At Bette Hochberger, CPA, CGMA, we know that understanding tax deductions for LLCs is essential for business owners looking to maximize their financial benefits.

LLCs offer unique tax advantages, but navigating the complexities of deductions can be challenging. This guide will walk you through common deductions, special considerations, and strategies to optimize your LLC’s tax position.

Whether you’re a single-member or multi-member LLC, we’ll help you uncover potential savings and avoid common pitfalls in your tax planning.

What Tax Deductions Can LLCs Claim?

LLCs can access a wide range of tax deductions to reduce their tax burden significantly. Let’s explore some of the most impactful deductions available to LLCs.

Business Operating Expenses

The core of LLC tax deductions consists of ordinary and necessary business expenses. These include rent, utilities, office supplies, and inventory costs. For example, a retail LLC can deduct the cost of goods sold, which directly reduces taxable income.

Home Office and Vehicle Expenses

LLCs operating from home can benefit from the home office deduction. This allows for the deduction of a portion of mortgage or rent, utilities, and maintenance costs based on the percentage of the home used exclusively for business. Vehicle expenses for business use also qualify for deductions. The IRS offers two methods: the standard mileage rate (67 cents per mile for 2024) or the actual expenses method.

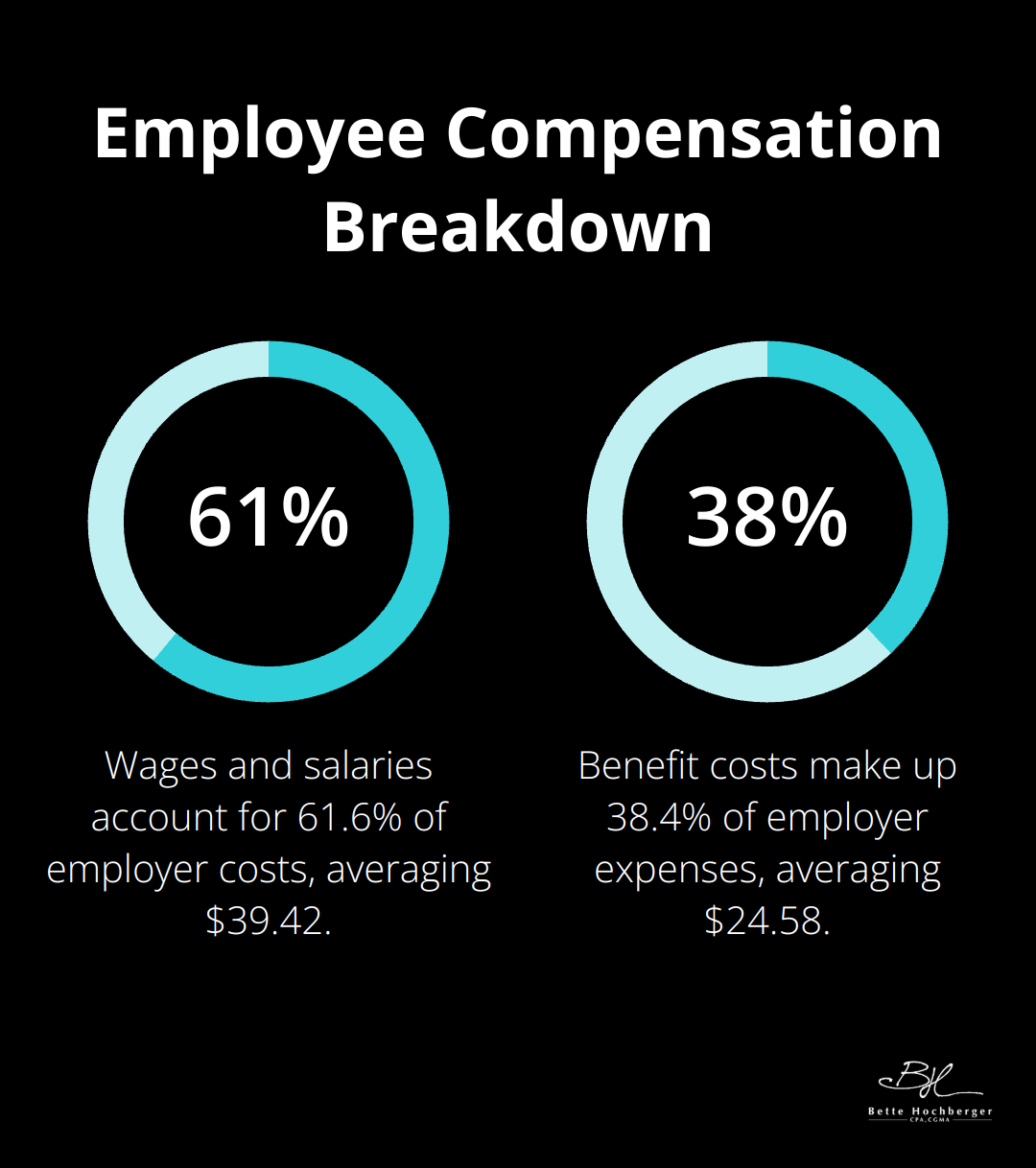

Employee Compensation and Benefits

LLCs with employees can deduct their salaries, wages, and benefits fully. This encompasses health insurance premiums, retirement plan contributions, and other fringe benefits. Single-member LLCs can deduct their own health insurance premiums as well. According to the Bureau of Labor Statistics, wages and salaries averaged $39.42 and accounted for 61.6 percent of employer costs, while benefit costs averaged $24.58 and accounted for 38.4 percent.

