Running a business across borders means navigating tax codes from multiple countries simultaneously. Most companies either overpay taxes or miss deductions they’re legally entitled to claim.

We at Bette Hochberger, CPA, CGMA help businesses implement international tax planning optimization strategies that reduce your tax burden while keeping you compliant. This guide walks you through the structure, techniques, and decisions that shape a genuinely effective global tax strategy.

Understanding International Tax Obligations

What International Taxes Actually Cost Your Business

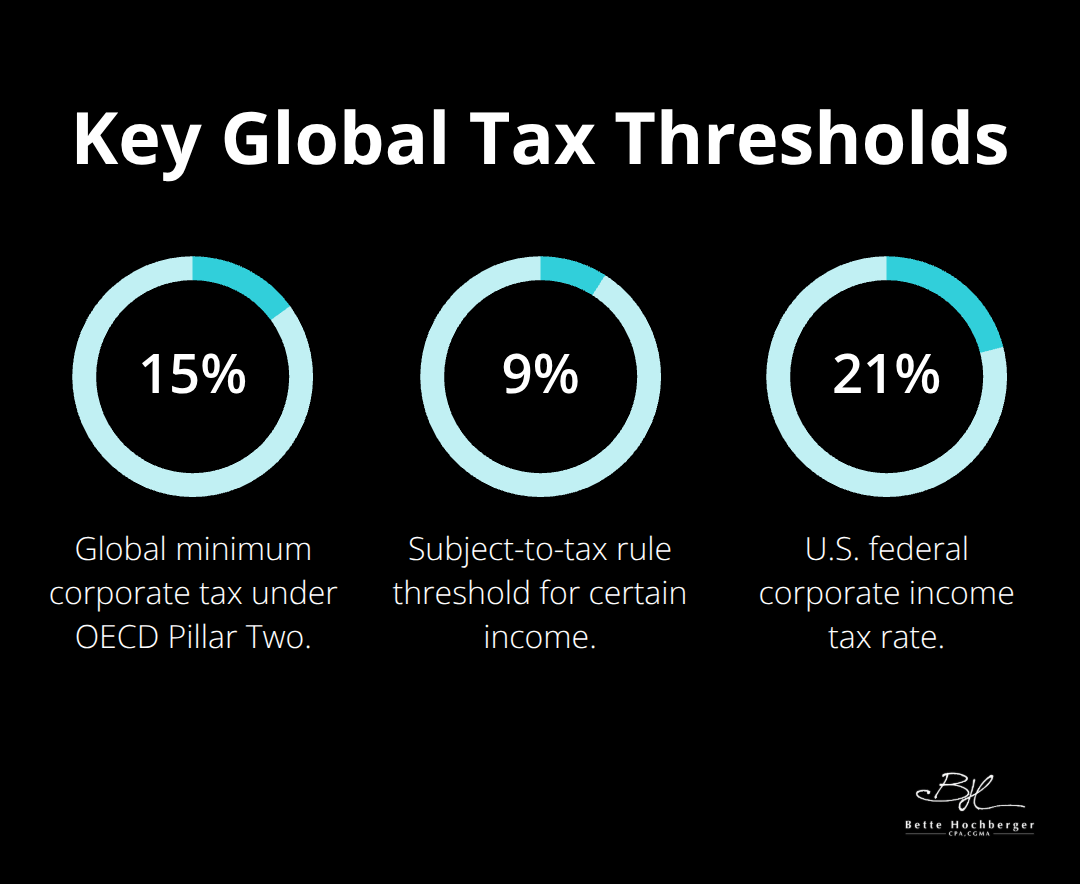

