Facing an IRS audit or dispute can feel overwhelming, but you don’t have to navigate it alone. At Bette Hochberger, CPA, CGMA, we’ve helped countless clients understand their rights and build effective defense strategies.

This IRS representation guidance walks you through the steps to protect your interests and work confidently with a professional representative.

Your Right to Professional Representation

The Foundation of Your Defense

The IRS recognizes your fundamental right to have a qualified representative handle your tax matters, whether you face an audit, a collection action, or a penalty dispute. Under the Taxpayer Bill of Rights, you cannot be forced to communicate directly with the IRS if you have authorized someone to act on your behalf. This protection matters because the IRS conducted over 500,000 audits in 2024 alone, resulting in nearly $30 billion in additional tax assessments. A professional representative acts as your intermediary, communicates with the IRS, attends interviews, requests document extensions, and negotiates settlements on your behalf.

Who Can Represent You Before the IRS

The IRS accepts representation from attorneys, CPAs, enrolled agents, enrolled actuaries, and enrolled retirement plan agents. Each brings different strengths to your defense. Tax attorneys offer attorney-client privilege for confidential strategy discussions, CPAs provide deep accounting expertise and tax knowledge, and enrolled agents specialize in individual and small business tax matters.

You authorize representation through Form 2848, which establishes a Power of Attorney with the IRS and gets recorded in their Centralized Authorization File. Without this form, the IRS won’t recognize your representative’s authority, so you must submit it immediately when you hire someone.

When Professional Representation Becomes Essential

Audit exposure remains under 1 percent for most individual returns, but rises substantially for high earners, businesses, and complex filings. The IRS uses a Discriminant Inventory Function score to flag returns with unusual deductions relative to income, and information mismatches between your reported figures and W-2s, 1099s, or K-1s trigger correspondence audits. If you understated gross income by more than 25 percent, the IRS can audit back up to six years instead of the standard three.

You need professional representation when you face an office or field audit rather than a simple correspondence audit, when multiple years are under examination, or when the IRS pursues collection actions like wage garnishment or bank levies. These situations demand expertise that protects your interests and reduces your exposure.

Affordable Options When Resources Are Limited

If you cannot afford representation, Low Income Taxpayer Clinics offer free or low-cost assistance for audits, appeals, and collection disputes. These independent clinics serve those below income thresholds and provide multilingual support. You can locate one by calling 800-829-3676 or visiting the Low Income Taxpayer Clinics page. With representation in place, you shift from reactive defense to strategic positioning-and that positioning determines how you address the specific issues the IRS raises.