Professional Services and Education

Fees paid to lawyers, accountants, and other professionals for business-related services qualify as deductible expenses. Education or training expenses that maintain or improve skills needed in the business also qualify for write-offs. This could include conference fees, online courses, or industry-specific certifications.

Equipment and Depreciation

LLCs can deduct the cost of equipment and machinery used in their business operations. The IRS allows for immediate expensing of up to $1,220,000 of qualifying equipment and software purchased in 2024 under Section 179. This provision can provide substantial tax relief for LLCs investing in new assets.

To maximize these deductions effectively, LLCs must maintain meticulous records and understand the specific rules for each deduction. Professional guidance can help navigate these complexities and optimize tax strategies. The next section will discuss special considerations that LLCs should keep in mind when claiming these deductions.

How Special Considerations Affect LLC Tax Deductions

Pass-Through Taxation Impact

LLCs typically operate as pass-through entities for tax purposes. This structure means the LLC itself does not pay federal income taxes on business income. Instead, profits and losses flow through to the individual members’ tax returns. While this avoids double taxation, it can push LLC members into higher personal tax brackets.

For instance, a single-member LLC owner with $100,000 in business income reports this on their personal tax return. This could potentially increase their overall tax rate. Multi-member LLCs distribute profits according to their operating agreement, which affects each member’s tax liability differently.