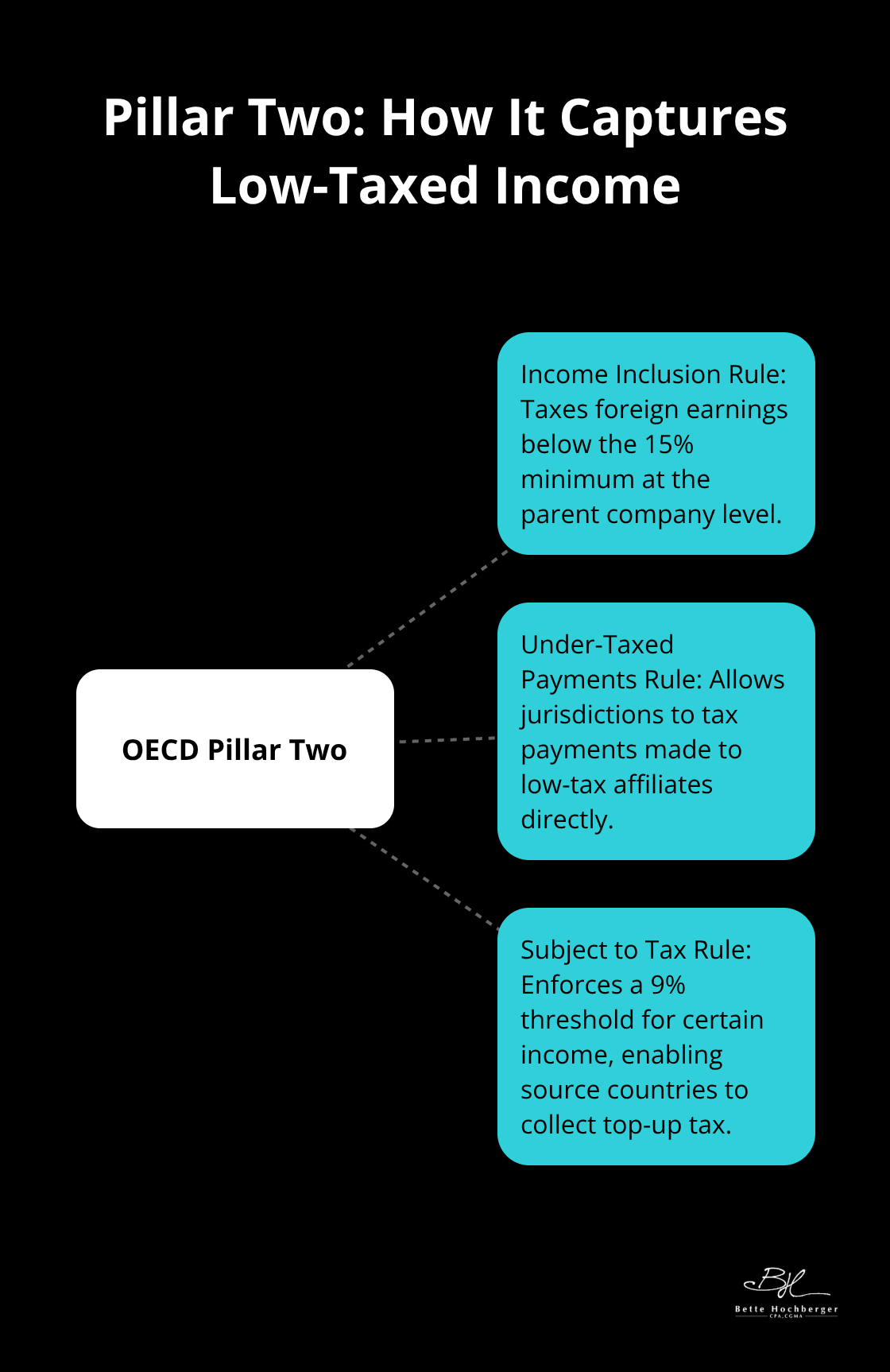

The moment you earn income across borders, you face taxation in multiple jurisdictions simultaneously. The OECD reports that multinationals with revenues exceeding €750 million must comply with the global minimum tax framework, which establishes a 15% floor on corporate taxation. Pillar Two applies through three mechanisms: the income inclusion rule taxes low-taxed foreign earnings at the parent company level, the under-taxed payments rule allows jurisdictions to tax payments to low-tax affiliates, and the subject to tax rule creates a 9% threshold for certain income.

