 8949 and Schedule D, the IRS cross-references your reported proceeds against 1099-DA forms they receive from brokers. A mismatch between your return and the IRS’s records can trigger notices, so robust software that ingests and reconciles 1099-DA data becomes your first line of defense. Even if enforcement is limited now, the IRS intends to process new digital asset reporting forms, and data can be reviewed years later. With your loss documentation locked down and your records aligned with IRS reporting, you’re ready to explore how to offset those losses against your capital gains and structure a multi-year tax strategy.

How Crypto Losses Actually Reduce Your Tax Bill

Real Losses Create Real Tax Savings

A trader holding Ethereum purchased at $2,800 per coin watched the price drop to $1,200 in late 2022. Instead of waiting for recovery, they sold 10 coins for a $16,000 loss and immediately repurchased at $1,250 when they believed the bottom was near. That $16,000 loss offset $16,000 in short-term gains from other crypto trades executed earlier that year, reducing their ordinary income tax from roughly $5,920 (at the 37% federal rate) to zero on that portion of gains. Without the loss realization, they would have owed thousands in federal tax alone on profits they felt were offset by their larger portfolio decline.

This scenario plays out repeatedly in crypto portfolios because volatile assets create genuine loss opportunities that traditional stock investors cannot exploit as freely due to wash-sale restrictions. The IRS estimates 75% of crypto holders fail to report losses correctly, which means most people leave thousands in tax deductions on the table. A $50,000 loss harvested strategically can reduce your federal tax bill by $18,500 if you’re in the top bracket, or $15,000 if you’re in the 30% bracket.

Multi-Year Loss Strategies Compound Your Advantage

The real power emerges when you structure losses across multiple years. A crypto investor who realized $45,000 in capital losses during the 2023 market decline used $8,000 to offset gains that year (reducing taxable income by $3,000 after the annual $3,000 ordinary income limitation), then carried forward $37,000 to subsequent years. Over the next three years, as markets recovered and they executed profitable trades generating $28,000 in gains, the carryforward losses eliminated all tax on those gains. They paid zero capital gains tax on $28,000 of profit because prior-year losses did the heavy lifting.

Meanwhile, a peer who held the same underwater positions without selling paid full capital gains tax on their profitable trades when markets rebounded, costing them thousands in unnecessary tax. The difference between strategic loss recognition and passive portfolio management is substantial and compounds over time.

Documentation and Timing Drive Results

The mechanics require precision: maintain a detailed ledger tracking cost basis separately from exchange price movements, use crypto tax software like CoinTracker to flag discrepancies before filing, and plan loss sales throughout the year rather than cramming them into December. When you file Form 8949 and Schedule D, the IRS cross-references your reported loss amounts against 1099-DA forms from brokers, so accuracy in documentation prevents automated notices.

Execute loss sales when markets dip significantly and positions trade substantially below cost basis, treating each sale as a genuine investment decision rather than a tax-manufacturing event. Under current federal law, cryptocurrency is not subject to wash-sale rules, which gives you the flexibility to harvest losses and maintain exposure simultaneously, but only if your records are airtight and your transaction patterns reflect authentic investment intent rather than artificial timing designed purely for deductions.

Final Thoughts

Cryptocurrency losses function as direct tax deductions that reduce what you owe to the IRS. You sell underwater positions, document the transactions with precision, and offset those losses against your capital gains. When losses exceed gains, you deduct up to $3,000 against ordinary income and carry the remainder forward indefinitely. A $50,000 loss harvested strategically can save you $15,000 to $18,500 in federal taxes depending on your bracket, and the absence of wash-sale rules in crypto gives you flexibility that stock investors lack.

The real advantage emerges when you structure cryptocurrency losses across multiple years. A trader who realized $45,000 in losses during a market downturn used them to offset gains over three subsequent years, paying zero capital gains tax on $28,000 of profit. Without strategic loss recognition, they would have owed thousands in unnecessary tax, and most crypto holders miss these opportunities because they fail to document losses properly or wait until December to act.

Professional tax planning matters for digital assets because the IRS cross-references your reported losses against Form 1099-DA data from brokers, and mismatches trigger automated notices. We at Bette Hochberger, CPA, CGMA help clients structure cryptocurrency losses strategically, maintain compliant documentation, and execute multi-year tax plans that compound savings over time. Contact us to consolidate your transaction records, plan loss sales throughout the year, and align your loss strategy with your overall financial goals.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}