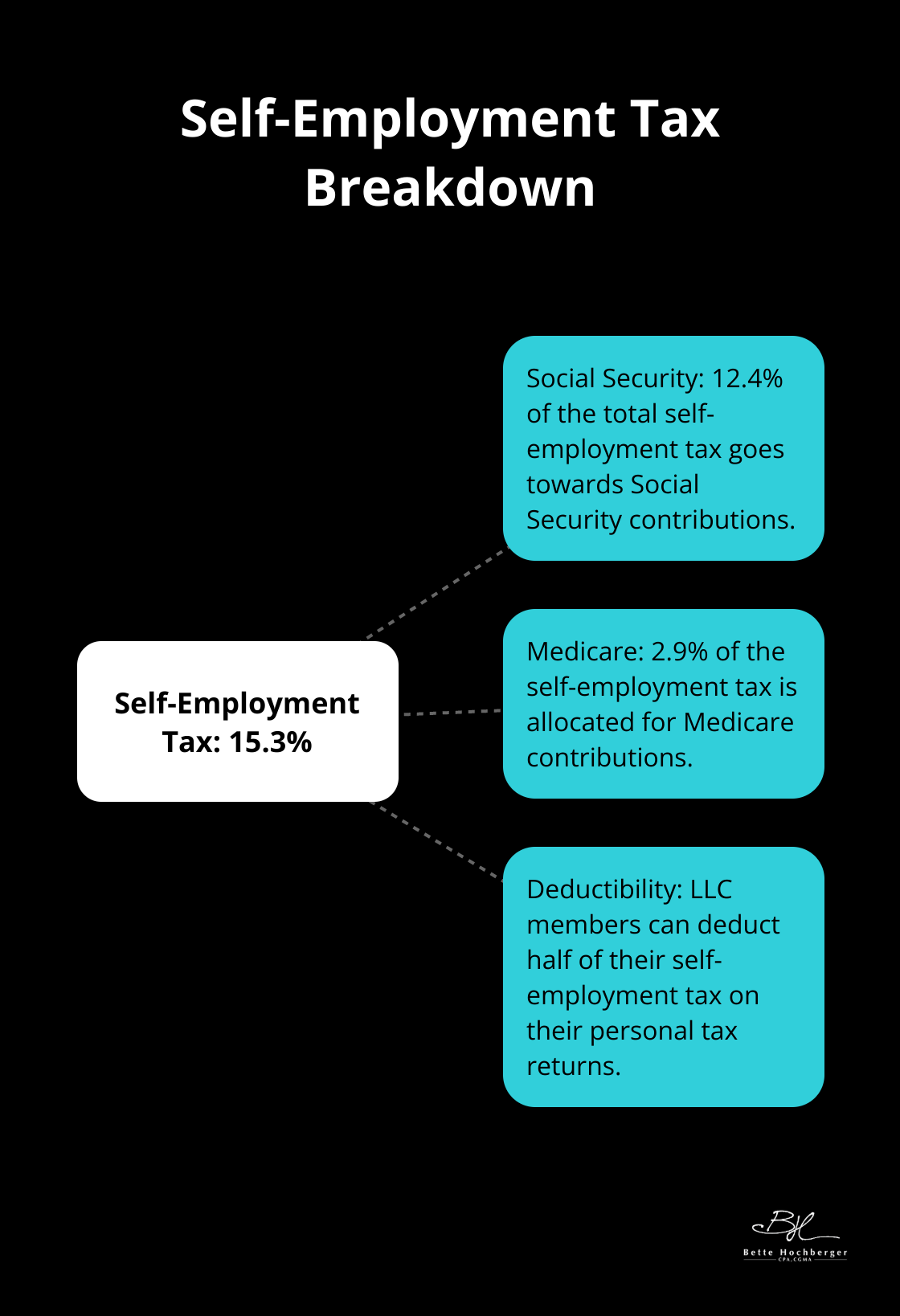

Self-Employment Taxes for Members

LLC members usually fall under the self-employed category for tax purposes. They must pay self-employment taxes on their share of LLC profits. The self-employment tax rate is 15.3%, consisting of 12.4% for social security and 2.9% for Medicare. Members can deduct half of this tax on their personal returns.

Some LLCs elect to be taxed as S corporations to potentially reduce self-employment taxes. This strategy involves paying a reasonable salary to members (subject to employment taxes) and distributing remaining profits as dividends (not subject to self-employment tax).

State-Specific LLC Taxation

Federal tax rules for LLCs remain consistent across the country, but state-level taxation varies significantly. Some states impose additional taxes or fees on LLCs. California, for example, charges an annual $800 minimum franchise tax for LLCs, regardless of profitability.

Other states offer specific deductions or credits that LLCs can use to their advantage. New York provides various tax incentives for businesses in certain industries or locations. Understanding your state’s specific rules proves essential for optimizing your tax strategy.