How to Prepare Your Documentation and Defense

Gather Every Document That Supports Your Position

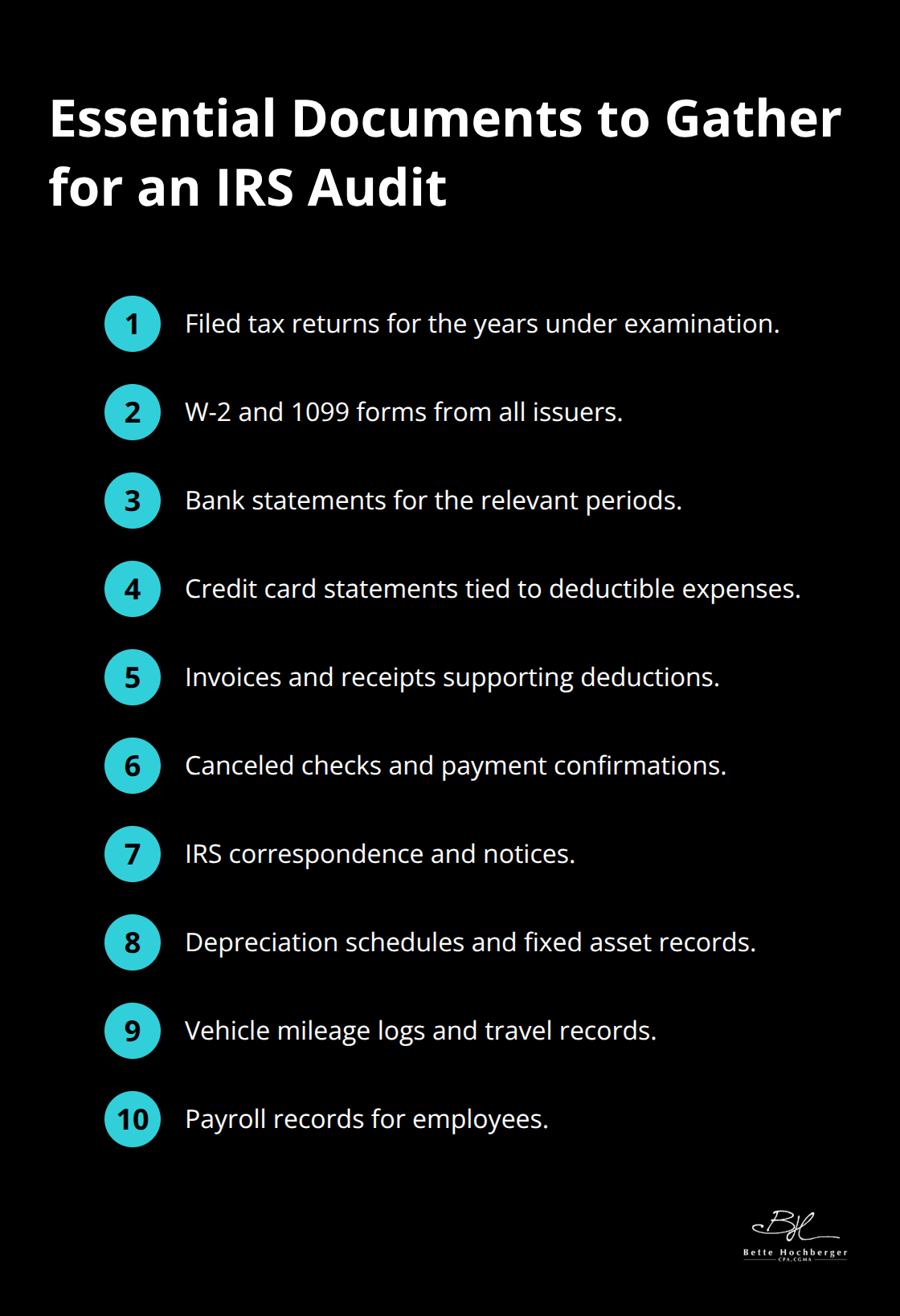

Documentation is your defense. The IRS operates on paper trails, receipts, ledgers, and contemporaneous records-not memory or good intentions. Before your representative meets with the IRS, you must gather every document related to the years under examination.

This includes tax returns, W-2s, 1099s, bank statements, credit card statements, invoices, receipts, canceled checks, and any correspondence with the IRS. If the audit involves business deductions, pull depreciation schedules, vehicle logs, meal and entertainment records, and employee payroll documentation.

The IRS scrutinizes deductions that appear inflated relative to your income, and weak documentation transforms a defensible position into a losing one. Most audits focus on the last two tax years, but if the IRS suspects you understated income by more than 25 percent, they can reach back six years. That means you may need records spanning far longer than you initially thought. Organize these documents chronologically and by category-do not hand your representative a shoebox of receipts and expect them to build a strategy. Your representative needs to see exactly what you have before they walk into an IRS office.

Identify the Specific Issues Under Examination

Once you organize documentation, your representative identifies the specific issues the IRS is examining. Audits rarely challenge everything on your return; the IRS typically targets particular line items or deduction categories. Information matching between what you reported and what third parties reported to the IRS often reveals the real problem. If your 1099 income does not match what you claimed on your return, that represents a clear discrepancy that needs explaining. If you claimed business expenses that seem disproportionate to your reported income, the IRS will ask for substantiation.

Your representative then develops a response strategy that either justifies those deductions with solid documentation or identifies which items are indefensible and should be conceded early. Conceding weak positions early actually strengthens your negotiating power on the items you can defend. The IRS categorizes audit outcomes into three categories: No Change, Agreed, and Disagreed. Working toward an Agreed outcome on most issues while preserving appeal rights on disputed items requires strategy built on what the documentation actually shows, not what you wish it showed.

Prepare Written Explanations and Close Documentation Gaps

Your representative coordinates with you to fill documentation gaps, obtain missing records from third parties if necessary, and prepare written explanations for complex deductions or transactions. These explanations must address the IRS’s specific concerns and reference the supporting documents you’ve organized. A well-prepared written response demonstrates that you took the audit seriously and that your position rests on fact, not assumption. This preparation phase determines whether the IRS views you as a credible taxpayer or as someone trying to hide something.

With documentation organized and explanations prepared, your representative moves into active negotiation with the IRS. The strength of your defense depends entirely on what you present during this phase.