You’ll also encounter country-specific income taxes, withholding taxes on cross-border payments ranging from 5% to 30% depending on treaty status, value-added taxes on goods and services, and employment-related taxes. Most businesses underestimate these cumulative obligations. Without a deliberate international tax plan, your worldwide tax liability and compliance obligations can double or triple, directly reducing competitiveness. The EU is expanding compliance requirements through country-by-country reporting, mandatory disclosure regimes, and cross-border arrangement reporting, while e-filing has become mandatory in most developed economies. Many companies waste resources filing in every jurisdiction without understanding which taxes actually apply to their specific structure.

How Tax Treaties Transform Your Bottom Line

A tax treaty between two countries allocates taxing rights and prevents double taxation on the same income. The United States maintains roughly 70 tax treaties that define how dividends, interest, royalties, and business profits are taxed across borders. Consider a practical example: without a treaty, a US parent company might face 30% withholding tax on dividends from a foreign subsidiary. Under the applicable treaty, this rate often drops to 5% or 15%, immediately improving cash flow. Treaties also provide foreign tax credits or exemptions that prevent taxation of the same income in both countries. However, limitation of benefits clauses exist specifically to prevent treaty abuse, requiring your structure to meet certain criteria to claim benefits. Before you expand internationally, conduct a treaty analysis with an international tax advisor to identify benefits specific to your target jurisdictions. Many companies establish operations in treaty jurisdictions without realizing they’ve missed critical benefits or triggered unexpected withholding obligations in non-treaty countries.

Permanent Establishment Rules Shape Your Tax Exposure

The permanent establishment rules embedded in treaties determine when your foreign business triggers tax liability in the host country. If your operations don’t meet permanent establishment thresholds, you may avoid local taxation entirely. Your business structure, the nature of your activities, and the duration of your presence all influence whether a permanent establishment exists. Mapping your global footprint early identifies treaty versus non-treaty jurisdictions and the tax treatment each offers. This analysis reveals which locations provide treaty benefits and which ones expose you to unexpected tax obligations. Understanding these distinctions before you commit resources to a new market prevents costly restructuring later. The right international tax advisor helps you navigate these rules and position your operations to minimize exposure while maintaining full compliance.

Structuring Your Global Operations for Maximum Tax Efficiency

Entity selection determines your tax rate

The structure you choose for your international operations determines whether you pay 15% or 40% in combined taxes. Most companies default to a subsidiary structure in every country without analyzing whether that structure actually minimizes their tax burden. The US corporate tax rate sits at 21%, but your effective rate depends entirely on where you place entities, how you allocate profits between them, and which credits you claim.

A pass-through structure often works better than corporate subsidiaries when you expand into high-tax countries because foreign income routes into your US return and you leverage foreign tax credits more efficiently. The OECD’s global minimum tax framework now requires multinationals with revenues exceeding €750 million to pay at least 15% tax in each jurisdiction, which means aggressive tax minimization strategies face real constraints.