Single-Member vs. Multi-Member LLCs

The tax treatment differs between single-member and multi-member LLCs in several key ways. Single-member LLCs typically receive treatment as sole proprietorships for tax purposes, reporting business income on Schedule C of their personal tax return. Multi-member LLCs usually receive treatment as partnerships, filing Form 1065 and issuing Schedule K-1 to each member.

This distinction affects not only how taxes are filed but also the available deductions and strategies. Multi-member LLCs have more flexibility in allocating profits and losses among members, which can serve as a valuable tax planning tool.

These special considerations play a significant role in how LLCs optimize their tax positions. Each situation requires a unique approach, and professional guidance can help navigate these complexities effectively. The next section will explore strategies to maximize LLC tax deductions, building on the foundation of these special considerations.

How LLCs Can Maximize Their Tax Deductions

At Bette Hochberger, CPA, CGMA, we understand the impact of proper tax planning on an LLC’s bottom line. Maximizing tax deductions requires a strategic approach and attention to detail. Here’s how LLCs can optimize their tax positions:

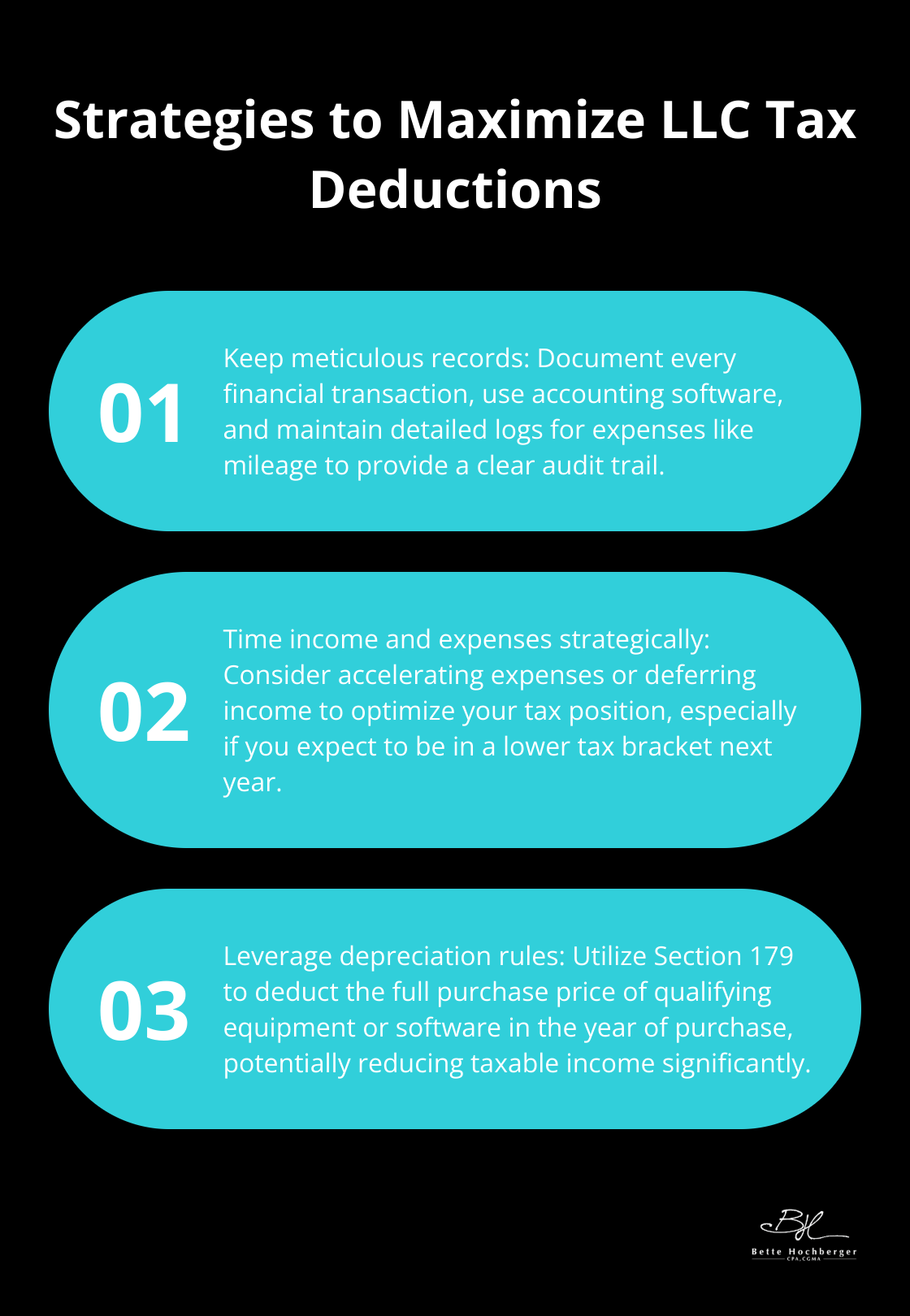

Keep Meticulous Records

The foundation of maximizing tax deductions is impeccable record-keeping. Document and organize every receipt, invoice, and financial transaction. Use accounting software to track expenses in real-time. This simplifies tax preparation and provides a clear audit trail if the IRS investigates.

For mileage deductions, maintain a detailed log of business trips (including dates, destinations, and purposes). The IRS scrutinizes vehicle expenses closely, so thorough documentation is essential.

Time Income and Expenses Strategically

Timing can significantly affect your tax liability. If your LLC uses cash-basis accounting, consider accelerating expenses into the current tax year or deferring income to the next year to lower your current tax bill. This strategy works well if you expect to be in a lower tax bracket next year.

For example, if you plan a major equipment purchase, buying in December rather than January could provide immediate tax benefits. However, avoid artificially manipulating your finances solely for tax purposes, as this can alert the IRS.