What the IRS Actually Targets in Audits

Information Matching Reveals Your Real Exposure

The IRS does not randomly audit returns. They use data analytics and information matching to identify specific discrepancies, and your defense strategy must address exactly what triggered the examination. The IRS uses information matching to verify self-reported income and tax on returns filed by taxpayers, comparing what you claimed against what employers, financial institutions, and clients reported to the IRS on W-2s, 1099s, and K-1s. If you reported $80,000 in self-employment income but a client sent the IRS a 1099 showing $120,000 in payments, that gap becomes your audit. Your representative must obtain copies of every third-party information return filed about you and compare it line-by-line to what you reported. Discrepancies here are not matters of interpretation; they are factual errors that require either amended returns, reasonable explanations backed by documentation, or concession.

Deduction Scrutiny and the DIF Score

The IRS’s Discriminant Inventory Function score flags returns where deductions appear inflated relative to reported income, meaning a Schedule C business showing $50,000 in revenue but $45,000 in expenses will draw scrutiny. Many taxpayers lose audits because they argue about deductions when the real problem is unreported income the IRS discovered through information matching. Your representative must separate weak positions from strong ones and concede items that lack solid documentation. This strategic approach actually strengthens your negotiating power on the items you can defend with evidence.

Collection Actions and Immediate Response Requirements

Wage garnishments and bank levies occur when you owe back taxes and fail to respond to collection notices. Your representative must act immediately upon receiving an audit notice to prevent the IRS from escalating to enforcement actions. The statute of limitations for IRS assessment is three years from the later of your return due date or filing date, but if you understated gross income by more than 25 percent, the IRS can assess back six years. This extended timeline means the IRS can examine multiple years simultaneously, multiplying your exposure and complexity.

Penalties and Abatement Opportunities

Penalties compound the damage in audits because the IRS assesses accuracy-related penalties for substantial understatement of income, negligence penalties for inadequate record-keeping, and fraud penalties if they suspect intentional evasion. Most penalties are abatable if your representative can demonstrate reasonable cause and that you exercised ordinary business care. This requires contemporaneous documentation showing you maintained records, relied on a qualified tax professional, or faced circumstances beyond your control that prevented accurate reporting. The IRS abates penalties frequently when taxpayers have clean compliance histories and can show the error was isolated, not a pattern. Your representative negotiates penalty abatement separately from the underlying tax assessment, and securing abatement can reduce your total exposure by 20 to 40 percent depending on which penalties applied.

Audit Outcomes and Multi-Year Strategy

The three audit outcomes-No Change, Agreed, and Disagreed-determine your next steps and your rights to appeal. An Agreed outcome means you accept the IRS’s proposed adjustments and pay the additional tax, interest, and any applicable penalties. A Disagreed outcome preserves your right to request a manager conference, file an appeal with the IRS Office of Appeals, or pursue judicial review in Tax Court or Federal Court.

Your representative must evaluate whether disputing an item makes financial sense given the strength of your documentation and the cost of continued representation through appeals. When multiple years are involved, your representative must immediately calculate the cumulative impact across all years under examination because fighting one year while conceding another may not be the optimal strategy. Penalty abatement becomes even more valuable when multiple years are involved because penalties compound across years. If the IRS proposed penalties on three consecutive years of undisclosed income, abating penalties on even one year saves substantial money. The defense strategy shifts from defending individual line items to managing total exposure across all years, all penalties, and all interest calculations.

Final Thoughts

IRS representation guidance succeeds when you act before problems escalate. The foundation of your defense rests on three elements: understanding your right to professional representation, organizing documentation that supports your position, and addressing the specific issues the IRS targets. Most taxpayers lose audits not because their positions lack merit, but because they fail to document their deductions or they wait too long to hire representation.

Your representative transforms a reactive scramble into a strategic response. They identify which items you can defend with evidence and which items require concession, they negotiate penalty abatement that reduces your total exposure, and they manage multi-year audits by calculating cumulative impact rather than fighting each year in isolation. The cost of professional representation pays for itself through penalty abatement alone-when the IRS proposes accuracy-related penalties, negligence penalties, or fraud penalties, your representative demonstrates reasonable cause and ordinary business care to secure abatement.

We at Bette Hochberger, CPA, CGMA specialize in personalized financial services including strategic tax planning and tax preparation designed to minimize tax liabilities. We help clients navigate IRS disputes and build defense strategies that protect their interests. Contact us today to discuss your situation and develop a plan that addresses your specific exposure.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}