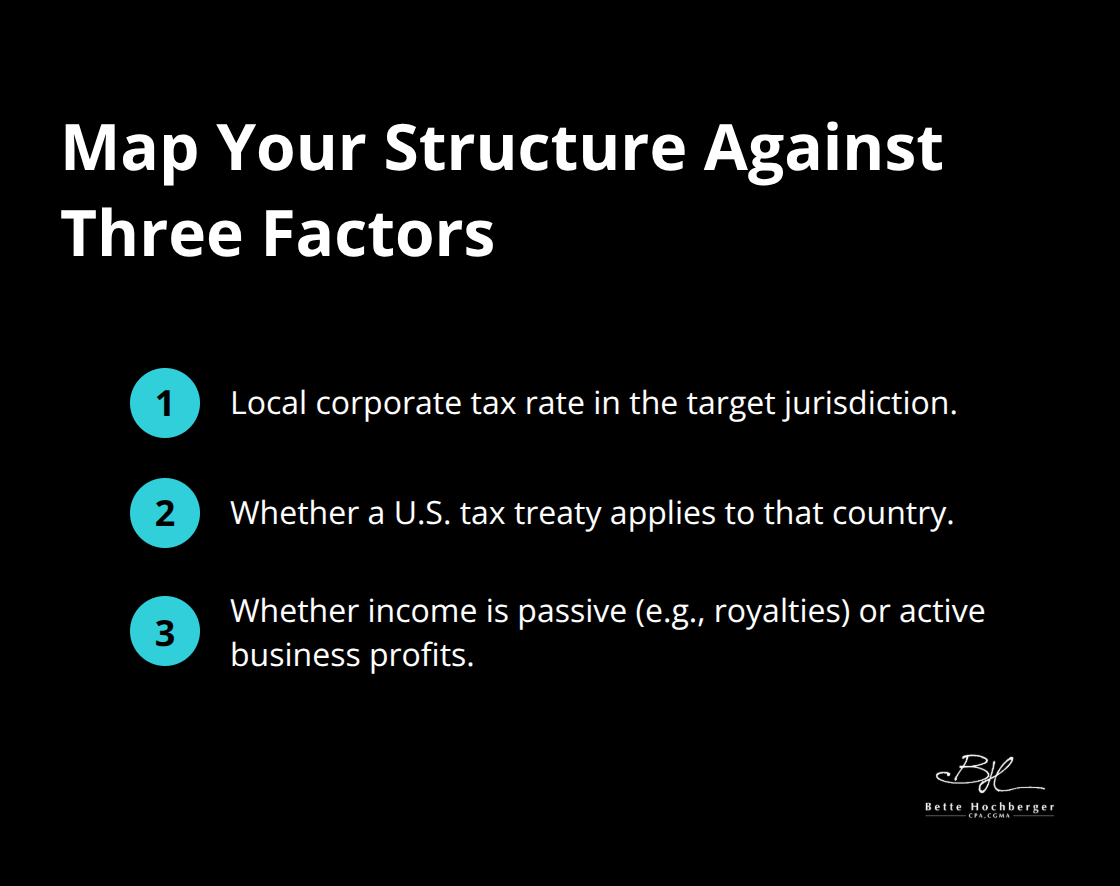

Before you establish operations anywhere, map your structure against three factors: the local tax rate in your target jurisdiction, whether that country has a tax treaty with the US, and whether your business model generates passive income like royalties or active business profits. A company expanding into Ireland might structure differently than one entering Germany because Ireland’s corporate tax rate is 12.5% while Germany’s is 30%. This structural decision alone can reduce your global tax liability by millions annually.

Transfer pricing requires arm’s length documentation

Transfer pricing represents your second critical decision point, and the IRS treats mispricing as a serious violation. Transfer pricing rules require that transactions between related entities occur at arm’s length prices-the price you’d charge an unrelated third party. The OECD transfer pricing guidelines and IRS regulations demand detailed documentation showing how you determined these prices.

If you manufacture components in a low-tax jurisdiction and sell them to your US parent at below-market prices, the IRS will recharacterize those profits and assess penalties that often exceed the tax itself. Establish transfer pricing policies before you begin cross-border transactions, not after an audit triggers scrutiny. A smartphone manufacturer that sources components from Taiwan and sells finished products from the US needs transfer pricing documentation that withstands IRS examination.

Foreign Tax Credits Prevent Double Taxation

Foreign tax credits and deductions form your final optimization layer. If you pay taxes to multiple countries on the same income, foreign tax credits prevent double taxation by allowing you to claim credits for taxes paid abroad against your US liability. The mechanism works differently for different income types: dividends from foreign subsidiaries may qualify for a dividends-received deduction, while GILTI income and Subpart F income have separate credit calculations.

Understanding which income category applies to your specific situation determines whether you recover 80% or 100% of your foreign taxes paid. These credit calculations interact with your entity structure and transfer pricing decisions, which means you cannot optimize one element in isolation. The interplay between where you locate your operations, how you price intercompany transactions, and which credits you claim creates either significant tax savings or unexpected exposure.

Your next step involves moving beyond basic structuring into the advanced techniques that separate tax-efficient companies from those leaving money on the table.