Use Depreciation and Section 179

Understanding depreciation rules can lead to substantial tax savings. Section 179 of the tax code allows LLCs to deduct the full purchase price of qualifying equipment or software purchased or financed during the tax year. For 2025, the deduction limit is $2,500,000.

If your LLC purchases $50,000 worth of office equipment, you could potentially deduct the entire amount in the year of purchase (instead of depreciating it over several years), substantially reducing your taxable income.

Maximize Retirement Contributions

LLC owners can use retirement plans as powerful tax-saving tools. Options like SEP IRAs, SIMPLE IRAs, or Solo 401(k)s allow for significant pre-tax contributions.

This reduces your current tax liability and helps build your retirement nest egg. The key is choosing the right plan for your LLC’s size and financial situation.

Optimize Health Insurance Premiums

Self-employed individuals (including single-member LLC owners) can deduct 100% of their health insurance premiums, including coverage for spouses and dependents. This often-overlooked deduction can result in substantial tax savings.

Multi-member LLCs can also benefit by setting up a health reimbursement arrangement (HRA) to provide tax-free health benefits to employees, including members.

Final Thoughts

Tax deductions for LLCs offer numerous opportunities to reduce tax burdens and improve financial health. LLCs must maintain meticulous records, strategically time income and expenses, and leverage depreciation rules to maximize these deductions. However, tax laws constantly evolve, making it essential to stay informed about changes and reassess business structures regularly.

Professional expertise often proves necessary to navigate the intricacies of LLC taxation effectively. At Bette Hochberger, CPA, CGMA, we specialize in personalized financial services for businesses, including strategic tax planning and preparation. Our team uses advanced technology to help diverse industries minimize tax liabilities and ensure profitability.

Effective tax planning requires an ongoing process, not just a yearly event. Proactive planning and expert guidance can transform tax season from a stressful obligation into a strategic opportunity for your LLC’s financial success. Consider how your growth plans might impact your tax situation and plan accordingly.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}