Substance Over Strategy: Why Real Operations Matter More Than Tax Planning

Tax Authorities Now Demand Genuine Economic Activity

The OECD BEPS initiative and Pillar Two rules have fundamentally shifted how tax authorities evaluate international structures. Tax authorities scrutinize whether your operations possess genuine economic substance or exist solely to reduce taxes. The permanent establishment rules and substance requirements work together to determine legitimate tax treatment. If you establish a subsidiary in a low-tax jurisdiction but conduct no actual business there, tax authorities will disregard that entity and reallocate profits to where real economic activity occurs.

This means your office lease, employee payroll, management decisions, and customer relationships must align with where you claim profits. A US software company that routes all revenue through an Irish subsidiary but maintains product development, sales, and customer support entirely in the US faces significant exposure because the Irish entity lacks substance. The IRS and OECD expect documented evidence that your structure reflects genuine business operations, not tax avoidance.

Permanent Establishment Rules Trigger Unexpected Tax Obligations

Permanent establishment rules define when your foreign business triggers local tax liability, and these rules have tightened considerably. If you maintain a fixed place of business abroad for more than six months, or if your dependent agent regularly negotiates contracts on your behalf, you have likely created a permanent establishment even if you did not intend to. This triggers corporate tax obligations in that jurisdiction regardless of your entity structure.

The consequences extend beyond the initial tax bill. Once a permanent establishment exists, you must file local returns, maintain compliance documentation, and potentially hire local tax advisors to manage ongoing obligations. Many companies discover permanent establishment exposure only after tax authorities assess back taxes and penalties.

Country-by-Country Reporting Exposes Profit Misalignment

The OECD BEPS framework introduced country-by-country reporting requirements for multinationals with revenues exceeding €750 million, and these reports expose misalignment between where you claim profits and where your actual operations sit. Tax authorities across 38 OECD member countries now exchange this data automatically, making it nearly impossible to hide profit shifting. The three mechanisms under Pillar Two actively hunt for low-taxed income: the income inclusion rule taxes foreign earnings below 15% at the parent company level, the under-taxed payments rule allows jurisdictions to tax payments to low-tax affiliates directly, and the subject to tax rule creates enforcement mechanisms at the 9% threshold.

This means establishing operations in a 12.5% jurisdiction like Ireland no longer provides the protection it once did because Pillar Two rules will tax the difference between that rate and 15% at the parent level. Your real strategic opportunity lies in legitimate tax-advantaged jurisdictions that align with genuine business operations.

Align Tax Benefits With Actual Business Functions

If you manufacture products in Mexico because of lower labor costs and established supply chains, the tax benefits follow naturally. If you establish an R&D center in a jurisdiction offering research credit incentives because your business actually conducts product development there, those credits withstand scrutiny. Tax authorities accept these structures because the business rationale exists independent of tax considerations.

Try mapping your global operations against actual business functions before considering tax benefits. This approach ensures compliance while capturing legitimate savings that survive audit. The companies that successfully navigate modern international tax rules structure their operations around genuine economic activity first, then optimize taxes within that framework.

Final Thoughts

An effective international tax strategy requires you to align your structure with genuine business operations rather than pursuing generic tax reduction tactics. OECD Pillar Two rules now tax low-taxed income at the parent company level, country-by-country reporting exposes profit misalignment automatically, and tax authorities across 38 member countries exchange this data without delay. This regulatory shift means aggressive tax minimization strategies face real constraints, but substantial legitimate savings remain available to companies that structure properly.

The complexity of modern international taxation makes professional guidance essential. Transfer pricing documentation, permanent establishment analysis, treaty benefit qualification, and Pillar Two compliance calculations require expertise that most internal teams cannot provide. We at Bette Hochberger, CPA, CGMA help businesses implement international tax planning optimization strategies that minimize your tax liabilities while maintaining full compliance across jurisdictions.

Your next step involves conducting a comprehensive review of your current structure against these principles. Contact Bette Hochberger, CPA, CGMA to develop a customized international tax strategy that captures legitimate savings while protecting your business from regulatory exposure.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}